EU Energy Crisis • REIT Earnings • Week Ahead

- U.S. equity markets were mixed Monday ahead of a jam-packed week of economic data, corporate earnings results, and the Fed rate hike decision with recession and inflation concerns in the spotlight.

- Following gains of more than 2% last week - just its fourth "up-week" in sixteen weeks - the S&P 500 finished fractionally higher today. Mid-Caps and Small-Caps gained 0.6%.

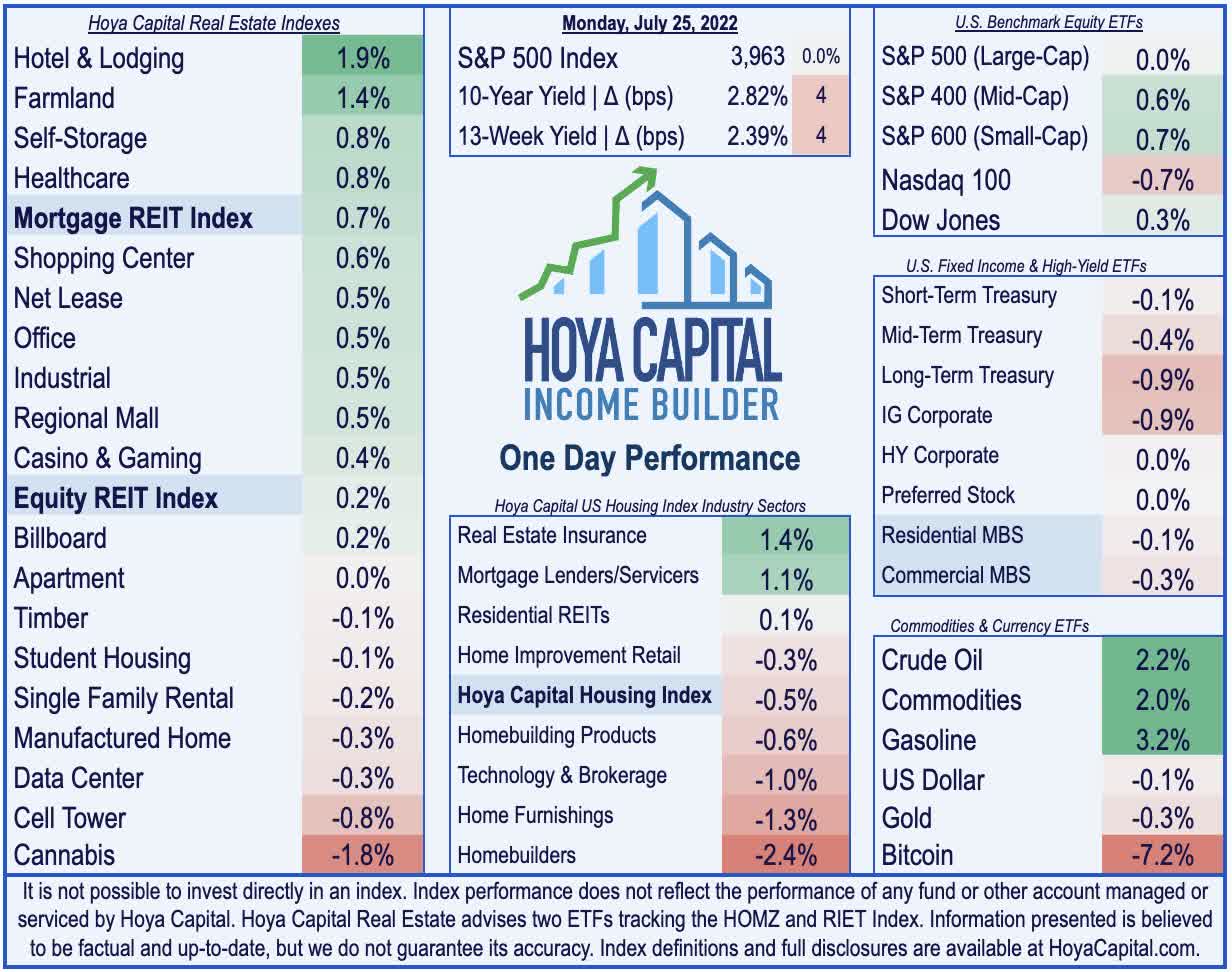

- Real estate equities were mostly-higher today ahead of a busy slate of REIT earnings results over the coming week. The Equity REIT Index gained 0.2% today with 11-of-18 property sectors higher.

