Carnage Continues • Mall Earnings • Data Center M&A?

- U.S. equity markets finished sharply lower Monday - extending a punishing sell-off across essentially all sectors - driven by mounting doubt over the Fed's ability to engineer a "soft landing."

- Posting its worst three-day slide since the March 2020 pandemic lows, the S&P 500 dipped another 3.2% today while the tech-heavy Nasdaq 100 declined nearly 4%.

- Real estate equities were also broadly lower as the Equity REIT Index dipped 4.4% today with all 19 property sectors in negative territory while Mortgage REITs declined by 3.5%.

- Ahead of the closely-watched report this afternoon from Simon Property (SPG), earnings results this morning from Macerich (MAC) were a bit disappointing as leasing spreads slipped in Q1, but tenant sales productivity showed notable improvement.

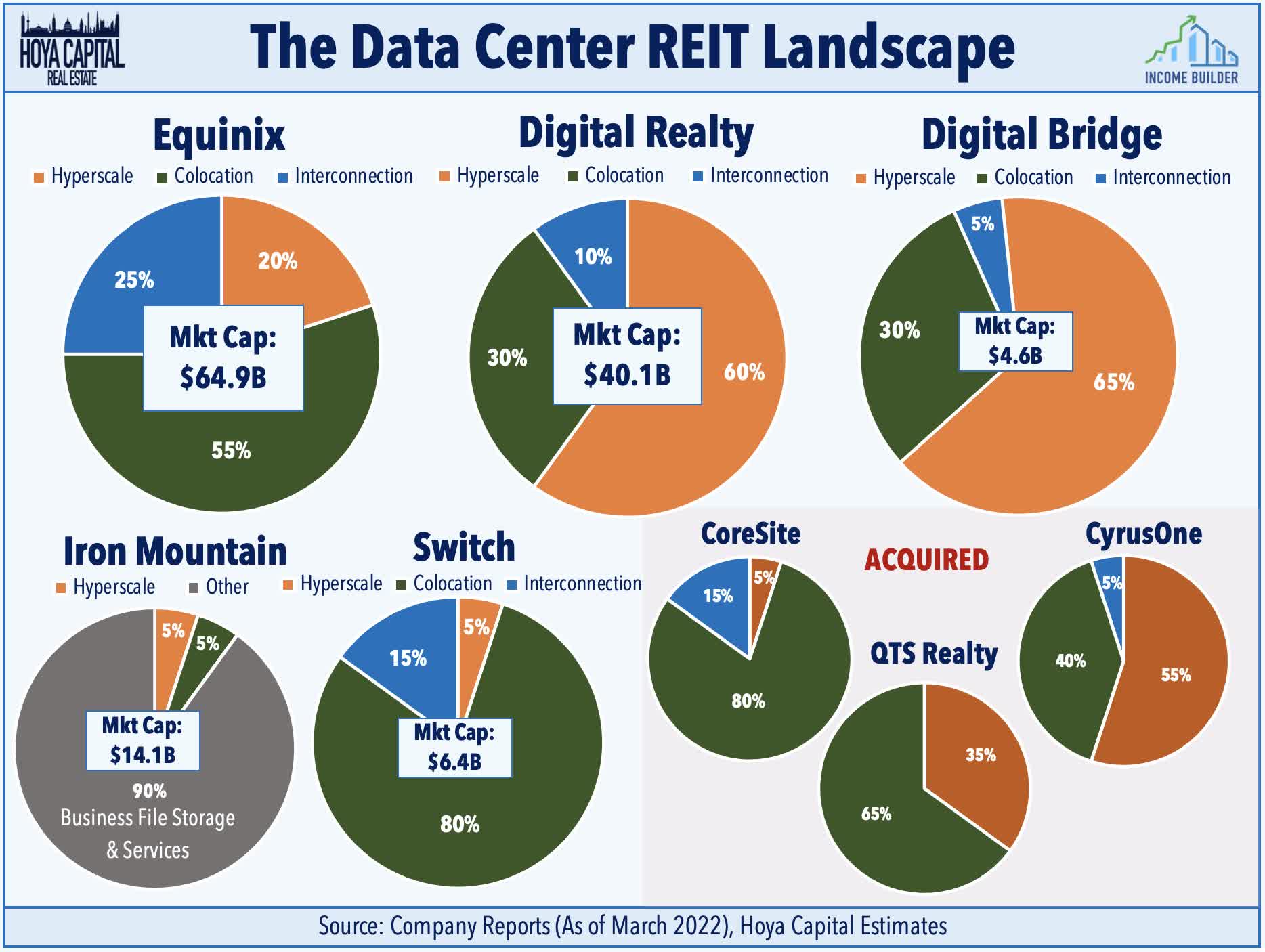

- Bloomberg reported this afternoon that Digital Bridge (DBRG) has emerged as a suitor for data center operator Switch (SWCH) and is reportedly competing against a unit of Brookfield Asset Management.

