PMI Plunge • REIT Earnings • Yields Retreat

- U.S. equity markets slipped Friday following three days of gains while interest rates declined after PMI data in both the U.S. and Eurozone showed an unexpectedly sharp contraction in economic activity.

- Still managing to hang onto gains of 2.5% for the week, the S&P 500 retreated by 0.9% today while the tech-heavy Nasdaq 100 dipped nearly 2% to trim its weekly.

- Real estate equities and other yield-sensitive market segments were among the outperformers today as the benchmark 10-Year Treasury Yield dipped to the lowest level since late May.

- The US PMI Composite Output Index dipped to 47.5 in July, down notably from 52.3 in June - marking the sharpest decline since May 2020 as both manufacturers and service providers reported subdued demand conditions.

- Alpine Income (PINE) was among the leaders today after reporting strong results and raising its full-year outlook while noting that private market valuations of net lease assets remain firm.

Income Builder Daily Recap

U.S. equity markets slipped Friday following three days of gains while benchmark interest rates dipped after PMI data in both the U.S. and Eurozone showed an unexpectedly sharp contraction in economic activity. Still managing to hang onto gains of 2.5% for the week, the S&P 500 retreated by 0.9% today while the tech-heavy Nasdaq 100 dipped nearly 2% to trim its weekly gains to 3.5%. Real estate equities and other yield-sensitive market segments were among the outperformers today as the benchmark 10-Year Treasury Yield dipped to the lowest level since late May. The Equity REIT Index gained 0.5% today with 13-of-18 property sectors in positive territory while the Mortgage REIT Index slipped 0.5%.

Economic activity contracted sharply in both the U.S. and Eurozone in July according to Flash PMI data from S&P Global released this morning. The US PMI Composite Output Index dipped to 47.5 in July, down notably from 52.3 in June - marking the sharpest decline since May 2020 as both manufacturers and service providers reported subdued demand conditions. The Euro Area PMI fell to 49.4 in July from 52.0 in June - the lowest since February 2021. Eight of the eleven GICS equity sectors finished lower on the day, but retreating yields sparked a bid for Utilities (XLU) and Real Estate (XLRE). Homebuilders and the broader Hoya Capital Housing Index continued their rebound as well today, lifted by moderating interest rates which should filter through into mortgage rates over the coming weeks.

Real Estate Daily Recap

Best & Worst Performance Today Across the REIT Sector

Net Lease: Alpine Income (PINE) was among the leaders today after reporting strong results and raising its full-year outlook citing "attractive asset pricing" that has resulted in "attractive net investment spreads and improved earnings growth." PINE - which recorded nearly 30% FFO growth last year - boosted its full-year FFO outlook by 200 basis points to 0.9%. PINE expects to accelerate its disposition activity which reflects its "continued confidence in our ability to sell assets at attractive valuations." PINE noted that despite the jump in interest rates, private markets pricing of net lease properties remains firm, commenting "on the smaller property sales, you're really seeing a lot of high net worth in and some institutional investors, buying these properties at Cap rates that really haven't changed too much from six months ago."