- Economic issues in the Euro Area were amplified today after Russia said it would further reduce natural-gas supplies to Europe this week - a region still heavily dependent on Russian exports for 40-60% of their heating and electric power.

- REIT earnings season kicks into gear this week with reports from nearly a quarter of the sector over the coming five days. This afternoon, we'll hear results from lab space REIT Alexandria Realty (ARE) and manufactured housing REIT Sun Communities (SUI).

Income Builder Daily Recap

U.S. equity markets were mixed Monday ahead of a jam-packed week of economic data, corporate earnings results, and the Fed rate hike decision with recession and inflation concerns in the spotlight. Following gains of more than 2% last week - just its fourth "up-week" in sixteen weeks - the S&P 500 finished fractionally higher today. Domestic-focused indexes delivered stronger gains with the Mid-Cap 400 and Small-Cap 600 advancing 0.6% while the tech-heavy Nasdaq 100 slumped 0.7%. Real estate equities were mostly-higher today ahead of a busy slate of REIT earnings results over the coming week. The Equity REIT Index gained 0.2% today with 11-of-18 property sectors in positive territory while the Mortgage REIT Index gained 0.7%.

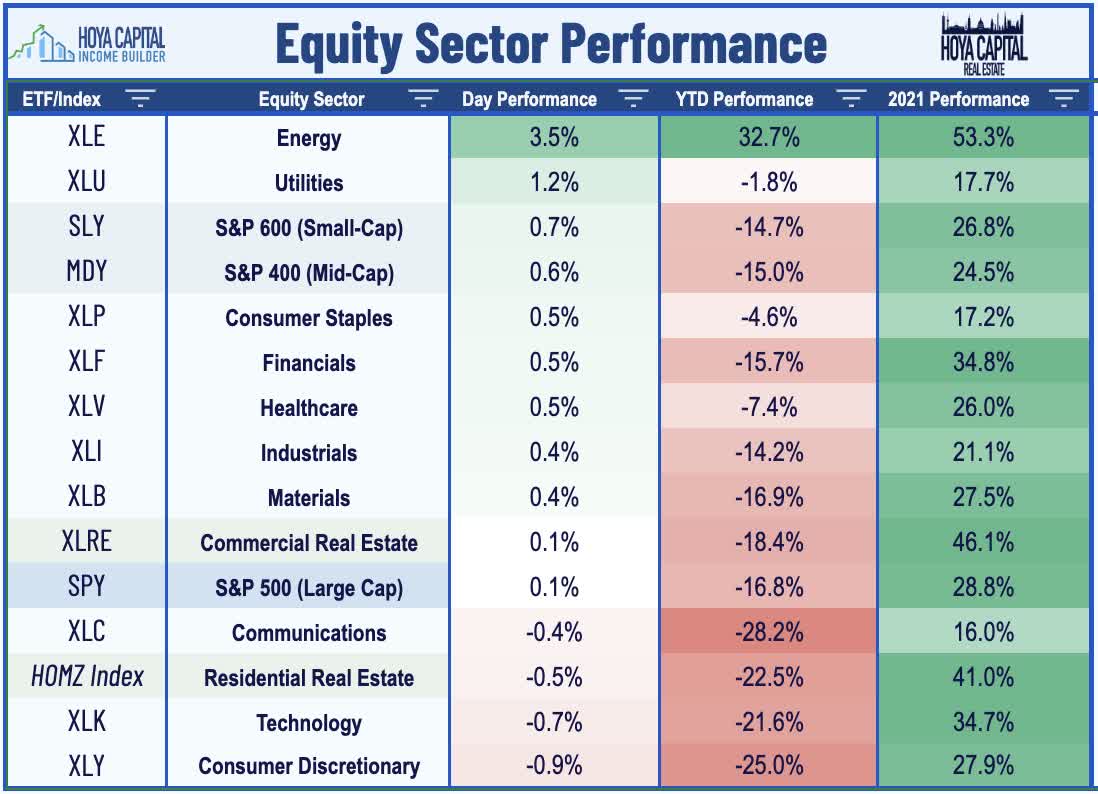

As discussed in our Real Estate Weekly Outlook, all eyes are on the Federal Reserve this week as weakening conditions have rapidly shifted the narrative from the Fed being "behind the curve" to potentially "ahead of the curve." Economic issues in the Euro Area were amplified today after Russia said it would further reduce natural-gas supplies to Europe this week - a region still heavily dependent on Russian exports for 40-60% of their heating and electric power - sending Crude Oil and Commodities (DJP) prices higher by 2%. Stateside, the 10-Year Treasury Yield was little-changed at 2.82% - a modest rebound after sliding to the lowest level since May last week - but still only 32 basis points above the upper-end of the expected Fed Funds overnight rate (2.25%-2.50%) beginning this week. Eight of the eleven GICS equity sectors finished higher today as gains from Energy (XLE) and Utilities (XLU) stocks offset declines from Technology (XLK) stocks.

