Jobs Report • REIT Earnings • Dividend Hikes

- U.S. equity markets rebounded Friday- clawing back some of the sharp weekly declines- after lukewarm employment data showed that while hiring has slowed in recent months, labor markets remain historically tight.

- Cutting its weekly declines to 3.3%, the S&P 500 rebounded 1.4% today while the tech-heavy Nasdaq 100 advanced 1.6% - cutting its weekly losses to under 6%.

- Real estate equities were among the better-performers today following a strong slate of earnings reports and a trio of dividend hikes. Equity REITs advanced 1.4% while Mortgage REITs rallied 3.8%.

- Shopping Center REIT Regency Centers (REG) - which we own in the REIT Dividend Growth Portfolio - rallied nearly 6% after boosting its full-year FFO and NOI outlook while also raising its dividend by 4%.

- Mortgage REIT Arbor Realty (ABR) - which we own in the REIT Focused Income Portfolio - surged more than 10% today after reporting strong Q3 results and raising its dividend for the fourth time this year.

Income Builder Daily Recap

U.S. equity markets rebounded Friday - clawing back some of the sharp weekly declines - after lukewarm employment data showed that while hiring has slowed in recent months, labor markets remain historically tight. Cutting its weekly declines to 3.3%, the S&P 500 rebounded 1.4% today while the tech-heavy Nasdaq 100 advanced 1.6% - cutting its weekly losses to under 6%. Consistent with a theme throughout the week, the Mid-Cap 400 and Small-Cap 600 modestly outperformed the large-cap indexes. Real estate equities were also among the better-performers today following a strong slate of earnings reports and a trio of dividend hikes. The Equity REIT Index advanced 1.4% today with 15-of-18 property sectors in positive territory while the Mortgage REIT Index rallied 3.8% and Homebuilders gained 2.8%.

