Powell In Focus • REIT Updates • Skilled Nursing Struggles

- U.S. equity markets rebounded Tuesday despite a bounce in benchmark interest rates following comments from Fed Chair Powell as investors take positions ahead of the critical CPI report on Thursday.

- Following declines of 0.1% on Monday, the S&P 500 advanced 0.7% today while the Mid-Cap 400 and Small-Cap 600 each gained over 1%.

- Real estate equities were mostly higher as well today despite the jump in benchmark interest rates. The Equity REIT Index advanced 0.3% with 11-of-18 property sectors in positive territory.

- Omega Healthcare (OHI) slid more than 4% today after it announced in an investor presentation that it “expects both EBITDA and FAD to decline from 4Q22 to 1Q23” due to ongoing rent collection issues from several skilled nursing operator tenants.

- Net Lease REIT Getty Realty (GTY) gained 0.5% after providing a business update that included its initial 2023 outlook which calls for a full-year FFO of $2.20/share, representing growth of about 4% in 2023 following FFO growth of nearly 8% in 2022.

Income Builder Daily Recap

U.S. equity markets rebounded Tuesday despite a bounce in benchmark interest rates following comments from Fed Chair Powell as investors take positions ahead of the critical CPI report on Thursday. Following declines of 0.1% on Monday, the S&P 500 advanced 0.7% today while the Mid-Cap 400 and Small-Cap 600 each gained over 1%. The tech-heavy Nasdaq 100 gained nearly 1%. Real estate equities were mostly higher as well today despite the jump in benchmark interest rates. The Equity REIT Index advanced 0.3% with 11-of-18 property sectors in positive territory. The Mortgage REIT Index advanced 1.5% while Homebuilders gained 0.8%.

Investors parsed comments from Fed Chair Powell, who reiterated that the central bank is committed to fighting inflation but focused his remarks on the political independence of the Fed, commenting that the central bank should refrain from being a "climate policy maker" and instead should “‘stick to our knitting" on inflation and employment. The 10-Year Treasury Yield bounced 10 basis points today to close at 3.62% after dipping to the lowest level since mid-December on Monday. Crude Oil prices were little changed as investors monitor high-frequency data from China to assess the economic impacts of recent easing in COVID-related lockdown measures. Ten of the eleven GICS equity sectors were higher on the day with Communications (XLC) leading on the upside while Consumer Staples (XLP) stocks lagged.

Real Estate Daily Recap

Best & Worst Performance Today Across the REIT Sector

Healthcare: Omega Healthcare (OHI) slid more than 4% today after it announced in an investor presentation that it “expects both EBITDA and FAD to decline from 4Q22 to 1Q23” due to ongoing rent collection issues from several skilled nursing operator tenants. OHI reported that it collected 91% of its rent in October - up slightly from the third quarter in which it reported that operators representing 12% its tenant base did not pay all of their contractual rent. OHI noted that “both our dividend payout ratio and our near-term leverage being higher than our historical range during this period of time.” Last week, the National Investment Center reported that skilled nursing occupancy rates recovered to 79.4% in Q4 - up 70 basis points from the prior quarter - but still 8.2 percentage points below the pre-pandemic level of 87.6%.

Manufactured Housing: Today we published Manufactured Housing: Recession Resistant REITs. MH REITs snapped an incredible streak of nine straight years of outperformance over the REIT Index in 2022, impacted by headwinds from higher interest rates and hurricane-related disruptions. While rent growth has moderated from record-high levels across other residential property types, MH revenue growth is poised to accelerate in 2023, driven by their under-appreciated inflation-linkage and Cost-of-Living-Adjustment effects. Nearly half of MH residents receive monthly Social Security benefits, which are poised to rise 8.7% beginning this month - the highest COLA increase in four decades - which will give MH REITs and senior housing REITs room to push rent growth. Sun Communities (SUI) traded flat today after pricing $400 million of 5.70% senior notes due 2033.

Net Lease: Gas station owner Getty Realty (GTY) gained 0.5% after providing a business update that included its initial 2023 outlook which calls for a full-year FFO of $2.20/share, representing growth of about 4% in 2023 following FFO growth of nearly 8% in 2022. Elsewhere, Realty Income (O) slipped 1% after it priced $500 million of 5.05% senior unsecured notes due 2026 and $600 million of 4.85% senior unsecured notes due 2030. After the close today, Gladstone Commercial (GOOD) announced that it will reduce its monthly dividend from $0.1254 to $0.10 per share "in an effort to increase retained capital in anticipation of further economic headwinds."