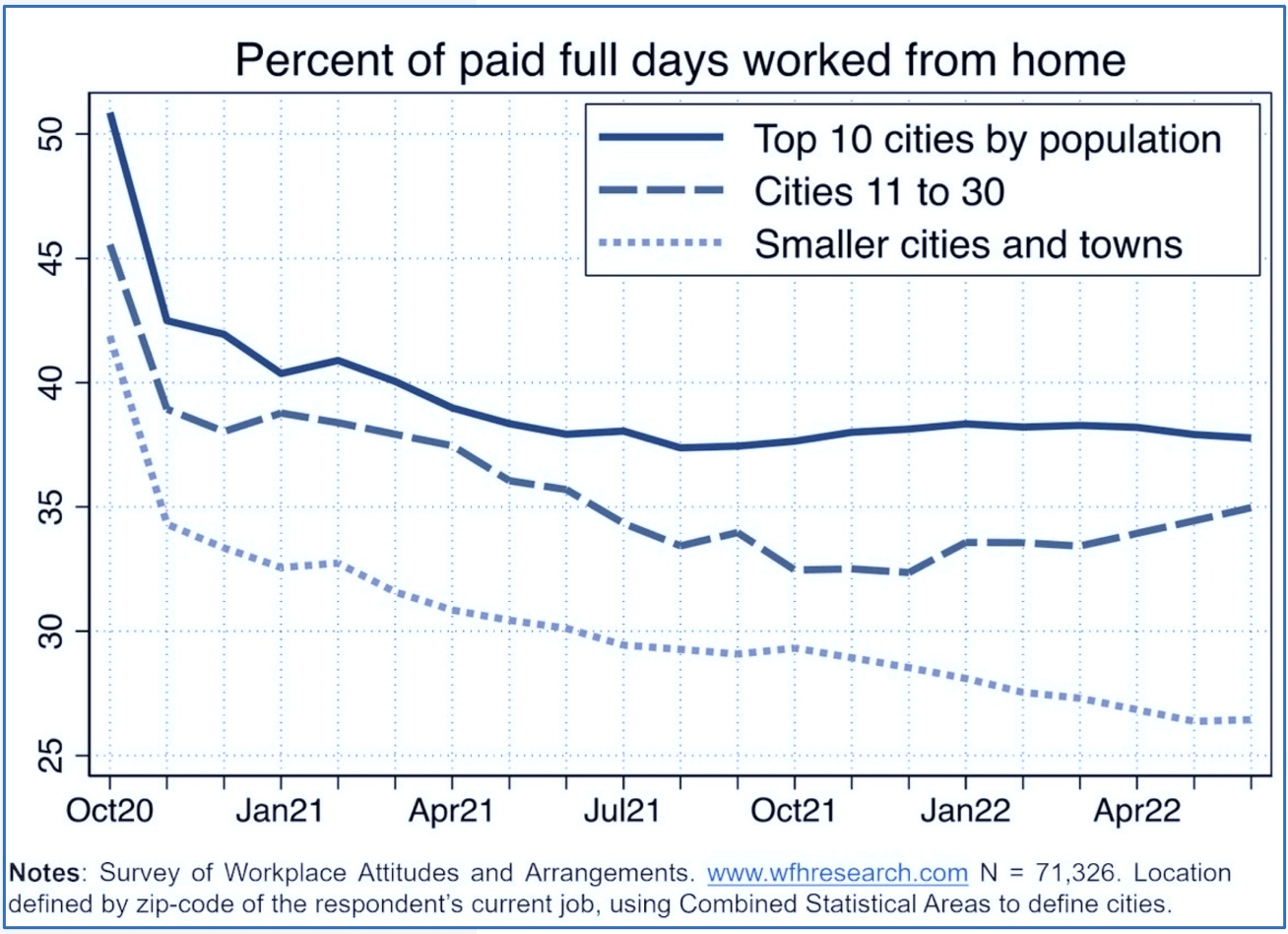

Office: Today we published Office REITs: It's All About The Commute on the Income Builder Marketplace which discussed our updated outlook and recent allocations in the office REIT sector. The 'Return to the Office' is here - but it's underwhelming. Despite 80% of employees currently in post-pandemic work arrangements, office utilization rates have remained 40-60% below pre-pandemic levels. Office leasing activity has remained surprisingly resilient at just 10% below pre-pandemic levels - as have office REIT earnings results - but corporations won't pay for half-empty space indefinitely. As projected, commute times have been the key variable explaining significant differences in WFH adoption across regions. Workers don't necessarily dislike the office, but long commutes more than offset any productivity gains. The outlook remains far sunnier in the Sunbelt and in secondary markets with net population growth, shorter commute times, and a more favorable industry mix.