Real Estate Daily Recap

Best & Worst Performance Today Across the REIT Sector

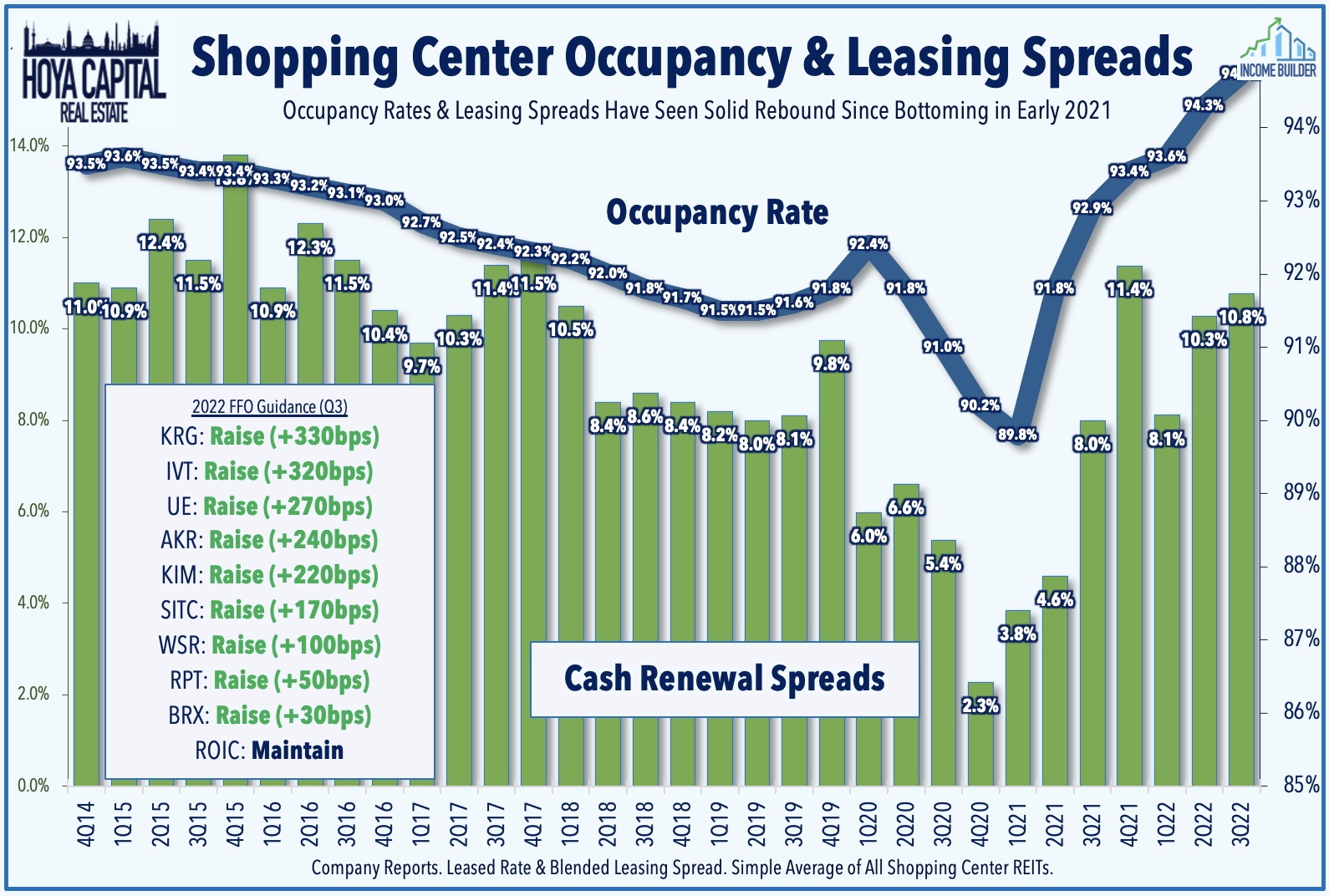

Shopping Center: The strong earnings season for shopping center REITs concluded on a high note with a trio of very upbeat reports. Regency Centers (REG) - which we own in the REIT Dividend Growth Portfolio - rallied nearly 6% after reporting better-than-expected results and raising its full-year FFO and NOI outlook while raising its dividend by 4%. Lifted by another strong quarter of leasing demand, Regency lifted its full-year FFO growth outlook by 190 basis points. Federal Realty (FRT) also rallied nearly 6% after reporting similarly strong results and raising its full-year FFO outlook by 220 basis points. Phillips Edison (PECO) advanced 4% after hiking its FFO growth outlook by 90 basis points while recording impressive leasing spreads of 16.9%. Across the sector, occupancy rates improved by an average of 40 basis points sequentially and 140 basis points from last year to new record-highs.

Net Lease: The strong earnings season for net lease REITs continued as well over the past 24 hours. WP Carey (WPC) - which we own in the REIT Focused Income Portfolio - rallied more than 3% after reporting better-than-expected results driven by record-high rent growth driven by CPI adjustments. WPC - which owns the most inflation-hedged portfolio among net lease REITs - commented, "As current CPI numbers flow through to rents, we expect our same-store growth to move even higher in 2023, and to continue seeing the benefits into 2024." WPC now expects FFO growth of 5.0% this year - up 40 basis points from its prior outlook - and is one of seven net lease REITs to raise its full-year outlook this quarter despite the headwind from higher rates.

Apartment: Apartment Income (AIRC) - which we own in the REIT Focused Income Portfolio - was among the better-performers in the sector today after reporting better-than-expected results and raising its full-year NOI growth outlook while reiterating its FFO target. Leasing results from AIRC were notably stronger than its coastal-focused peers, reporting 14.0% blended spreads in Q3 and 12.9% in October while recording an impressive 640 basis point decline in turnover rates - each among the best in the sector. AvalonBay (AVB) slipped 2% after reporting relatively weaker results and revising lower its full-year FFO and NOI growth outlook. Of note, AVB was the lone apartment REIT this earnings season to downward revise its full-year outlook lower across FFO and same-store revenues, expenses, and NOI. On the upside, AVB did also record a year-over-year decline in turnover rates.