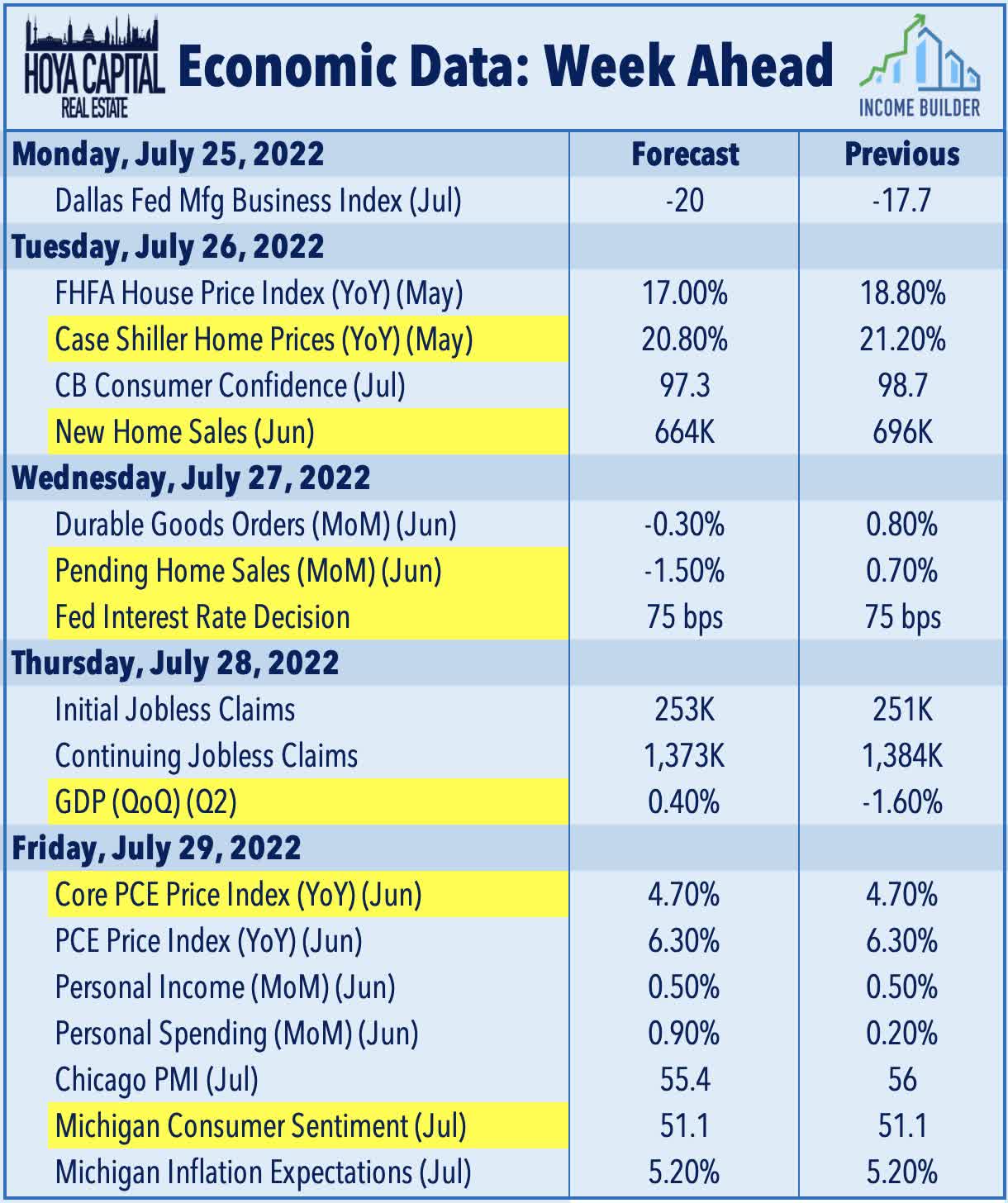

The week ahead will be jam-packed with earnings reports, economic data, and a critical Federal Reserve interest rate decision. On Tuesday and Wednesday, we'll see New Home Sales and Pending Home Sales data for June which is expected to reflect the significant summer slowdown seen in Existing Sales and Housing Starts data this past week. We'll also see home price data on Tuesday with reports from Case Shiller and the FHFA but due to the nearly two-month lag in these indexes, the effect of the recent cooldown in home sales activity may not yet be seen. On Wednesday afternoon, we'll see the FOMC Interest Rate Decision in which the Fed is expected to hike rates by 75 basis points, but could signal a "wait and see" approach to future hikes given the recent deterioration in global economic growth conditions. Whether or not we're truly in a recession will be determined on Thursday with Gross Domestic Product data. While the Atlanta Fed's GDPNow Forecast sees -1.6% growth in Q2, analysts still expect the economy to record a 0.4% increase in growth and narrowly avoid a technical recession. On Friday, we'll see another critical inflation report with the Core PCE Index - the Fed's preferred gauge of inflation - which has been one of the early indicators showing signs of peaking price pressures in recent months.