Income Builder Daily Recap

We recently launched Hoya Capital Income Builder - a premier income-focused investment research service through Seeking Alpha Marketplace - that will be the new exclusive home of all of Hoya Capital's investment research. Income Builder focuses on real income-producing asset classes that offer the opportunity for diversification, monthly income, capital appreciation, and inflation hedging. If you're not already on board, give us a try with a completely risk-free two-week trial and take a look around.

U.S. equity markets finished sharply lower Monday - extending a punishing sell-off across essentially all sectors - driven by mounting doubt over the Federal Reserve's ability to engineer a "soft landing." Posting its worst three-day slide since the March 2020 pandemic lows, the S&P 500 dipped another 3.2% today while the tech-heavy Nasdaq 100 declined nearly 4% to push its drawdown to over 26%. Real estate equities were also broadly lower as the Equity REIT Index dipped 4.4% today with all 19 property sectors in negative territory while Mortgage REITs declined by 3.5%.

Bonds did catch a bid today amid the carnage, however, as the 10-Year Treasury Yield pulled back 4 basis points while the 2-Year Treasury Yield dipped 10 basis points. Mortgage-backed bonds (MBB) exhibited notable strength on the day while IG corporate bonds (LQD) also gained ground. There were few places to hide in the equity market, however, as all eleven GICS equity sectors were lower today with notable declines from the Energy (XLE) sector as Crude Oil futures dipped 6% amid global demand concern. Also of note, Bitcoin slumped another 9% today and is now 50% off its recent highs.

