REIT Earnings Begin • Farmland Dividend Hike • Week Ahead

- U.S. equity markets finished broadly lower Monday ahead of a busy week of earnings and economic data as stocks retreated from early-session gains despite relatively solid earnings results this morning.

- Following declines of 0.9% last week, the S&P 500 finished lower by 0.8% while the more domestic-focused Small-Cap 600 and Mid-Cap 400 finished essentially flat.

- Real estate equities were mixed today as a rebound from retail and hotel REITs was offset by pressure on technology and industrial REITs. The Equity REIT Index declined 0.7% today.

- REIT earnings season kicked off this morning with very strong results from Prologis and Duke Realty - a pair of the most closely-watched reports of the entire month. PLD boosted its full-year FFO and NOI outlook while reporting a record-high 45.6% increase in effective rents.

- Gladstone Land (LAND) was among the leaders today after it boosted its monthly dividend by 0.4%, its third dividend hike this year. Farmland REITs - which were the best-performing sector in the first quarter of this year - have sold off over the past quarter as concerns over inflation have been superseded by recession concerns.

Income Builder Daily Recap

U.S. equity markets finished broadly lower Monday ahead of a busy week of earnings and economic data as stocks retreated from early-session gains despite relatively solid earnings results this morning from several major banks. Following declines of 0.9% last week, the S&P 500 finished lower by 0.8% while the more domestic-focused Small-Cap 600 and Mid-Cap 400 finished essentially flat. Real estate equities were mixed today as a rebound from retail and hotel REITs was offset by continued pressure on technology and industrial REITs despite strong results from the two largest logistics-focused REITs. The Equity REIT Index finished lower by 0.7% today with 11-of-18 property sectors in negative territory while the Mortgage REIT Index finished lower by 0.2%.

As discussed in Inflation vs Recession, concerns over inflation have clashed with the emerging deflationary forces of stalling global economic growth with much of Europe and Asia appearing to be headed into contraction. The "pro-inflation" forces were the driving force today as Crude Oil prices bounced back above $100/barrel while the 10-Year Treasury Yield ticked higher by 3 basis points to close at 2.96%. Eight of the eleven GICS equity sectors finished lower on the day with Technology (XLV) stocks seeing the most significant mid-day reversal following reports that Apple (APLE) plans to slow hiring next year, erasing much of the positive sentiment earlier in the session following upbeat results from Bank of America (BAC) and Goldman Sachs (GS).