Billboard: Lamar Advertising (LAMR) slipped about 1% after reporting results that were roughly in line with estimates while noting that its "tracking to the top of our previously provided guidance range for full-year diluted AFFO per share." LAMR cited strong political ad spending as a key driver of revenue growth in Q3 and into early Q4, contributing 210 basis points of the total sales growth of 7.6% in October. LAMR did note relative weakness in demand from national brands with its national/programmatic segment growing just 0.3% in Q3 while its local business grew 6.4%. Outfront (OUT) dipped more than 3% after reporting that its billboard business continues to outperform its transit business - primarily through its major deal with the New York MTA, which continues to operate at "essentially breakeven" levels.

Mortgage REIT Daily Recap

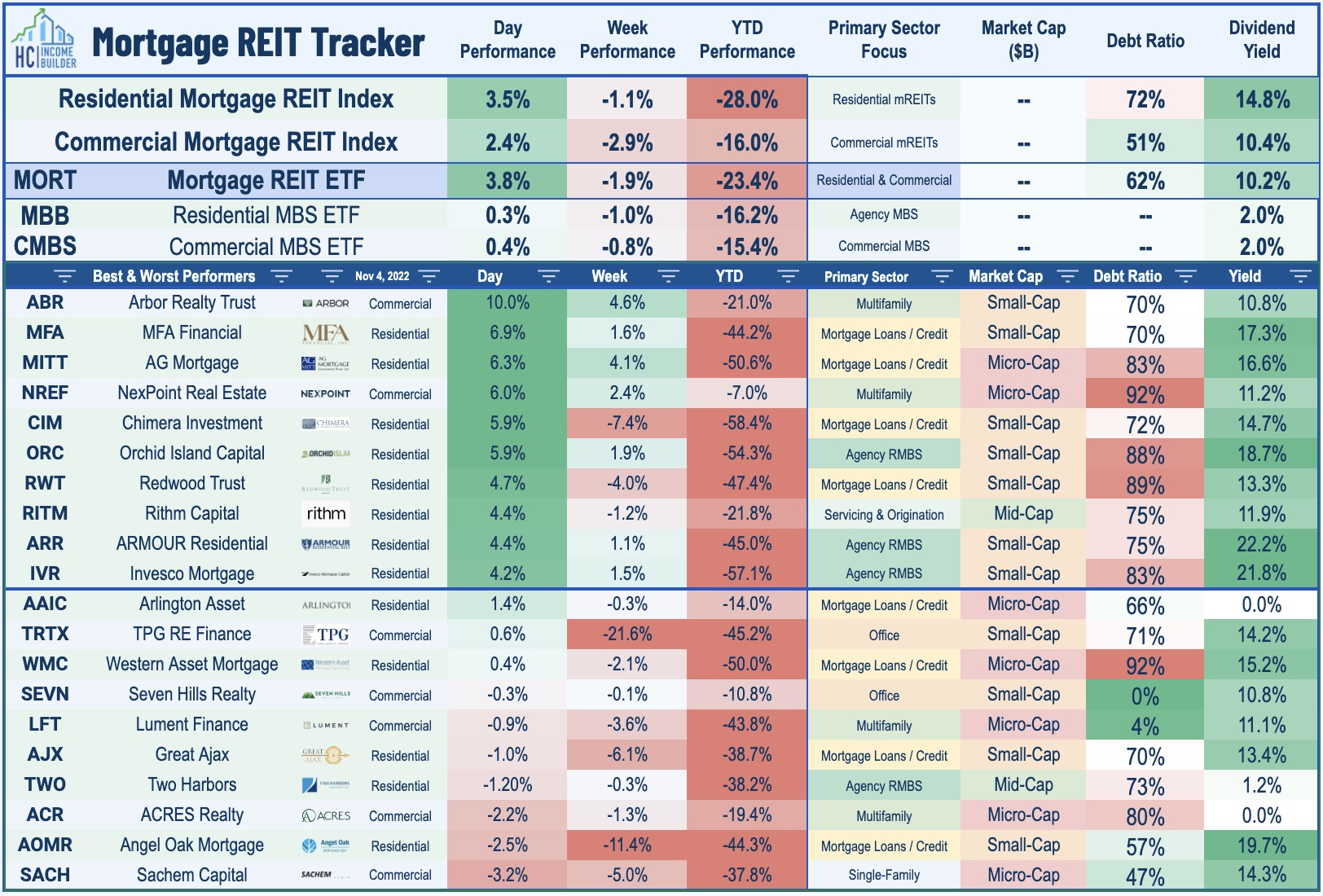

Per the REIT Rankings Tracker available to Income Builder subscribers, mortgage REITs rallied today after a strong slate of earnings reports. Arbor Realty (ABR) - which we own in the REIT Focused Income Portfolio - surged more than 10% today after reporting strong Q3 results and raising its dividend for the fourth time this year. Hannon Armstrong (HASI) advanced nearly 4% after reporting better-than-expected results and affirming its guidance that Distributable Earnings Per Share is expected to grow at a compound annual rate of 10% to 13% from 2021 to 2024, relative to the 2020 baseline of $1.55 per share. Great Ajax (AJX) slipped about 1% after reporting in-line results with its Book Value Per Share ("BVPS") declining 8.2% to $13.75 in Q3. Western Asset (WMC) advanced 1% despite reporting a sector-worst 30% decline in its BVPS, but noted that it remains committed to "pay dividends that are supported by the long-term earnings power of the portfolio." ACRES Commercial (ACR) slipped 2% despite reporting that its BVPS advanced 2% in Q3, among the best in the sector thus far.

Disclosure: Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index. Index definitions and a complete list of holdings are available on our website.

Hoya Capital Research & Index Innovations (“Hoya Capital”) is an affiliate of Hoya Capital Real Estate, a registered investment advisory firm based in Rowayton, Connecticut that provides investment advisory services to ETFs, individuals, and institutions. Hoya Capital Research & Index Innovations provides non-advisory services including market commentary, research, and index administration focused on publicly traded securities in the real estate industry.

