Stocks Slump • Casino M&A • Sentiment At Decade-Lows

- U.S. equity markets slumped Tuesday after China announced a loosening of COVID restrictions, adding to upward pressure on commodities and gasoline prices, which has fueled a plunge in consumer confidence.

- Following declines of 0.3% on Monday, the S&P 500 finished lower by 2.0% today, extending its drawdown back below the "bear market" threshold of 20%.

- Real estate equities were lower as well today as strong performance from residential REITs was offset again by declines from technology REITs. The Equity REIT Index declined by 1.2% today.

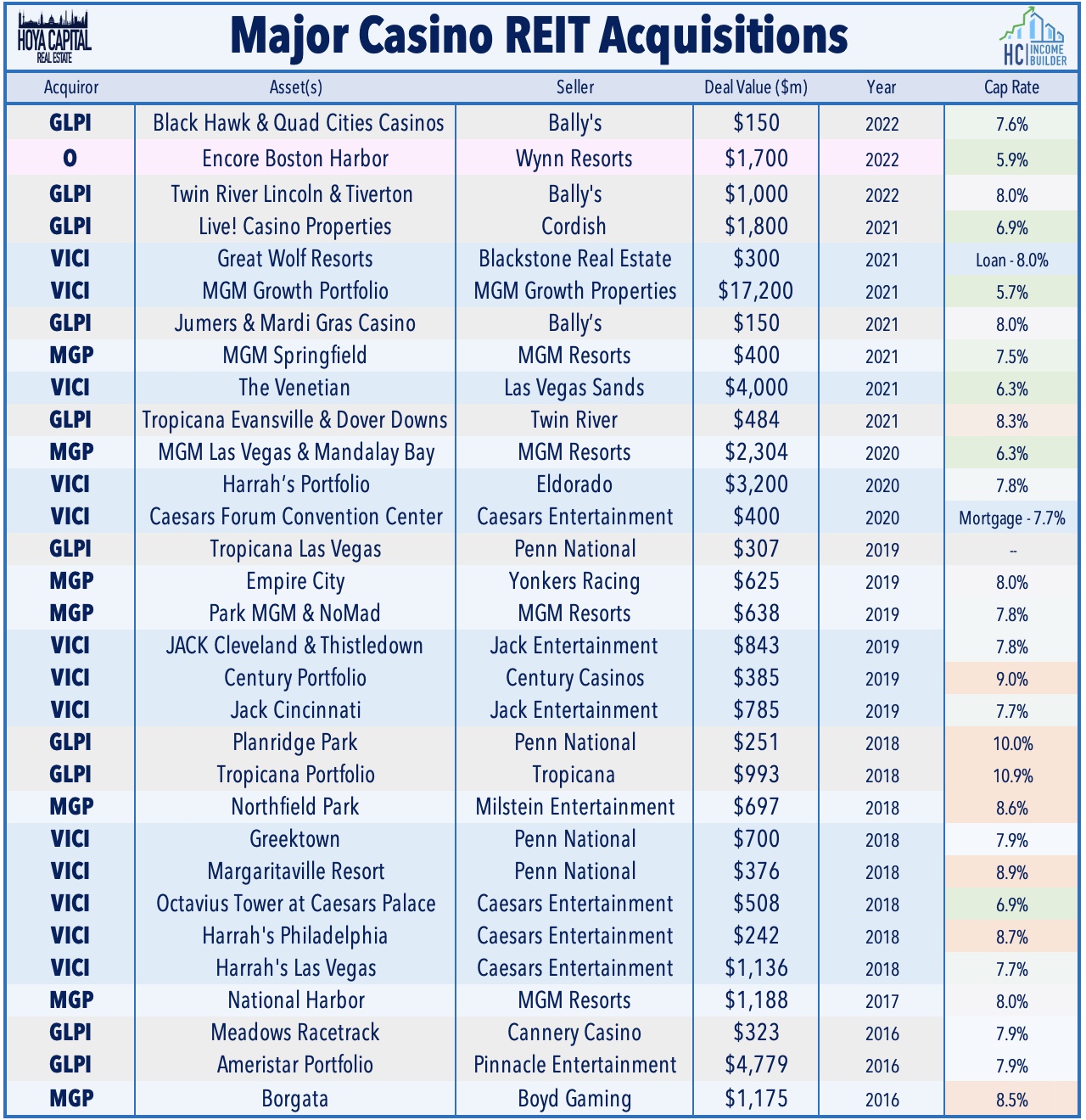

- After the close today, Gaming and Leisure Properties (GLPI) announced that it reached a $1.0 billion deal with Bally’s to acquire two Rhode Island casinos.

- Invesco Mortgage (IVR) surged 7% after providing a business update in which it held its dividend steady while reporting that declines in its Book Values were less steep than many feared.

Income Builder Daily Recap

We recently launched Hoya Capital Income Builder - a premier income-focused investment research service through Seeking Alpha Marketplace - that will be the new exclusive home of all of Hoya Capital's investment research. Income Builder focuses on real income-producing asset classes that offer the opportunity for diversification, monthly income, capital appreciation, and inflation hedging. If you're not already on board, give us a try with a completely risk-free two-week trial and take a look around.

