REIT Dividend Hikes • PPI Cools • Rally Fizzles

- U.S. equity markets finished little-changed Thursday - erasing an early-session gain following another cooler-than-expected inflation report - amid investor skepticism over the sustainability and pace of cooling inflation.

- Following gains of more than 2% yesterday, the S&P 500 slipped 0.1% today but the Mid-Cap 400 and Small-Cap 600 each held onto gains of 0.6% while technology stocks lagged.

- Real estate equities were mixed as well today as strong gains from pro-cyclical property sectors offset weakness from technology REITs. The Equity REIT Index slipped 0.2% with 11-of-18 property sectors.

- Kite Realty (KRG) - which last week we named one of our three "Best Ideas in Real Estate" - was among the leaders today after it raised its quarterly dividend for the third time this year to $0.22/share, a 4.8% increase from its prior dividend and a 33% increase from its third quarter dividend last year.

- Investors received more good news on the inflation front as the wholesale prices fell in July for the first time in two years as plunging commodities prices resulting from slowing global economic growth cooled the pace of inflation.

Real Estate Daily Recap

U.S. equity markets finished little-changed Thursday - erasing an early-session gain following another cooler-than-expected inflation report - amid investor skepticism over the sustainability and pace of cooling inflation. Following gains of more than 2% yesterday, the S&P 500 slipped 0.1% today but the Mid-Cap 400 and Small-Cap 600 each held onto gains of 0.6%. Real estate equities were mixed as well today as strong gains from pro-cyclical property sectors offset weakness from technology REITs. The Equity REIT Index slipped 0.2% with 11-of-18 property sectors in positive territory while the Mortgage REIT Index declined 0.2% while homebuilders and the broader Hoya Capital Housing Index delivered a second day of outperformance.

Following the cooler-than-expected CPI report on Wednesday, investors received more good news on the inflation front as the wholesale prices fell in July for the first time in two years as plunging commodities prices resulting from slowing global economic growth cooled the pace of inflation. The headline Producer Price Index fell 0.5% from June - its first month-over-month decrease since April 2020 - and significantly better than the expected increase of 0.2%. On a year-over-year basis, the index is higher by 9.8% - its the lowest rate since October 2021 - and snapping a record streak of seven months of double-digit inflation. Despite the cooler-than-expected report, bonds were under pressure with the 10-Year Treasury Yield jumping 10 basis points to 2.89% as Crude Oil prices rebounded on reports showing tightening inventory levels and oil production outages in the Gulf of Mexico.

Real Estate Daily Recap

Best & Worst Performance Today Across the REIT Sector

Shopping Center: Kite Realty (KRG) - which last week we named one of our three "Best Ideas in Real Estate" - was among the leaders today after it raised its quarterly dividend for the third time this year to $0.22/share, a 4.8% increase from its prior dividend and a 33% increase from its third quarter dividend last year. Earnings results from shopping center REITs were highly impressive as fundamentals are now as strong – if not stronger - than before the pandemic with occupancy rates climbing to the highest level since early 2015 while rental rates have continued to accelerate despite the broader economic slowdown. Elsewhere, small-cap mall REIT CBL Properties (CBL) - which emerged from Chapter 11 bankruptcy last year - reinstated its quarterly dividend at $0.25/share. We've now seen 87 REITs raise their dividends in 2022 while 6 REITs have lowered their payouts.

Homebuilders: Today, we published Homebuilders: Short Term Pain, Long-Term Gain which discussed our updated outlook for the sector and recent portfolio allocations. Those looking for a deep value “contrarian play” need not look much further than the homebuilders, which are perhaps the most unloved industry group across the entire equity market. This sharply bearish sentiment comes on the heels of a historically strong year of operating performance for the industry as robust demand clashed with tight inventory levels resulting from a decade of underbuilding. These discounted valuations may have been justified if mortgage rates continued their extraordinary surge seen in early 2022, a surge that rapidly turned the housing market from red-hot to icy-cold. While not out of the woods yet given the ongoing uncertainty over the path of inflation - which ultimately dictates the path of Fed policy and mortgage rates - we believe that the risk-reward for the homebuilding sector is now skewed heavily to the upside.

