Goldilocks Returns? • Stocks Rally • Hotel REIT Updates

- U.S. equity markets rallied Friday while benchmark interest rates dipped after the closely-watched nonfarm payrolls report showed a slowdown in wage growth consistent with a broader cooling of inflationary pressures.

- Snapping a three-week losing streak with cumulative weekly gains of 1.5%, the S&P 500 advanced 2.3% today while the tech-heavy Nasdaq 100 rallied nearly 3%.

- Real estate equities - one of the more yield-sensitive segments of the market - were among the leaders today and for the week. The Equity REIT Index rallied 2.7% today.

- The December payrolls report showed that despite stronger-than-expected job growth, wages rose at the slowest pace since August 2021, providing evidence that a cooldown in inflationary pressures may not require a further intensification of monetary tightening.

- Braemar Hotels (BHR) surged nearly 9% today after it announced preliminary fourth-quarter results, noting that it achieved RevPAR levels that were 20% above the pre-pandemic comparable levels from 2019.

Income Builder Daily Recap

U.S. equity markets rallied Friday while benchmark interest rates dipped after the closely-watched BLS nonfarm payrolls report showed a slowdown in wage growth consistent with a broader cooling of inflationary pressures. Snapping a three-week losing streak with cumulative weekly gains of 1.5%, the S&P 500 advanced 2.3% today while the tech-heavy Nasdaq 100 rallied nearly 3%. Real estate equities - one of the more yield-sensitive segments of the market - were among the leaders today and for the week. The Equity REIT Index rallied 2.7% today with all 18 property sectors in positive-territory while the Mortgage REIT Index advanced 1.7%. The dip in benchmark rates was especially welcome news for homebuilders and the broader Hoya Capital Housing Index, which gained 2.6% today and nearly 5% this week.

Concluding a busy week of employment data, the critical BLS nonfarm payrolls report this morning showed that the U.S. economy added 223k jobs in December - above consensus estimates of roughly 200k. Despite a decline in the unemployment rate to just 3.5%, however, average hourly earnings rose at the slowest pace since August 2021, providing evidence that a cooldown in inflationary pressures may not require a further intensification of monetary tightening. Hopes of a potential 'soft landing' sparked a broad-based bid for bonds across the credit and maturity curve with the 10-Year Treasury Yield (US10Y) dipping over 30 basis points on the week while the policy-sensitive 2-Year Treasury Yield (US2Y) plunged nearly 20 basis points on the week.

We'll publish a full analysis and commentary of this week's developments in the real estate industry, as well as an analysis of the busy week of economic data in our Real Estate Weekly Outlook this weekend.

