Data Center M&A • Peaking Inflation? • Sell-Off Deepens

- U.S. equity markets finished lower again Wednesday in another volatile session after CPI inflation data failed to show significant signs of easing, likely keeping the "pedal-to-the-metal" for Fed monetary tightening.

- Now having shed more than 8% in the past five trading sessions, the S&P 500 declined another 1.7% while the tech-heavy Nasdaq 100 dipped 3.0% to the cusp of a 30%-drawdown.

- Real estate equities were relative outperformers today amid a tough start to the month as the Equity REIT Index declined by 0.2% today with 8-of-19 property sectors in positive territory.

- Peak Inflation? Perhaps Not Quite Yet. Consumer prices rose at a hotter-than-expected pace in April but did ease slightly from the four-decade-high rate set last month as cost increases for food, airline fares, and vehicles kept persistent upward pressure on prices.

- The data center REIT sector remains a hotbed of M&A activity. Data center REIT DigitalBridge (DBRG) announced that it will acquire data center operator Switch (SWCH), leveraging its private equity platform to outbid Brookfield Asset Management.

Income Builder Daily Recap

We recently launched Hoya Capital Income Builder - a premier income-focused investment research service through Seeking Alpha Marketplace - that will be the new exclusive home of all of Hoya Capital's investment research. Income Builder focuses on real income-producing asset classes that offer the opportunity for diversification, monthly income, capital appreciation, and inflation hedging. If you're not already on board, give us a try with a completely risk-free two-week trial and take a look around.

U.S. equity markets finished lower again Wednesday in another volatile session after CPI inflation data failed to show significant signs of easing and likely kept the "pedal to the metal" for the Fed to continue on its accelerated path of monetary tightening. Now having shed more than 8% in the past five trading sessions, the S&P 500 declined another 1.7% today while the tech-heavy Nasdaq 100 dipped 3.0% and is now on the cusp of a 30% drawdown. Real estate equities were relative outperformers today amid a tough start to the month as the Equity REIT Index declined by 0.2% today with 8-of-19 property sectors in positive territory while Mortgage REITs declined 1.1%.

Peak Inflation? Perhaps Not Quite Yet. Consumer prices rose at a hotter-than-expected pace in April but did ease slightly from the four-decade-high rate set last month as cost increases for food, airline fares, and vehicles kept persistent upward pressure on prices. The headline Consumer Price Index (CPI-U) increased 0.3% in April to bring its year-over-year increase to 8.3% - higher than consensus estimates of 8.1%. The Core CPI - the metric on which the Fed focuses its attention - rose 6.2% - above expectations for a 6% gain. The hotter-than-expected report came despite a 2.7% monthly decline in energy prices and a 6.1% drop in gasoline prices, both of which are poised to reverse in May at based on current prices. The index for airline fares continued to rise sharply, increasing 18.6% in April, the largest 1- month increase on record.

As we've discussed for the last year, we continue to project persistent pressure on the headline inflation metrics due to the delayed impact of soaring rents and home values, which are just beginning to filter in the data. The cost of shelter increased 0.5% in April to bring its year-over-year rise to 5.1% - which we believe still significantly understates the actual rise in shelter costs. Private market rent data has shown that national rent inflation has been in the 10-15% range over the past six months while home values have risen by 15-20%. The Dallas Fed published a report highlighting the data issues at the BLS, finding a 16-month lag between the BLS inflation series and real-time market pricing of home prices and rents which will add an estimated 0.6-1.2% to the Core CPI index in 2022 and 2023.