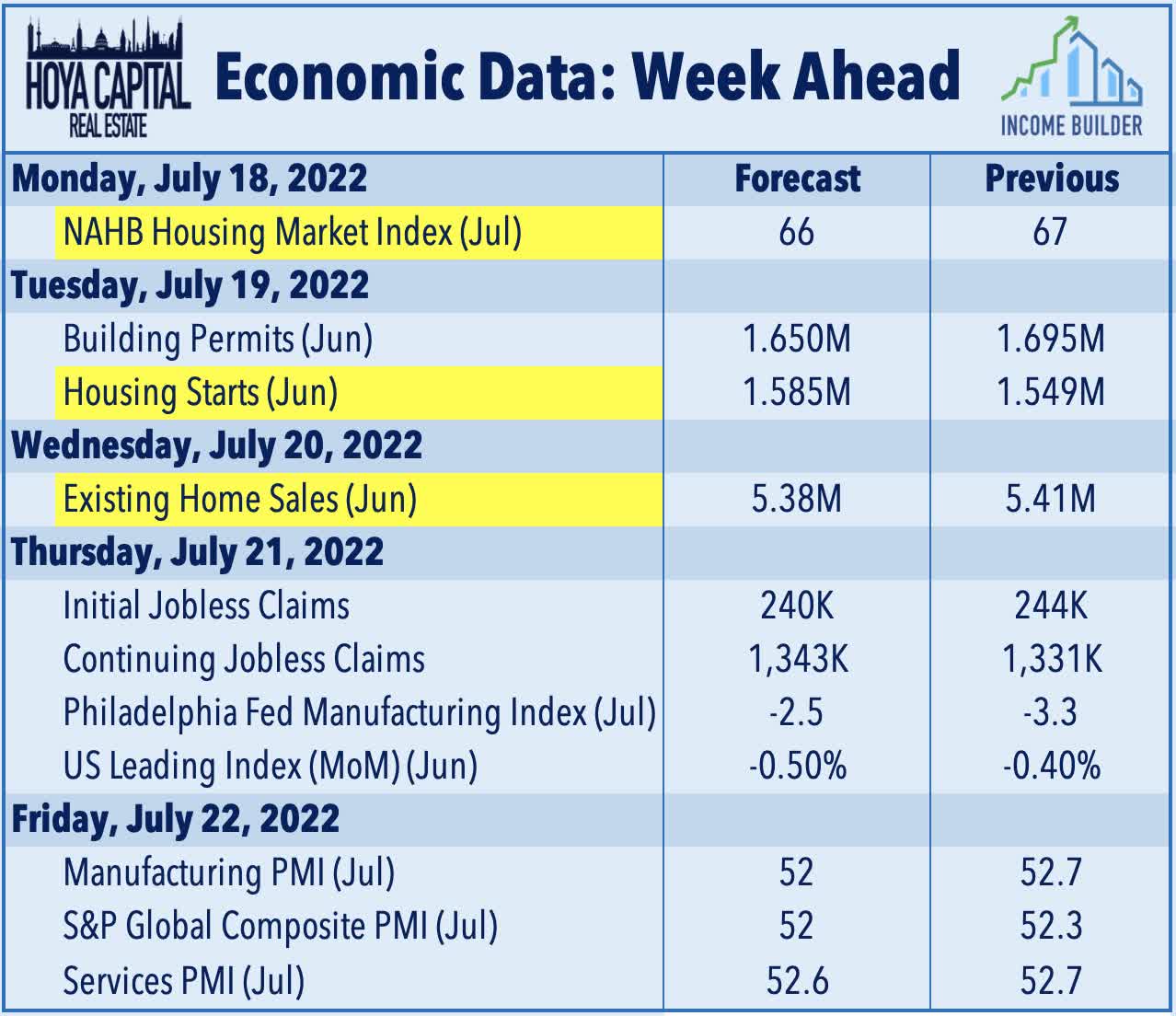

The state of the housing market will continue to be in focus throughout the week with a trio of reports expected to show a continued cool down in activity over the past month, reflecting the surge in mortgage rates which climbed to nearly 6% in late June before moderating in recent weeks. Following Homebuilder Sentiment data today, we'll see Housing Starts and Building Permits data on Tuesday which is expected to show a continued moderation in the pace of new home construction, particularly within the single-family segment. On Wednesday, we'll see Existing Home Sales data which is expected to slow to the lowest rate since June 2020. There are some early signs that the recent dip in mortgage rates, moderating home prices, and slightly higher inventory levels have pulled some potential buyers back into the fold in recent weeks, however, as the Redfin Homebuyer Demand Index has rebounded about 5% from its late-June lows.

Real Estate Daily Recap

Best & Worst Performance Today Across the REIT Sector

Real estate earnings season kicks off this week, and over the next month, we'll hear results from more than 175 equity REITs, 40 mortgage REITs, and dozens of housing industry companies. Today, we published our REIT Earnings Preview on the Income Builder Marketplace which discusses the major themes and metrics we'll be watching across each of the major property sectors this earnings season. Since the start of last earnings season, the Equity REIT Index has declined 16%, slightly lagging the 12% decline in the S&P 500 during this time while the 10-Year Yield is essentially after a brief surge to 3.50%. The past quarter has seen a reversal in property sector performance trends since early in 2022 with interest-rate-sensitive REITs catching a bid while pro-cyclical REITs have lagged on recession concerns.

Industrial: REIT earnings season kicked off this morning with very strong results from Prologis (PLD) and Duke Realty (DRE) - a pair of the most closely-watched reports of the entire month. Industrial REITs have been slammed over the past quarter after Amazon (AMZN) announced plans to cut costs in its logistics network. Results from Prologis showed few signs of slowing demand as the logistics giant boosted its full-year NOI and FFO outlook while recording an acceleration in renewal rates. PLD recorded a record-high 45.6% increase in effective rents and a record 27.5% increase in cash rents, a notable acceleration from last quarter. Despite the strong results, PLD finished lower by 1.5% on the day. Duke - which will be acquired by Prologis in a deal expected to close next quarter - reported net effective rental rate growth of 69% and cash rent growth of 57.1%.