Real Estate Daily Recap

Best & Worst Performance Today Across the REIT Sector

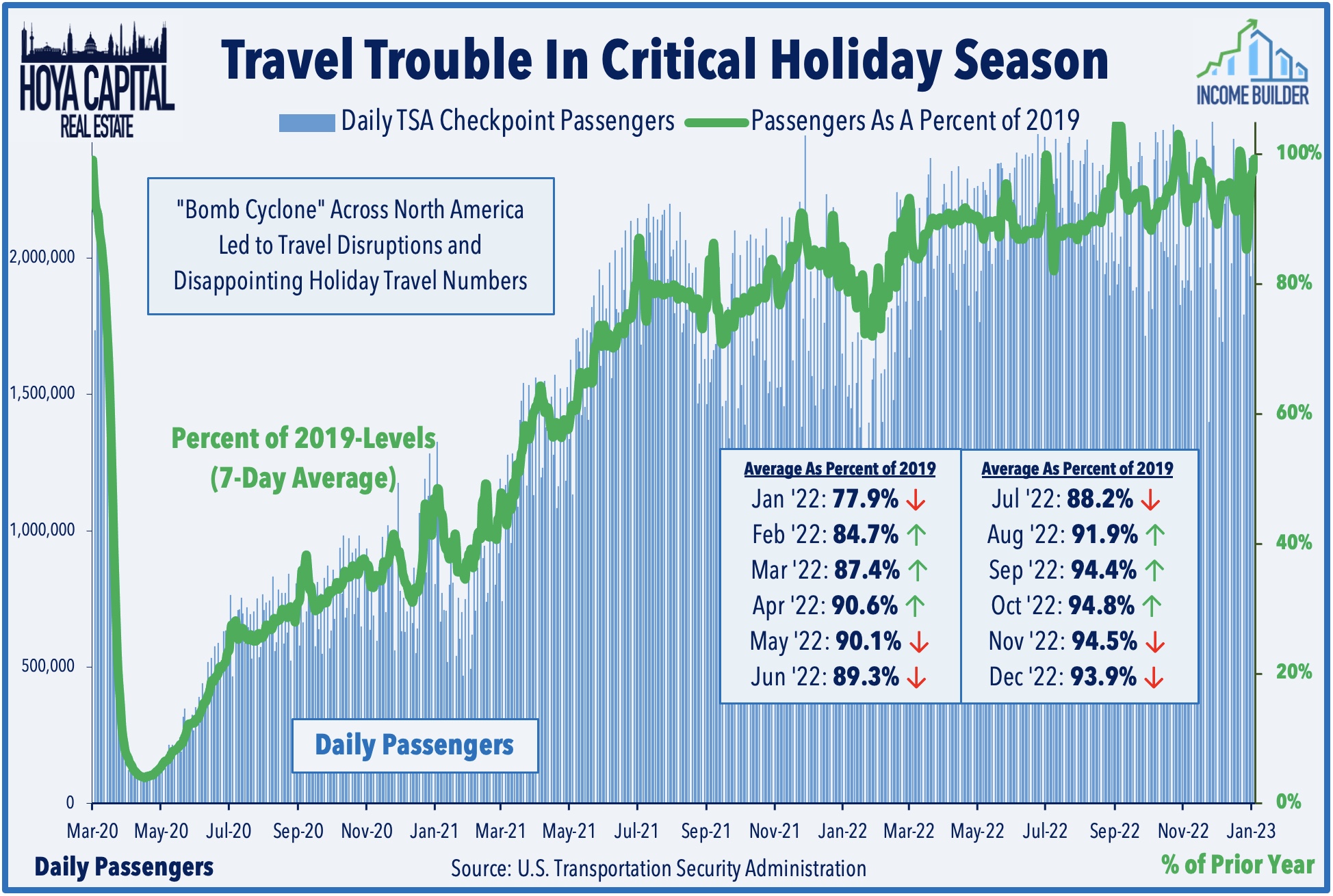

Hotels: Braemar Hotels (BHR) surged nearly 9% today after it announced preliminary fourth-quarter results, noting that it achieved RevPAR levels that were 20% above the pre-pandemic comparable levels from 2019. December was a particularly strong month for BHR with comparable RevPAR increasing 26% over 2019-levels, up from the 15% relative increase in November and 14% increase in December. Ashford Hotels (AHT) advanced nearly 5% after it reported that its fourth-quarter RevPAR was 1% below comparable 2019 levels with a similar trajectory of improvement in December compared with the two prior months. Recent TSA checkpoint data shows that passenger throughput finished the holiday season relatively strong around the New Year Holiday with the 30-Day average hovering around 99% of pre-pandemic levels.

Healthcare: Senior Housing REITs - notably Welltower (WELL) and Ventas (VTR) - were also broadly higher today following the release of the fourth-quarter NIC Map Vision report by the National Investment Center for Seniors Housing. The report showed that Senior Housing occupancy increased for a sixth-straight quarter to 83%, which is up 5.2% from the pandemic occupancy low of 77.8% in 2Q21 - but still below the pre-pandemic levels of roughly 90%. Despite the reduced occupancy levels, SH operators have exhibited strong pricing power with annual rent growth climbing to 4.9% in Q4 - the largest increase since NIC Map Vision data was reported starting in 2006. Higher demand and slower inventory growth were consistent trends throughout 2022 with NIC noting that just 11,000 units were added within NIC MAP Primary Markets last year, the weakest inventory growth since 2014. Elsewhere, LTC Properties (LTC) gained 2% after it announced a $128M deal for 12 assisted living/memory care properties in North Carolina.