Real Estate Daily Recap

Data Center: The data center REIT sector remains a hotbed of M&A activity. Consistent with reports earlier in the week, data center REIT DigitalBridge (DBRG) announced that it will acquire data center operator Switch (SWCH) for about $11 billion in cash, including the assumption of debt. Switch - which went public in 2017 and owns 16 large data centers across 5 large campuses focused primarily on colocation service - had planned to convert to a REIT for the 2023 fiscal year. Despite its modest market cap of around $4B and its recent transition from a diversified REIT into a pure-play technology REIT, DigitalBridge has leveraged its private equity platform to fuel a buying spree that has rapidly established the firm as one of the world's largest technology real estate operators, having now acquired more than a dozen companies including DataBank and Vantage Data Centers. DBRG reported beat-out Brookfield Asset Management (BAM) for Switch and is part of a year-long M&A boom that has seen Blackstone (BX) acquire QTS Realty for its non-traded REIT, KKR (KKR) and Global Infrastructure Partners acquire CyrusOne, and cell tower REIT American Tower (AMT) acquire CoreSite.

Industrial: While one REIT was finalizing a deal, another REIT was getting rejected. Duke Realty (DRE) rallied by nearly 8% after formally responding to yesterday's proposed acquisition by Prologis (PLD). Duke rejected the offer, noting that the latest $24 billion offer was "virtually unchanged" from prior proposals and is "insufficient", though the company still remains open to exploring ideas. Prologis has been actively pursuing Duke for at least six months and Duke previously rejected two proposals - the first one coming on November 29th and then again on May 3rd. Under the terms of yesterday's proposal, Duke Realty stockholders would receive 0.466 shares of Prologis common stock for each share of Duke Realty common stock they own and would own 19% of the combined company - which would be far-and-away the largest industrial real estate owner in the world.

Yesterday, we published our real estate Earnings Recap: REITs Are Suddenly Cheap. REIT earnings results were generally better-than-expected with roughly 85% of equity REITs beating consensus FFO estimates while nearly 70% of the REITs that provide forward guidance raised their full-year outlook. Despite the strong slate of earnings reports across most property sectors, however, performance trends continue to be dominated by macroeconomic factors and the broader sell-off across essentially all asset classes. The steep sell-off combined with upward earnings revisions and dividend hikes has pulled valuations to the "cheapest" level since 2020 and swelled the average dividend yield to the highest since 2018.

Mortgage REIT Daily Recap

Per the REIT Rankings Tracker available to Income Builder subscribers, mortgage REITs were mixed today as a solid earnings season wraps up. Granite Point (GPMT) advanced 0.6% today after reporting better-than-expected results including a relatively modest 2% decline in its Book Value Per Share ("BVPS") in Q1. In our Earnings Recap published yesterday, we noted that Residential mREIT Book Value Per Share ("BVPS") metrics declined by 8.5%, on average, in Q1 with a range of +10% to -28%. Book value changes across the commercial mREIT space were more muted with an average BVPS increase of 0.1% ranging from a high of 3.8% to a low of 1.9%.