Earlier this week, we published our REIT Earnings Preview which discusses the major themes and metrics we'll be watching across each of the major property sectors this earnings season. Since the start of last earnings season, the Equity REIT Index has declined 16%, slightly lagging the 12% decline in the S&P 500 during this time while the 10-Year Yield is essentially after a brief surge to 3.50%. The past quarter has seen a reversal in property sector performance trends since early in 2022 with interest-rate-sensitive REITs catching a bid while pro-cyclical REITs have lagged on recession concerns.

Mortgage REIT Daily Recap

Per the REIT Rankings Tracker available to Income Builder subscribers, mortgage REITs finished modestly lower amid an otherwise strong week of gains as residential mREITs slipped 0.4% today while commercial mREITs declined 0.5%. Hannon Armstrong (HASI) dipped more than 3% after a second firm - Jehoshaphat Research - released a short report on the renewal energy lender. The report - which focuses on the impact of rising interest rates on HASI's ability to cover its dividend - follows a Muddy Waters report in the prior week focused on its accounting practices that had sent HASI plunging by over 15%. HASI called the Muddy Waters allegations last week "deceptive" and said that it believes that its accounting is fully compliant and is an accurate representation of its financial performance. HASI also said it has sufficient portfolio cash flow to pay its dividend.

REIT Preferreds & Capital Raising

Per the Income Builder Preferred Tracker available to Income Builder subscribers, REIT Preferred stocks finished lower by 0.05% today, on average. REIT Preferreds are lower by roughly 10% on a total return basis this year after ending 2021 with price returns of roughly 8.0% and total returns of roughly 14%. There are now roughly 180 REIT-issued exchange-listed preferred and debt securities with an average current yield of 6.97%.

Economic Data This Week

We'll publish a full analysis and commentary of this week's developments in the real estate industry, as well as an analysis of the busy week of economic data in our Real Estate Weekly Outlook published this weekend.

Disclosure: Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index. Index definitions and a complete list of holdings are available on our website.

Hoya Capital Research & Index Innovations (“Hoya Capital”) is an affiliate of Hoya Capital Real Estate, a registered investment advisory firm based in Rowayton, Connecticut that provides investment advisory services to ETFs, individuals, and institutions. Hoya Capital Research & Index Innovations provides non-advisory services including market commentary, research, and index administration focused on publicly traded securities in the real estate industry.

This published commentary is for informational and educational purposes only. Nothing on this site nor any commentary published by Hoya Capital is intended to be investment, tax, or legal advice or an offer to buy or sell securities. This commentary is impersonal and should not be considered a recommendation that any particular security, portfolio of securities, or investment strategy is suitable for any specific individual, nor should it be viewed as a solicitation or offer for any advisory service offered by Hoya Capital Real Estate. Please consult with your investment, tax, or legal adviser regarding your individual circumstances before investing.

The views and opinions in all published commentary are as of the date of publication and are subject to change without notice. Information presented is believed to be factual and up-to-date, but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. Any market data quoted represents past performance, which is no guarantee of future results. There is no guarantee that any historical trend illustrated herein will be repeated in the future, and there is no way to predict precisely when such a trend will begin. There is no guarantee that any outlook made in this commentary will be realized.

Readers should understand that investing involves risk and loss of principal is possible. Investments in real estate companies and/or housing industry companies involve unique risks, as do investments in ETFs. The information presented does not reflect the performance of any fund or other account managed or serviced by Hoya Capital Real Estate. An investor cannot invest directly in an index and index performance does not reflect the deduction of any fees, expenses or taxes.

Hoya Capital Real Estate and Hoya Capital Research & Index Innovations have no business relationship with any company discussed or mentioned and never receives compensation from any company discussed or mentioned. Hoya Capital Real Estate, its affiliates, and/or its clients and/or its employees may hold positions in securities or funds discussed on this website and our published commentary. A complete list of holdings and additional important disclosures is available at www.HoyaCapital.com.