Real Estate Daily Recap

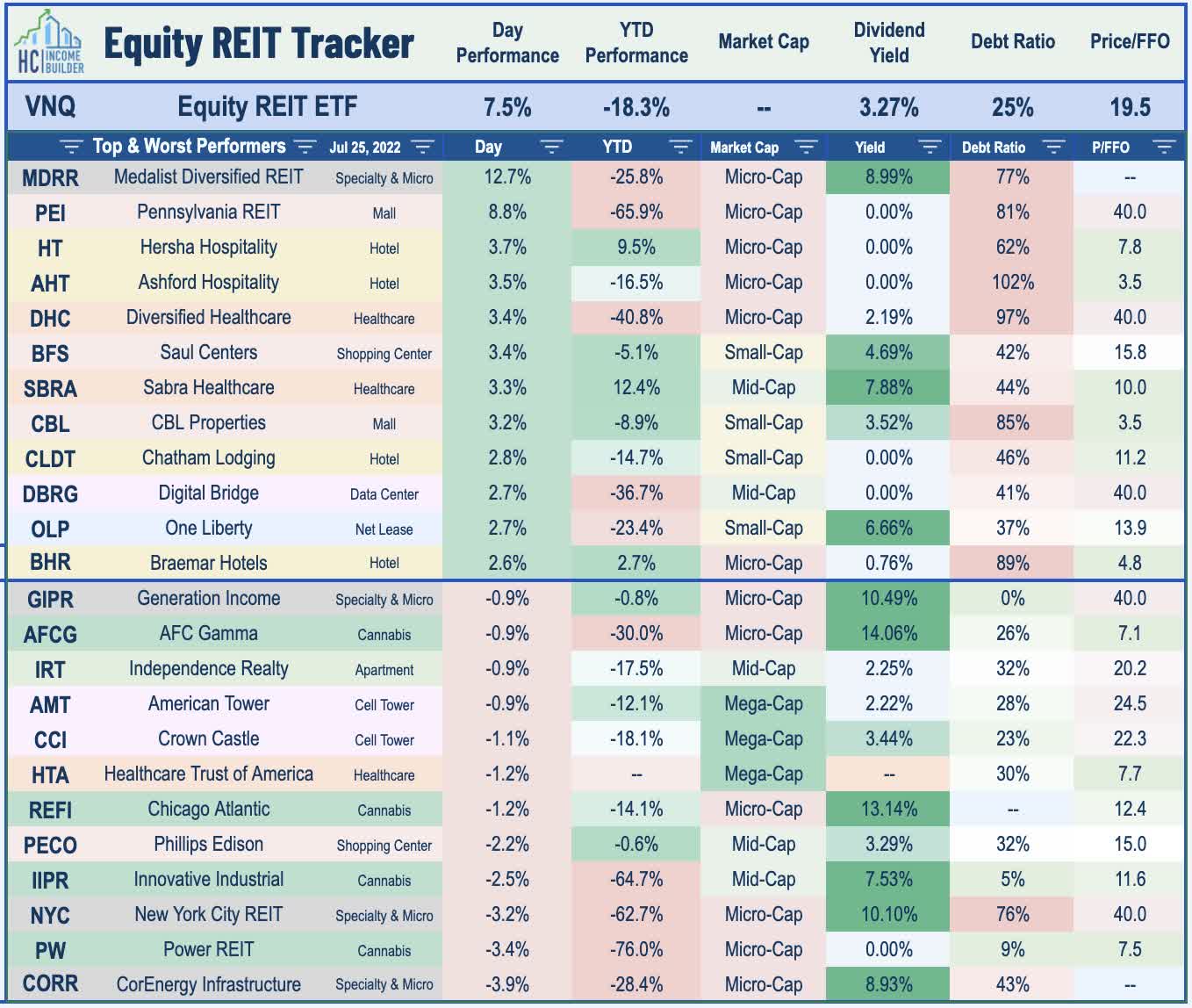

Best & Worst Performance Today Across the REIT Sector

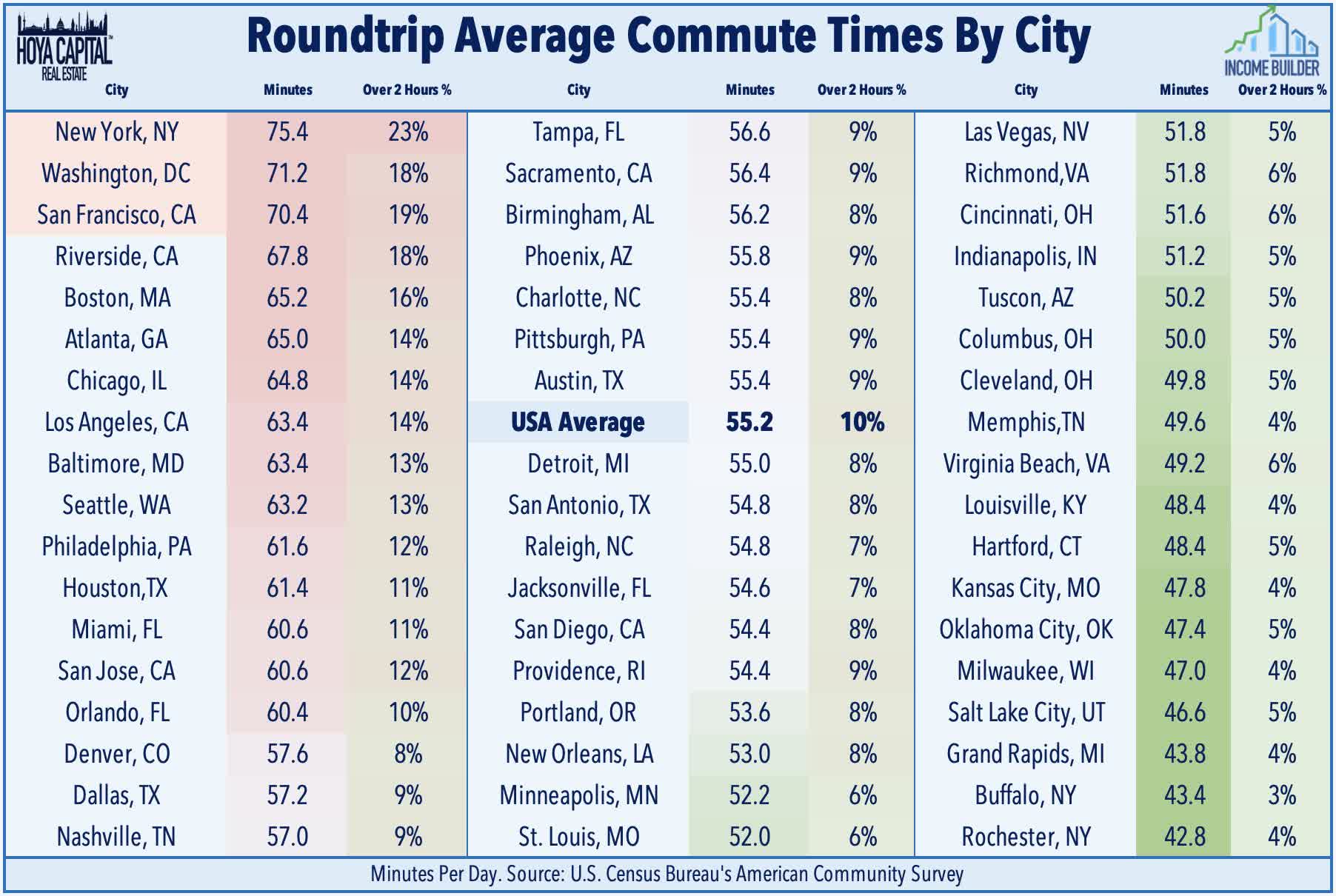

Office: Today we published Office REITs: Workers Hate The Commute, Not The Office which discussed our updated outlook and recent allocations in the office REIT sector. The 'Return to the Office' is here - but it's underwhelming. Despite 80% of employees currently in post-pandemic work arrangements, office utilization rates have remained 40-60% below pre-pandemic levels. Office leasing activity has remained surprisingly resilient at just 10% below pre-pandemic levels - as have office REIT earnings results - but corporations won't pay for half-empty space indefinitely. As projected, commute times have been the key variable explaining significant differences in WFH adoption across regions. Workers don't necessarily dislike the office, but long commutes more than offset any productivity gains. The outlook remains far sunnier in the Sunbelt and in secondary markets with net population growth, shorter commute times, and a more favorable industry mix.

REIT earnings season kicks into gear this week with reports from nearly a quarter of the sector over the coming five days. Last week, we published our REIT Earnings Preview which discusses the major themes and metrics we'll be watching across each of the major property sectors this earnings season. This afternoon, we'll hear results from lab space REIT Alexandria Realty (ARE) and manufactured housing REIT Sun Communities (SUI) - each of which we hold in our Income Builder REIT Dividend Growth Portfolio. We'll also see results from office REIT Brandywine Realty (BDN) this afternoon and from NexPoint Residential (NXRT) tomorrow morning. The past quarter has seen a reversal in property sector performance trends since early in 2022 with interest-rate-sensitive REITs catching a bid while pro-cyclical REITs have lagged on mounting recession concerns.