Additional Headlines from The Daily REITBeat on Income Builder

- Acadia Realty (AKR) reported that it will not recognize its share of the Albertson's Special Dividend in fiscal year 2022 and is therefore reducing its full year 2022 guidance to $1.17-1.19/share from $1.28-$1.30/share.

- American Assets (AAT) and Sabra Healthcare (SBRA) announced amended credit facilities.

- Gladstone Commercial (GOOD) announced a business update commenting that 100% of Q4 2022 cash base rents have been paid and collected while portfolio occupancy is at 96.8%.

- Fitch Ratings assigned a “BBB-“ rating to Getty (GTY) senior unsecured notes (Series O, P, and Q) with a stable outlook

- Baird upgraded Eastgroup (EGP), Hudson Pacific (HPP), and Regency Centers (REG) to Outperform from Neutral

- We're excited to announce that Armada ETF Advisors is a new contributing author on Income Builder. Members now receive access to Armada's insights and analysis focused on residential REITs.

Mortgage REIT Daily Recap

Per the REIT Rankings Tracker available to Income Builder subscribers, mortgage REITs continued their strong week with residential mREITs gaining another 1.2% today - pushing their weekly gains to nearly 7% - while commercial mREITs gained 1.8% to push their weekly gain to nearly 5%. Broadmark Realty (BRMK) finished higher by 3% today despite announcing that it received a letter from NYSE indicating that the exchange has commenced proceedings to delist its warrants based on their low selling price. The delisting does not affect its common stock. Last month, we published Mortgage REITs: High Yields Are Fine, For Now, which noted that despite paying average dividend yields in the mid-teens, the majority of mREITs have been able to cover their dividends, but we flagged a handful of mREITs with payout ratios above 100% of EPS.

Disclosure: Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index. Index definitions and a complete list of holdings are available on our website.

Hoya Capital Research & Index Innovations (“Hoya Capital”) is an affiliate of Hoya Capital Real Estate, a registered investment advisory firm based in Rowayton, Connecticut that provides investment advisory services to ETFs, individuals, and institutions. Hoya Capital Research & Index Innovations provides non-advisory services including market commentary, research, and index administration focused on publicly traded securities in the real estate industry.

This published commentary is for informational and educational purposes only. Nothing on this site nor any commentary published by Hoya Capital is intended to be investment, tax, or legal advice or an offer to buy or sell securities. This commentary is impersonal and should not be considered a recommendation that any particular security, portfolio of securities, or investment strategy is suitable for any specific individual, nor should it be viewed as a solicitation or offer for any advisory service offered by Hoya Capital Real Estate. Please consult with your investment, tax, or legal adviser regarding your individual circumstances before investing.

The views and opinions in all published commentary are as of the date of publication and are subject to change without notice. Information presented is believed to be factual and up-to-date, but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. Any market data quoted represents past performance, which is no guarantee of future results. There is no guarantee that any historical trend illustrated herein will be repeated in the future, and there is no way to predict precisely when such a trend will begin. There is no guarantee that any outlook made in this commentary will be realized.

Readers should understand that investing involves risk and loss of principal is possible. Investments in real estate companies and/or housing industry companies involve unique risks, as do investments in ETFs. The information presented does not reflect the performance of any fund or other account managed or serviced by Hoya Capital Real Estate. An investor cannot invest directly in an index and index performance does not reflect the deduction of any fees, expenses or taxes.

Hoya Capital Real Estate and Hoya Capital Research & Index Innovations have no business relationship with any company discussed or mentioned and never receives compensation from any company discussed or mentioned. Hoya Capital Real Estate, its affiliates, and/or its clients and/or its employees may hold positions in securities or funds discussed on this website and our published commentary. A complete list of holdings and additional important disclosures is available at www.HoyaCapital.com.