This published commentary is for informational and educational purposes only. Nothing on this site nor any commentary published by Hoya Capital is intended to be investment, tax, or legal advice or an offer to buy or sell securities. This commentary is impersonal and should not be considered a recommendation that any particular security, portfolio of securities, or investment strategy is suitable for any specific individual, nor should it be viewed as a solicitation or offer for any advisory service offered by Hoya Capital Real Estate. Please consult with your investment, tax, or legal adviser regarding your individual circumstances before investing.

The views and opinions in all published commentary are as of the date of publication and are subject to change without notice. Information presented is believed to be factual and up-to-date, but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. Any market data quoted represents past performance, which is no guarantee of future results. There is no guarantee that any historical trend illustrated herein will be repeated in the future, and there is no way to predict precisely when such a trend will begin. There is no guarantee that any outlook made in this commentary will be realized.

Readers should understand that investing involves risk and loss of principal is possible. Investments in real estate companies and/or housing industry companies involve unique risks, as do investments in ETFs. The information presented does not reflect the performance of any fund or other account managed or serviced by Hoya Capital Real Estate. An investor cannot invest directly in an index and index performance does not reflect the deduction of any fees, expenses or taxes.

Hoya Capital Real Estate and Hoya Capital Research & Index Innovations have no business relationship with any company discussed or mentioned and never receives compensation from any company discussed or mentioned. Hoya Capital Real Estate, its affiliates, and/or its clients and/or its employees may hold positions in securities or funds discussed on this website and our published commentary. A complete list of holdings and additional important disclosures is available at www.HoyaCapital.com.