Mortgage REIT Daily Recap

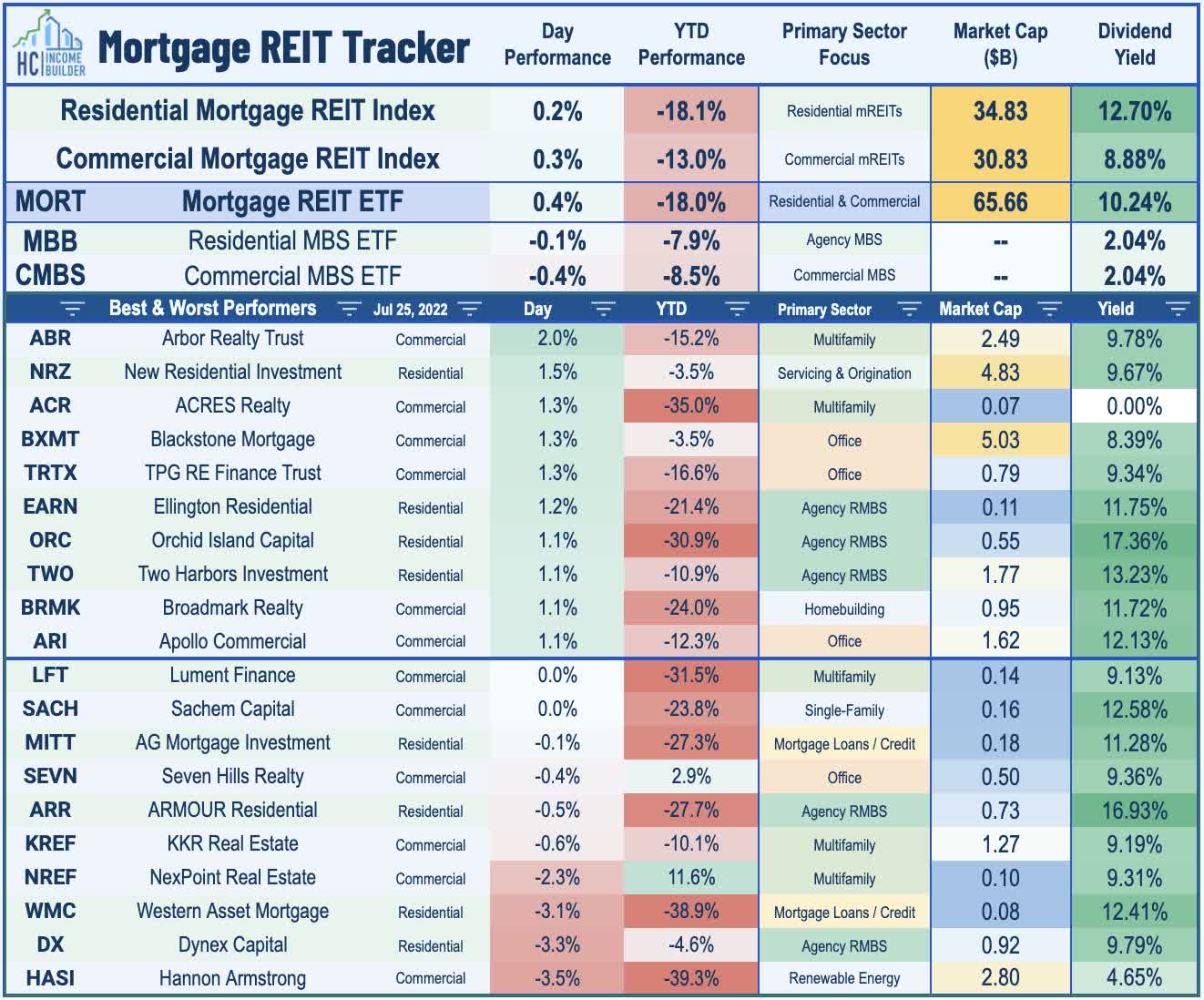

Per the REIT Rankings Tracker available to Income Builder subscribers, mortgage REITs finished modestly higher today as earnings season begins as residential mREITs advanced 0.2% while commercial mREITs gained 0.3%. Dynex Capital (DX) slumped after kicking-off mREIT earnings season this morning with mixed results. DX - which focuses primarily on agency RMBS - reported that its book value per share ("BVPS") declined by 7.9% in Q2 largely driven by spread widening on Agency RMBS, which followed a rather impressive first quarter in which it reported one of the few positive BVPS increases within the residential mREIT space resulting from gains on its interest rate hedge positions. Tomorrow we'll see results from AGNC Investment (AGNC) and KKR Real Estate (KREF).