Industrial: A pair of industrial REITs provided business updates ahead of the start of fourth-quarter earnings season later this month. Terreno (TRNO) traded little-changed today after it provided preliminary fourth-quarter results, noting that its operating portfolio was 98.6% leased at the end of Q4 - up 20 basis points from last quarter. Average rent spreads on new and renewed leases surged 45.2% in Q4, resulting in a full-year average rental rate increase of 49.5%. Indus Realty (INDT) was also little changed today after providing a business update noting that its portfolio was 98.8% leased while commenting that it is "actively evaluating the best path forward for the Company to maximize shareholder value" after it received an unsolicited takeover proposal from GIC Real Estate and Centerbridge to acquire 100% of the outstanding shares of the company’s common stock at $65.00 per share in cash.

Shopping Center: SITE Centers (SITC) provided a business update in which it reported that it sold 4 shopping centers and 1 land parcel in the fourth quarter for $166.3 million and used the proceeds to repurchase $28.8 million of common stock. Both SITE and Kimco (KIM) were under pressure today, however, after an analyst downgrade from Mizuho to Neutral from Buy. Troubled retailer Bed Bath & Beyond (BBBY) - which represents about 1% of shopping center REIT revenues - jumped nearly 30% today after it announced cost-cutting plans as it seeks to avoid bankruptcy. Later this week, we'll publish an updated report on the Shopping Center sector analyzing recent holiday spending data and our outlook for 2023.

Additional Headlines from The Daily REITBeat on Income Builder

- Crown Castle (CCI) priced $1 billion of 5.00% senior notes due 2028.

- Safehold (SAFE) announced a new $500 million unsecured revolving credit facility priced at SOFR plus 100 basis points with a maturity of July 2025.

- New York City REIT (NYC) announced that it will change its name to American Strategic Investment Co. effective on January 19, 2023.

- Fitch Ratings affirmed Global Net Lease (GNL) “BB+” credit rating but revised its outlook to negative from stable.