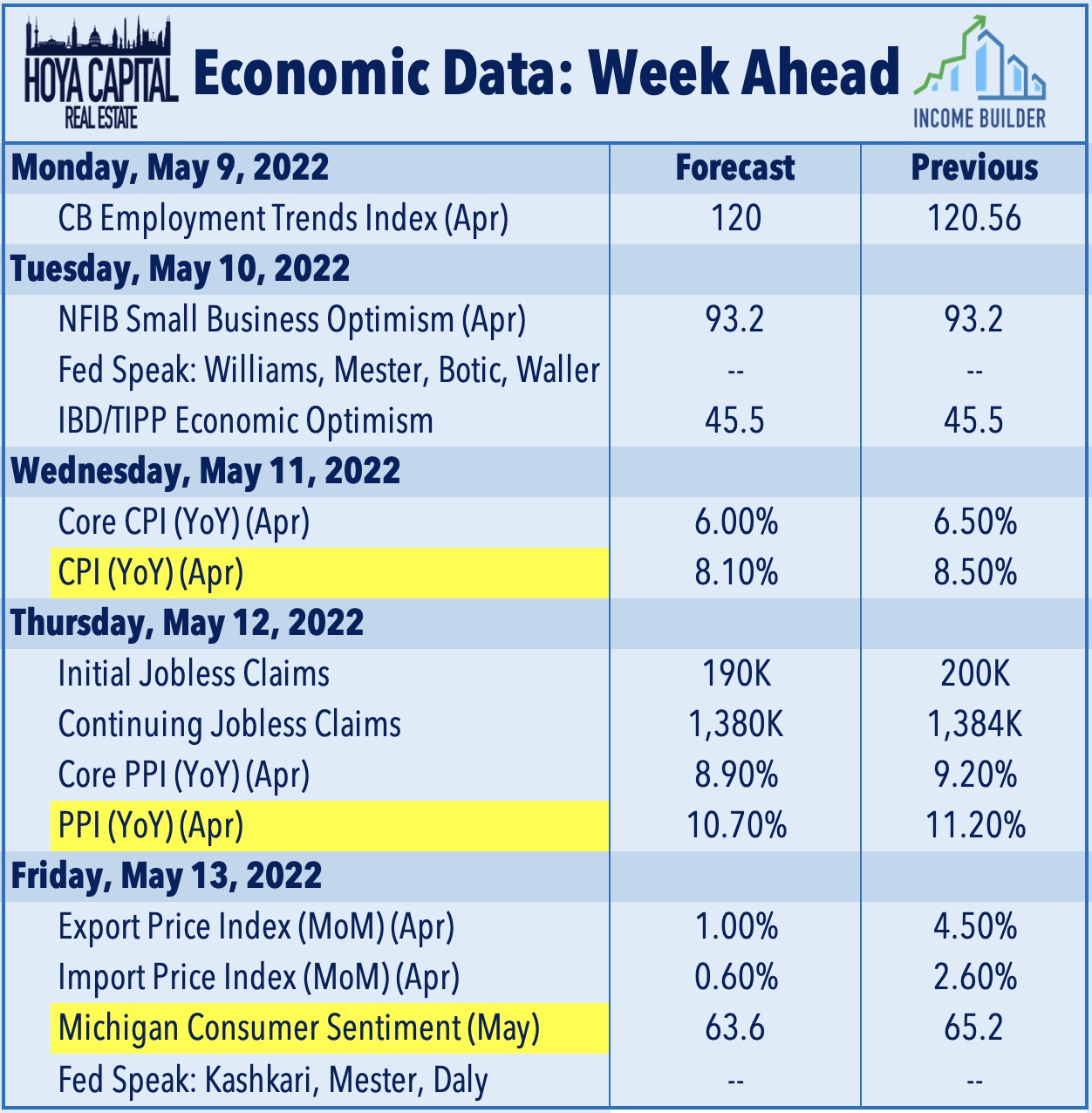

Economic Data In The Week Ahead

Inflation data and commentary from Fed members highlight the busy slate of economic data in the week ahead. On Wednesday, the BLS will report the Consumer Price Index which may potentially reveal that the fastest pace of year-over-year increases is finally behind us as both the headline and Core CPI is expected to show a cooldown in April to 8.1% and 6.0%, respectively. Similar themes are expected in the Producer Price Index report on Thursday is expected to show a 10.7% increase for the headline PPI, down from 11.2% in the prior month. On Friday, we'll also get our first look at Michigan Consumer Sentiment for May to see if the unexpected rebound in confidence seen last month can be sustained or if it resumes the downward trend that began last August amid persistent anxiety about inflation.

Access Our Complete Research Library

We recently launched Hoya Capital Income Builder - the new premier investment research service focused on real income-producing assets classes. Whether your focus is High Yield or Dividend Growth, we’ve got you covered with high-quality, actionable investment research and a comprehensive suite of tools and models to help build sustainable portfolio income targeting premium dividend yields of up to 10%. And of course, subscribers receive complete access to our investment research - including reports that are never published elsewhere - from Hoya Capital and our team of contributors.

Disclosure: Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index. Index definitions and a complete list of holdings are available on our website.

Additional Disclosure: It is not possible to invest directly in an index. Index performance cited in this commentary does not reflect the performance of any fund or other account managed or serviced by Hoya Capital Real Estate. Data quoted represents past performance, which is no guarantee of future results. Information presented is believed to be factual and up-to-date, but we do not guarantee its accuracy.