REIT Preferreds & Capital Raising

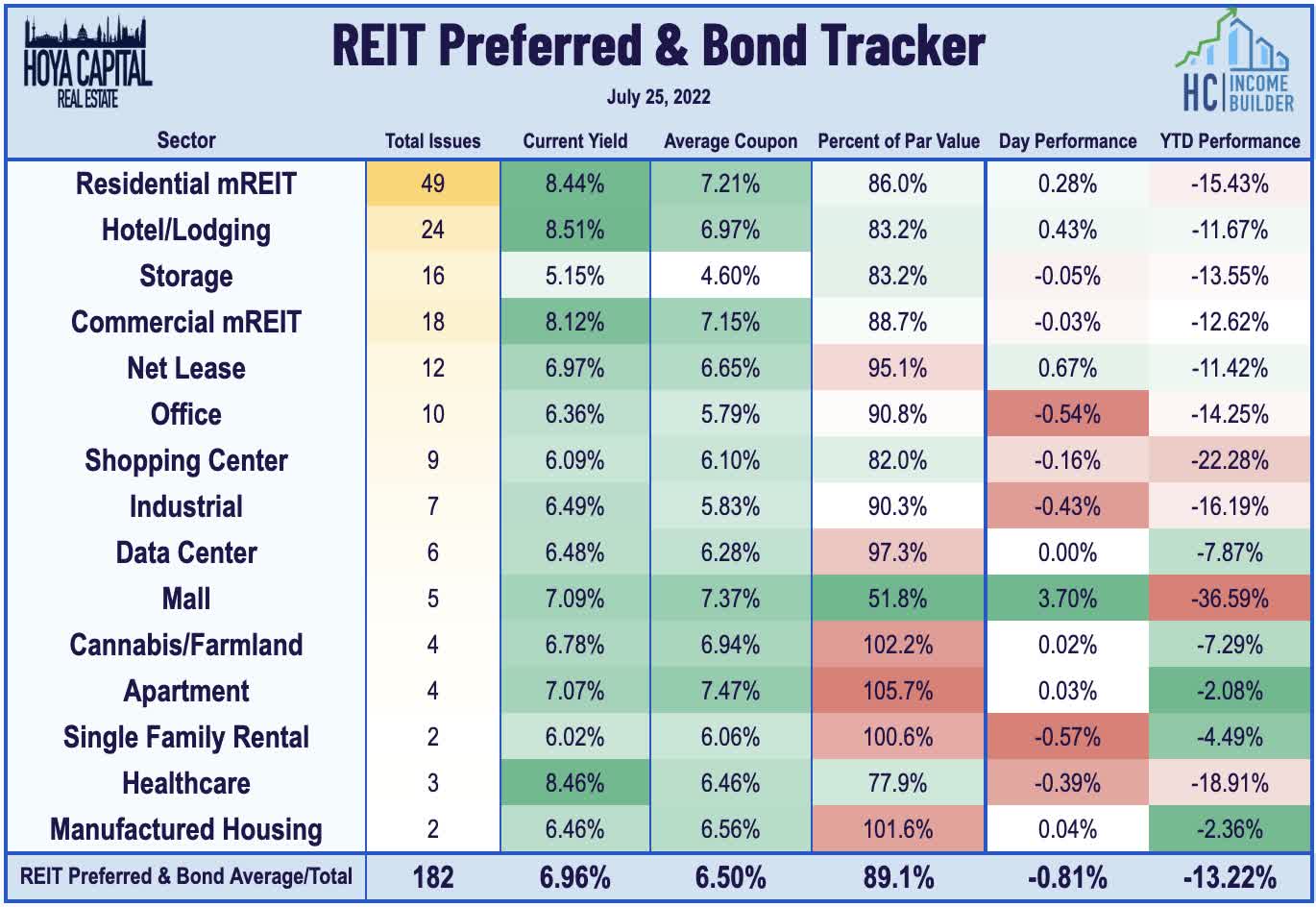

Per the Income Builder Preferred Tracker available to Income Builder subscribers, REIT Preferred stocks finished lower by 0.81% today, on average. REIT Preferreds are lower by roughly 10% on a total return basis this year after ending 2021 with price returns of roughly 8.0% and total returns of roughly 14%. There are now roughly 180 REIT-issued exchange-listed preferred and debt securities with an average current yield of 6.97%.

Disclosure: Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index. Index definitions and a complete list of holdings are available on our website.

Hoya Capital Research & Index Innovations (“Hoya Capital”) is an affiliate of Hoya Capital Real Estate, a registered investment advisory firm based in Rowayton, Connecticut that provides investment advisory services to ETFs, individuals, and institutions. Hoya Capital Research & Index Innovations provides non-advisory services including market commentary, research, and index administration focused on publicly traded securities in the real estate industry.

This published commentary is for informational and educational purposes only. Nothing on this site nor any commentary published by Hoya Capital is intended to be investment, tax, or legal advice or an offer to buy or sell securities. This commentary is impersonal and should not be considered a recommendation that any particular security, portfolio of securities, or investment strategy is suitable for any specific individual, nor should it be viewed as a solicitation or offer for any advisory service offered by Hoya Capital Real Estate. Please consult with your investment, tax, or legal adviser regarding your individual circumstances before investing.

The views and opinions in all published commentary are as of the date of publication and are subject to change without notice. Information presented is believed to be factual and up-to-date, but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. Any market data quoted represents past performance, which is no guarantee of future results. There is no guarantee that any historical trend illustrated herein will be repeated in the future, and there is no way to predict precisely when such a trend will begin. There is no guarantee that any outlook made in this commentary will be realized.

Readers should understand that investing involves risk and loss of principal is possible. Investments in real estate companies and/or housing industry companies involve unique risks, as do investments in ETFs. The information presented does not reflect the performance of any fund or other account managed or serviced by Hoya Capital Real Estate. An investor cannot invest directly in an index and index performance does not reflect the deduction of any fees, expenses or taxes.

Hoya Capital Real Estate and Hoya Capital Research & Index Innovations have no business relationship with any company discussed or mentioned and never receives compensation from any company discussed or mentioned. Hoya Capital Real Estate, its affiliates, and/or its clients and/or its employees may hold positions in securities or funds discussed on this website and our published commentary. A complete list of holdings and additional important disclosures is available at www.HoyaCapital.com.