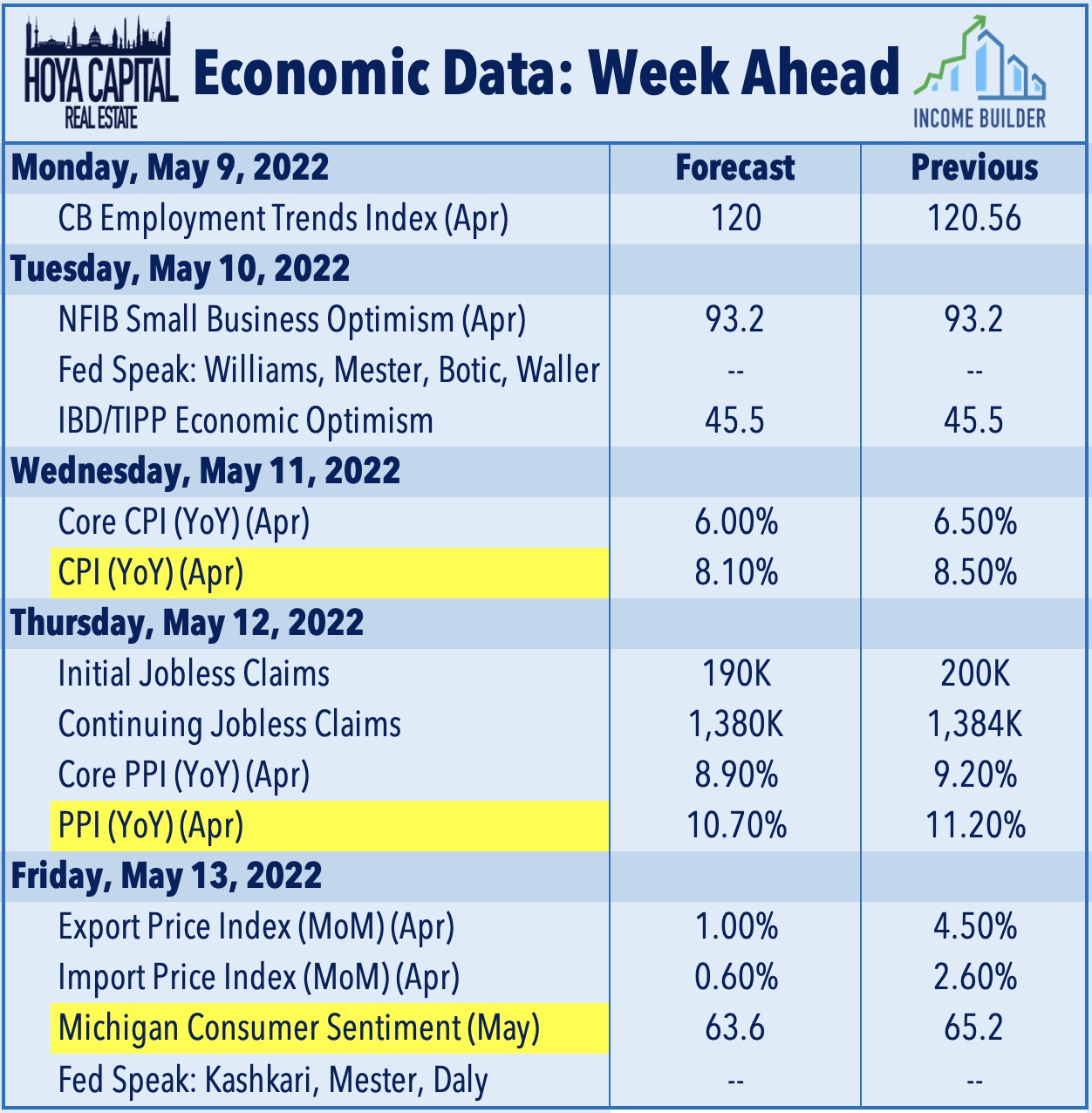

Inflation data and commentary from Fed members highlight the busy slate of economic data in the week ahead. On Wednesday, the BLS will report the Consumer Price Index which may potentially reveal that the fastest pace of year-over-year increases is finally behind us as both the headline and Core CPI is expected to show a cooldown in April to 8.1% and 6.0%, respectively. Similar themes are expected in the Producer Price Index report on Thursday is expected to show a 10.7% increase for the headline PPI, down from 11.2% in the prior month. On Friday, we'll also get our first look at Michigan Consumer Sentiment for May to see if the unexpected rebound in confidence seen last month can be sustained or if it resumes the downward trend that began last August amid persistent anxiety about inflation.

Real Estate Daily Recap

Today, we published our Real Estate Earnings Recap & Ratings Updates report for Income Builder members. Ahead of the final handful of earnings reports this week, we noted that results have generally been better-than-expected across most REIT sectors with nearly 70% of REITs that provide full-year guidance raising their FFO target. Results from residential and shopping center REITs were most impressive, followed closely by industrial and storage REITs while mortgage REITs have also been a bright spot amid the carnage over the past several weeks. Despite the strong slate of earnings reports across most property sectors performance trends continue to be dominated by macroeconomic factors.

Mall: Ahead of the closely-watched report this afternoon from Simon Property (SPG), earnings results this morning from Macerich (MAC) were a bit disappointing as leasing spreads took another leg lower in Q1 while its 230 basis point increase in occupancy from Q1 2021 trailed those of PREIT (+430) and Tanger (+260). MAC - which declined about 3% on the day - held the midpoint of its full-year FFO guidance unchanged, which calls for a 3.9% decline in FFO/share. Encouragingly, MAC did note that comparable tenant sales from spaces less than 10K square feet rose 14.5% from the year-ago quarter and were 11.5% higher than Q1 2019.

Data Center: Bloomberg reported this afternoon that Digital Bridge (DBRG) has emerged as a suitor for data center operator Switch (SWCH), citing people familiar with the matter. DBRG - which has emerged as a legit player in the data center space over the last year amid its "digital transformation" from its legacy Colony Capital portfolio towards a pure-play technology REIT - is reportedly competing against a unit of Brookfield Asset Management (BAM) for Switch, according to the Bloomberg report. Switch had planned to convert to a REIT for the 2023 fiscal year. The M&A boom in the space began last June when Blackstone (BX) acquired QTS Realty in a $10B deal, one of a half-dozen acquisitions over the past several years for its nontraded REIT portfolio. Then in November, KKR (KKR) and Global Infrastructure Partners announced a $15B deal to acquire CyrusOne. A week after that, American Tower (AMT) announced a $10B deal to acquire CoreSite.

In addition to Simon Property, we'll hear results from the final two dozen REITs this week including National Health Investors (NHI), BRT Apartment (BRT), and AIMCO (AIV) this afternoon. On Tuesday, we'll be watching results from senior housing REIT Welltower (WELL), single-family rental REIT Tricon (TCN), and data center operator Switch (SWCH). On Thursday, we'll hear results from net lease REIT Postal Realty (PSTL), cannabis REIT New Lake Capital (OTCQX:NLCP), and Southerly Hotels (SOHO), and on Friday, we'll hear results from New York City REIT (NYC).

Mortgage REIT Daily Recap

Per the REIT Rankings Tracker available to Income Builder subscribers, following a strong week of outperformance, mREITs were also broadly lower today ahead of the final stretch of earnings reports. Results over the past two weeks have been better-than-expected as residential mREITs reported an average decline in Book Value Per Share ("BVPS") of less than 8% - not as poor as the 10-15% declines expected - while commercial mREITs recorded a modest increase in BVPS. Small-cap mREITs were among the notable laggards today including Western Asset Mortgage (WMC) and Sachem Capital (SACH). We'll hear results from Broadmark Realty (BRMK), Cherry Hill Mortgage (CHMI), and Lument Finance (LFT) this afternoon.

Access Our Complete Research Library

We recently launched Hoya Capital Income Builder - the new premier investment research service focused on real income-producing assets classes. Whether your focus is High Yield or Dividend Growth, we’ve got you covered with high-quality, actionable investment research and a comprehensive suite of tools and models to help build sustainable portfolio income targeting premium dividend yields of up to 10%. And of course, subscribers receive complete access to our investment research - including reports that are never published elsewhere - from Hoya Capital and our team of contributors.

Disclosure: Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index. Index definitions and a complete list of holdings are available on our website.

Additional Disclosure: It is not possible to invest directly in an index. Index performance cited in this commentary does not reflect the performance of any fund or other account managed or serviced by Hoya Capital Real Estate. Data quoted represents past performance, which is no guarantee of future results. Information presented is believed to be factual and up-to-date, but we do not guarantee its accuracy.