Earlier this week we published our REIT Earnings Recap: Rents Paid, Dividends Raised. The U.S. REIT industry - which remains relatively "early" in its post-pandemic recovery - exhibited few signs of softness in the second quarter even as the U.S. entered a technical recession. Earnings results from residential, self-storage, and shopping center REITs were most impressive, followed closely behind by industrial and net lease REITs. Office REITs were the lone weak spot among major sectors. Nearly two-thirds of REITs raised their full-year guidance. Strong results from REITs come amid an otherwise disappointing earnings season for the broader equity market in which less than 50% of S&P 500 companies raised their 2022 earnings outlook.

Mortgage REIT Daily Recap

Per the REIT Rankings Tracker available to Income Builder subscribers, mortgage REITs were mixed today with residential mREITs advancing 0.5% while commercial mREITs slipped 0.6%. Ellington Residential (EARN) was among the outperformers today after it wrapped up mREIT earnings season with a decent report with EPS matching analyst estimates. EARN noted that its book value per share ("BVPS") dipped 10.6% in Q2 - roughly matching the sector average - as the "challenges of the previous quarter intensified during the second quarter" but noted that the wider yield spreads "have been a tailwind for earnings." EARN noted that it had a strong July "as interest rate volatility subsided somewhat and Agency yield spreads retraced a portion of their second quarter widening." As discussed in our REIT Earnings Recap, mortgage REITs have rebounded sharply since mid-June as mortgage-backed bonds (MBB) have caught a bid following a brutal first-half of 2022.

REIT Preferreds & Capital Raising

Per the Income Builder Preferred Tracker available to Income Builder subscribers, REIT Preferred stocks finished lower by 0.21% today, on average. REIT Preferreds are lower by roughly 5% on a total return basis this year after ending 2021 with price returns of roughly 8.0% and total returns of roughly 14%. There are now roughly 180 REIT-issued exchange-listed preferred and debt securities with an average current yield of roughly 6.75%. In the REIT primary capital markets today, net lease REIT Broadstone (BNL) slipped after announcing a secondary offering of 13M common shares.