Farmland: Gladstone Land (LAND) was among the leaders today after it boosted its monthly dividend by 0.4% to $0.0456/share - its third dividend hike this year. Farmland REITs - which were the best-performing sector in the first quarter of this year - have sold off over the past quarter as concerns over inflation have been superseded by recession concerns. LAND dipped nearly 50% from its all-time highs in mid-April to its recent lows in mid-June as worries over drought conditions in the west amplified the macroeconomic-related pressures. California, in particular, continues to struggle with a multi-year drought as snowpack levels, year-to-date precipitation, and reservoir levels are all below historical averages, pressure farmland valuations at farms with limited water supply. Farmland Partners (FPI) - which has more limited West Coast exposure - has posted more modest declines of roughly 15% over the past quarter.

Mortgage REIT Daily Recap

Per the REIT Rankings Tracker available to Income Builder subscribers, mortgage REITs were mixed today with residential mREITs slipping 1.5% while commercial mREITs gained 0.9%. Broadmark Realty (BRMK) finished flat today after it held its monthly dividend steady at $0.07/share. Hannon Armstrong (HASI) continued to bounce back today following a nearly 20% dip last week following the publication of a short report from Muddy Waters.

REIT Preferreds & Capital Raising

Per the Income Builder Preferred Tracker available to Income Builder subscribers, REIT Preferred stocks finished flat, on average. REIT Preferreds are lower by roughly 10% on a total return basis this year after ending 2021 with price returns of roughly 8.0% and total returns of roughly 14%. There are now roughly 180 REIT-issued exchange-listed preferred and debt securities with an average current yield of 6.97%. On Friday, Fitch Ratings affirmed Ventas' (VTR) credit rating of BBB+ and revised its outlook to stable from negative.

Disclosure: Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index. Index definitions and a complete list of holdings are available on our website.

Hoya Capital Research & Index Innovations (“Hoya Capital”) is an affiliate of Hoya Capital Real Estate, a registered investment advisory firm based in Rowayton, Connecticut that provides investment advisory services to ETFs, individuals, and institutions. Hoya Capital Research & Index Innovations provides non-advisory services including market commentary, research, and index administration focused on publicly traded securities in the real estate industry.

This published commentary is for informational and educational purposes only. Nothing on this site nor any commentary published by Hoya Capital is intended to be investment, tax, or legal advice or an offer to buy or sell securities. This commentary is impersonal and should not be considered a recommendation that any particular security, portfolio of securities, or investment strategy is suitable for any specific individual, nor should it be viewed as a solicitation or offer for any advisory service offered by Hoya Capital Real Estate. Please consult with your investment, tax, or legal adviser regarding your individual circumstances before investing.

The views and opinions in all published commentary are as of the date of publication and are subject to change without notice. Information presented is believed to be factual and up-to-date, but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. Any market data quoted represents past performance, which is no guarantee of future results. There is no guarantee that any historical trend illustrated herein will be repeated in the future, and there is no way to predict precisely when such a trend will begin. There is no guarantee that any outlook made in this commentary will be realized.

Readers should understand that investing involves risk and loss of principal is possible. Investments in real estate companies and/or housing industry companies involve unique risks, as do investments in ETFs. The information presented does not reflect the performance of any fund or other account managed or serviced by Hoya Capital Real Estate. An investor cannot invest directly in an index and index performance does not reflect the deduction of any fees, expenses or taxes.

Hoya Capital Real Estate and Hoya Capital Research & Index Innovations have no business relationship with any company discussed or mentioned and never receives compensation from any company discussed or mentioned. Hoya Capital Real Estate, its affiliates, and/or its clients and/or its employees may hold positions in securities or funds discussed on this website and our published commentary. A complete list of holdings and additional important disclosures is available at www.HoyaCapital.com.