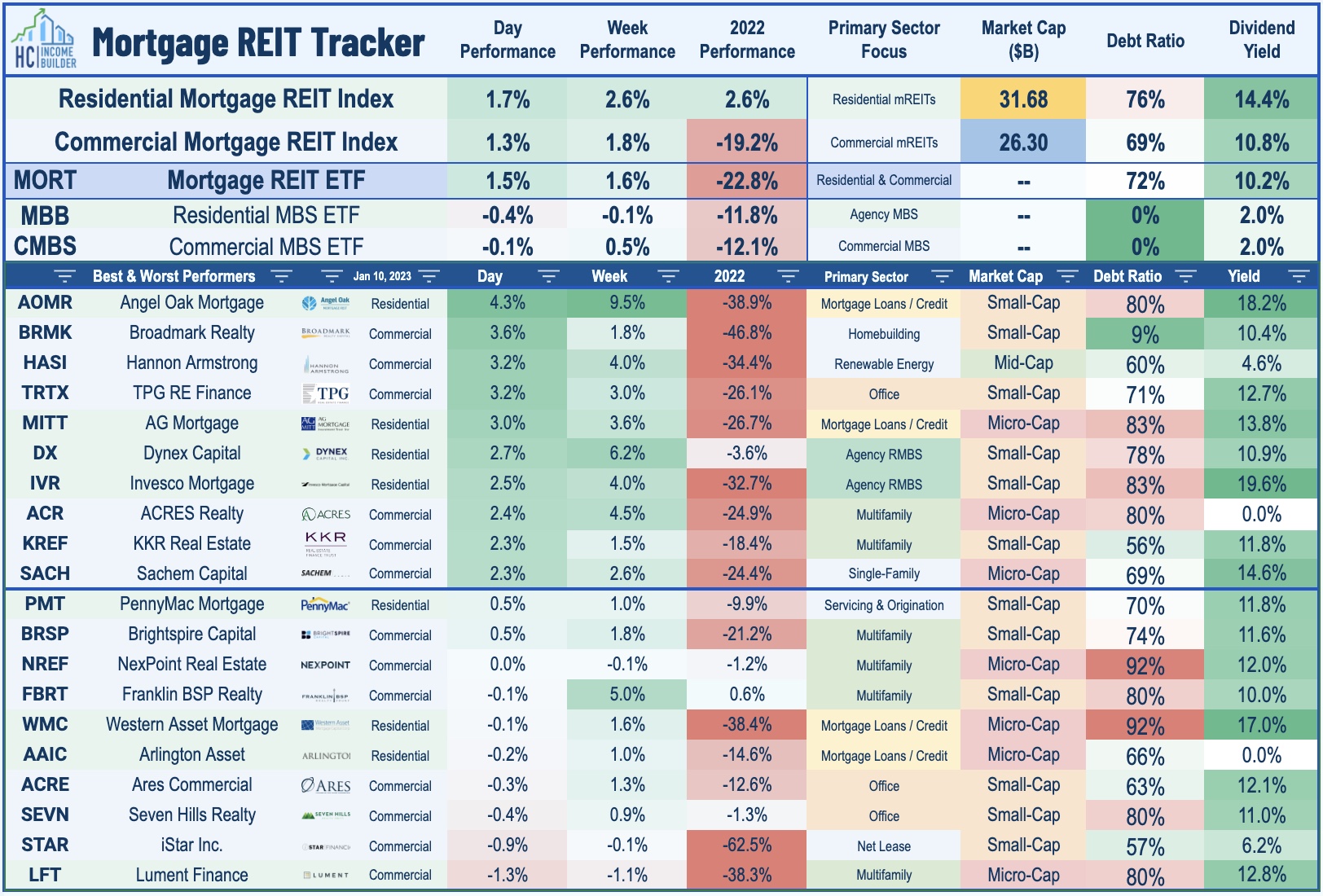

Mortgage REIT Daily Recap

Per the REIT Rankings Tracker available to Income Builder subscribers, mortgage REITs continued their strong start to the year with residential mREITs gaining another 1.7% today while commercial mREITs gained 1.3%. Ellington Residential (EARN) advanced 2%a after holding its monthly dividend steady at $0.08/share, representing a forward dividend yield of 12.9%. Ellington Financial (EFC) also gained 2% after holding its monthly dividend steady at 0.15/share, representing a dividend yield of 13.9%. Last month, we published Mortgage REITs: High Yields Are Fine, For Now, which noted that despite paying average dividend yields in the mid-teens, the majority of mREITs have been able to cover their dividends, but we flagged a handful of mREITs with payout ratios above 100% of EPS.

Economic Data This Week

It'll be another busy week of economic data with the main event coming on Thursday with the Consumer Price Index for December, which investors and the Fed are hoping will show that the fastest pace of year-over-year increases in inflation is finally behind us. The headline CPI is expected to moderate to a 6.5% year-over-year rate while the Core CPI is expected to decelerate to 5.7%. As with recent months, the metric we're watching most closely is the CPI-ex-Shelter Index - which since July has averaged a -1.9% annualized rate - among the most deflationary five-month periods on record. Critically, gasoline prices averaged $3.21 nationally in December - down about 13% from the prior month and 3% from the prior year. We'll also get our first look at Michigan Consumer Sentiment data on Friday - which includes a closely-watched consumer inflation expectations survey - and we'll be closely watching Jobless Claims data on Thursday as well.

Disclosure: Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index. Index definitions and a complete list of holdings are available on our website.

Hoya Capital Research & Index Innovations (“Hoya Capital”) is an affiliate of Hoya Capital Real Estate, a registered investment advisory firm based in Rowayton, Connecticut that provides investment advisory services to ETFs, individuals, and institutions. Hoya Capital Research & Index Innovations provides non-advisory services including market commentary, research, and index administration focused on publicly traded securities in the real estate industry.

This published commentary is for informational and educational purposes only. Nothing on this site nor any commentary published by Hoya Capital is intended to be investment, tax, or legal advice or an offer to buy or sell securities. This commentary is impersonal and should not be considered a recommendation that any particular security, portfolio of securities, or investment strategy is suitable for any specific individual, nor should it be viewed as a solicitation or offer for any advisory service offered by Hoya Capital Real Estate. Please consult with your investment, tax, or legal adviser regarding your individual circumstances before investing.

The views and opinions in all published commentary are as of the date of publication and are subject to change without notice. Information presented is believed to be factual and up-to-date, but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. Any market data quoted represents past performance, which is no guarantee of future results. There is no guarantee that any historical trend illustrated herein will be repeated in the future, and there is no way to predict precisely when such a trend will begin. There is no guarantee that any outlook made in this commentary will be realized.

Readers should understand that investing involves risk and loss of principal is possible. Investments in real estate companies and/or housing industry companies involve unique risks, as do investments in ETFs. The information presented does not reflect the performance of any fund or other account managed or serviced by Hoya Capital Real Estate. An investor cannot invest directly in an index and index performance does not reflect the deduction of any fees, expenses or taxes.

Hoya Capital Real Estate and Hoya Capital Research & Index Innovations have no business relationship with any company discussed or mentioned and never receives compensation from any company discussed or mentioned. Hoya Capital Real Estate, its affiliates, and/or its clients and/or its employees may hold positions in securities or funds discussed on this website and our published commentary. A complete list of holdings and additional important disclosures is available at www.HoyaCapital.com.