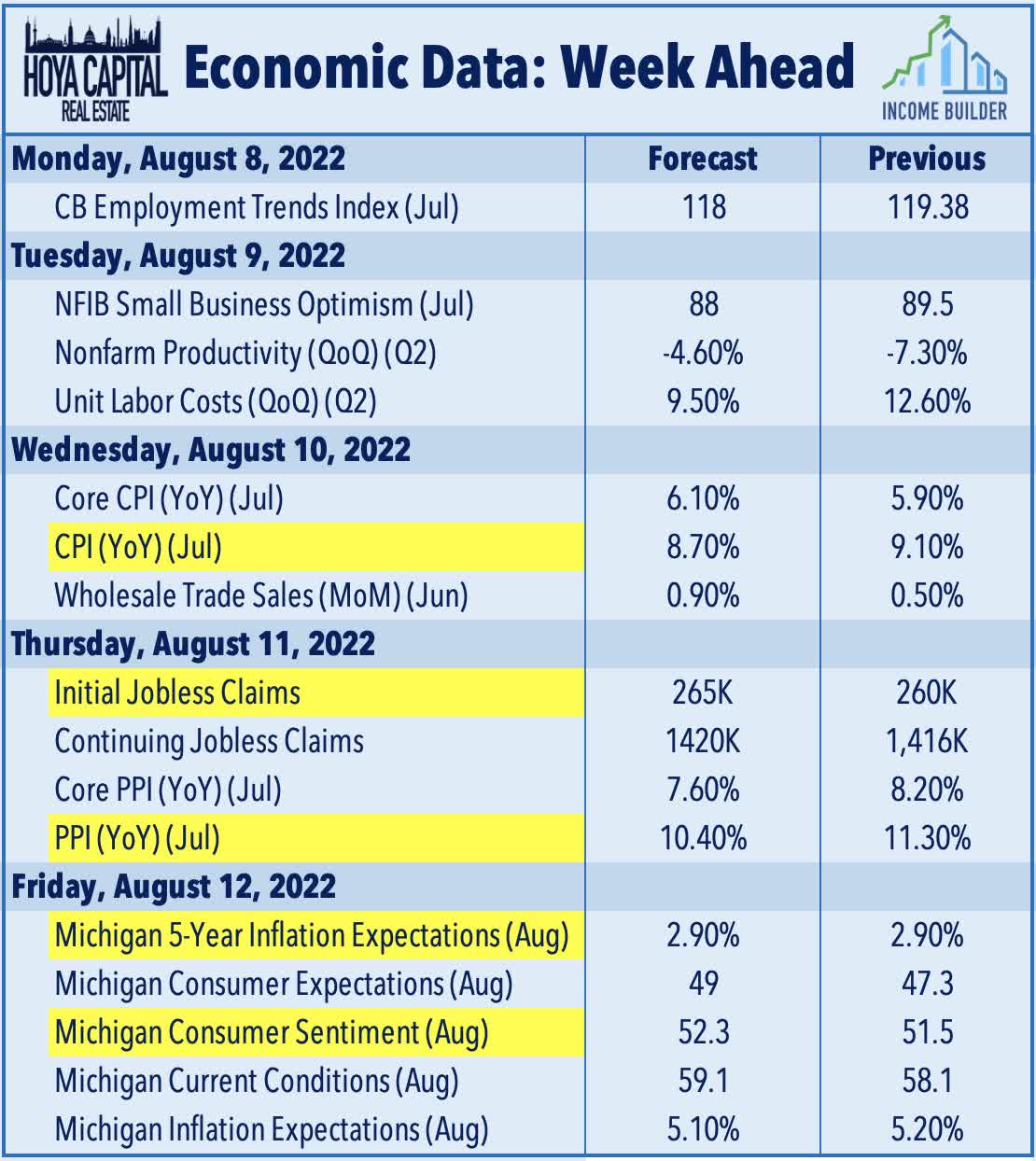

Economic Data This Week

The busy week of inflation data wraps up on Friday with our first look at Michigan Consumer Sentiment for August which includes the inflation expectations survey. Last month, sentiment fell to the lowest level in more than 10 years as persistent inflation and worries over economic growth have weighed on confidence. The Fed is particularly interested in the 5-Year Inflation Expectations survey, looking for signs of a potential "wage-price inflation spiral" through elevated consumer wage expectations.

Disclosure: Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index. Index definitions and a complete list of holdings are available on our website.

Hoya Capital Research & Index Innovations (“Hoya Capital”) is an affiliate of Hoya Capital Real Estate, a registered investment advisory firm based in Rowayton, Connecticut that provides investment advisory services to ETFs, individuals, and institutions. Hoya Capital Research & Index Innovations provides non-advisory services including market commentary, research, and index administration focused on publicly traded securities in the real estate industry.

This published commentary is for informational and educational purposes only. Nothing on this site nor any commentary published by Hoya Capital is intended to be investment, tax, or legal advice or an offer to buy or sell securities. This commentary is impersonal and should not be considered a recommendation that any particular security, portfolio of securities, or investment strategy is suitable for any specific individual, nor should it be viewed as a solicitation or offer for any advisory service offered by Hoya Capital Real Estate. Please consult with your investment, tax, or legal adviser regarding your individual circumstances before investing.

The views and opinions in all published commentary are as of the date of publication and are subject to change without notice. Information presented is believed to be factual and up-to-date, but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. Any market data quoted represents past performance, which is no guarantee of future results. There is no guarantee that any historical trend illustrated herein will be repeated in the future, and there is no way to predict precisely when such a trend will begin. There is no guarantee that any outlook made in this commentary will be realized.

Readers should understand that investing involves risk and loss of principal is possible. Investments in real estate companies and/or housing industry companies involve unique risks, as do investments in ETFs. The information presented does not reflect the performance of any fund or other account managed or serviced by Hoya Capital Real Estate. An investor cannot invest directly in an index and index performance does not reflect the deduction of any fees, expenses or taxes.

Hoya Capital Real Estate and Hoya Capital Research & Index Innovations have no business relationship with any company discussed or mentioned and never receives compensation from any company discussed or mentioned. Hoya Capital Real Estate, its affiliates, and/or its clients and/or its employees may hold positions in securities or funds discussed on this website and our published commentary. A complete list of holdings and additional important disclosures is available at www.HoyaCapital.com.