U.S. equity markets slumped Tuesday after China announced a loosening of COVID restrictions, adding to upward pressure on commodities and gasoline prices, which fueled a plunge in consumer confidence to decade-lows. Following declines of 0.3% on Monday, the S&P 500 finished lower by 2.0% today, extending its drawdown back below the "bear market" threshold of 20%. Real estate equities were lower as well today as strong performance from residential REITs was offset again by declines from technology REITs. The Equity REIT Index declined by 1.2% today with 18 of the 19 property sectors in negative territory while Mortgage REIT Index slipped 0.5%.

Data released from the Conference Board this morning showed that consumer sentiment dipped to the lowest point in nearly a decade in June, consistent with data last week from the University of Michigan showing a historic decline in sentiment fueled by concerns over inflation. Pushing the potential relief a bit further away, commodities prices rallied today after China’s National Health Commission announced that it would loosen quarantine requirements for international travelers, indicating a potential departure from its COVID-zero policies. Ten of the eleven GICS equity sectors slumped today while the benchmark 10 Year Treasury Yield climbed modestly to 3.21% ahead of pivotal PCE inflation data on Thursday.

Real Estate Daily Recap

Casino: After the close today, Gaming and Leisure Properties (GLPI) announced that it reached a $1.0 billion deal with Bally’s Corporation (BALY) to acquire the real property assets of Bally’s two Rhode Island casino properties – Bally’s Twin River Lincoln Casino Resort (“Lincoln”) and Bally’s Tiverton Casino & Hotel. Bally’s will immediately lease back both properties and continue to own, control, and manage all the gaming operations of the facilities on an uninterrupted basis. GLPI expects the transaction to be accretive to earnings upon closing in late 2022 and intends to fund the transaction through a mix of debt, equity, and OP units. Both properties are expected to be added to the existing Bally’s Master Lease (the “Master Lease”) between GLPI and Bally’s, with incremental rent of $76.3 million. Bally's Master Lease has an initial term of 15 years (with 14 years remaining) followed by four five-year renewals at the tenant’s option.

Manufactured Housing: Today, we published Manufactured Housing: Recession Resistant REITs to the Income Builder marketplace which discussed our updated outlook and a recently-added position. Manufactured Housing REITs - one of the most "recession-resistant" property sectors given their countercyclical demand profile- have rebounded over the past month following uncharacteristic underperformance in early 2022. MH REITs have remarkably delivered nine consecutive years of outperformance compared to the broader REIT Index, benefiting from strong operational execution, significant supply constraints, demographic tailwinds, and high barriers to entry. While MH REITs have historically been among the most rate-sensitive sectors due to their remarkable consistency in delivering steady 3-4% rent growth, we believe their inflation-hedging potential is underappreciated.

Mortgage REIT Daily Recap

Per the REIT Rankings Tracker available to Income Builder subscribers, mortgage REITs were mixed today with residential mREITs gaining 0.1% while commercial mREITs slipped 0.9% Invesco Mortgage (IVR) surged nearly 7% today after it provided a business update after the close yesterday. Encouragingly, IVR - which is among the most highly-levered mREITs and among the most exposed to interest rate volatility - held its quarterly dividend steady at $0.90 per share while providing an updated Book Value Per Share ("BVPS") that is above the current anlayst consensus. IVR estimated that its BVPS was in a range of $15.94 to $16.60 - down roughly 22% at the midpoint of its range from the end of Q1, but the decline is roughly half of much as its share price during this period.

REIT Preferreds & Capital Raising

Per the Income Builder Preferred Tracker available to Income Builder subscribers, REIT Preferred stocks finished lower by 0.06% today, on average. REIT Preferreds are lower by roughly 13% on a total return basis this year after ending 2021 with price returns of roughly 8.0% and total returns of roughly 14%. There are now roughly 180 REIT-issued exchange-listed preferred and debt securities with an average current yield of 7.06%.

Economic Data This Week

We'll see another busy slate of economic data in the week ahead with several key inflation and housing market reports. Following the better-than-expected Pending Home Sales data on Monay, we saw home price data on Tuesday with reports from Case Shiller and the FHFA but due to the nearly two-month lag in these indexes, the effect of the recent rate-driven cooldown is slow to be reflected in the data. The most closely-watched report of the week will be PCE Price Index on Thursday which investors - and the Fed - are hoping will finally show some signs of moderating price pressures. We'll also be watching Construction Spending on Friday and a flurry of Purchasing Managers' Index ("PMI") data and consumer sentiment surveys throughout the week.

Access Our Complete Research Library

We recently launched Hoya Capital Income Builder - the new premier investment research service focused on real income-producing asset classes. Whether your focus is High Yield or Dividend Growth, we’ve got you covered with high-quality, actionable investment research and a comprehensive suite of tools and models to help build sustainable portfolio income targeting premium dividend yields of up to 10%. And of course, subscribers receive complete access to our investment research - including reports that are never published elsewhere - from Hoya Capital and our team of contributors.

Disclosure: Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index. Index definitions and a complete list of holdings are available on our website.

Additional Disclosure: It is not possible to invest directly in an index. Index performance cited in this commentary does not reflect the performance of any fund or other account managed or serviced by Hoya Capital Real Estate. Data quoted represents past performance, which is no guarantee of future results. Information presented is believed to be factual and up-to-date, but we do not guarantee its accuracy.