Sticky Inflation • Stocks Slide • REIT Earnings

- U.S. equity markets finished broadly lower Thursday as investors parsed another round of hotter-than-expected economic data and hawkish rhetoric from several Federal Reserve officials.

- Erasing its gains for the week, the S&P 500 finished lower by 1.4% today while the tech-heavy Nasdaq 100 slid 1.9%.

- Real estate equities were among the better-performers today after a solid slate of earnings results and M&A news. Equity REITs declined 1.0% today while Mortgage REITs slipped 0.3%.

- The 10-Year Treasury Yield climbed to 3.84% - near the highest level of the year - after Producer Price Index data showed a reacceleration in price pressures in January.

- Hotel REIT Services Property (SVC) surged more than 20% after BP agreed to acquire TravelCenters of America - an operator of convenience stores that is partially owned by SVC and its external advisor RMR Group.

Income Builder Daily Recap

U.S. equity markets finished broadly lower Thursday as investors parsed another round of hotter-than-expected economic data and hawkish rhetoric from several Federal Reserve officials. Erasing its gains for the week, the S&P 500 finished lower by 1.4% today while the tech-heavy Nasdaq 100 slid 1.9%. The 10-Year Treasury Yield climbed to the highest levels of the year - rising 3 basis points to 3.84% today - after Producer Price Index data showed a reacceleration in price pressures in January. Real estate equities were among the better-performers today after a solid slate of earnings results and M&A news. The Equity REIT Index declined 1.0% today with 15-of-18 property sectors in negative territory while the Mortgage REIT Index slipped 0.3%.

Real Estate Daily Recap

Best & Worst Performance Today Across the REIT Sector

Hotels: Services Property (SVC) surged more than 20% after BP (BP) agreed to acquire TravelCenters of America (TA) at an 84% premium to its prior close - an operator of convenience stores that is partially owned by SVC and its external advisor RMR Group (RMR). Host Hotels (HST) dipped more than 5% today after reporting mixed results with a relatively strong final quarter of 2022 offset by a cautious outlook for 2023. HST noted that its FFO slightly exceeded its pre-pandemic level for full-year 2022 at $1.79/share, but projects that its FFO will decline by about 4% in 2023. HST sees flat RevPAR for full-year 2023 and expects its margins to decline in 2023 due to wage inflation, higher staffing levels, higher insurance and utility expenses, lower attrition and cancelation fees, and occupancy below 2019 levels. Hersha (HT) also finished lower by about 6% despite providing a more upbeat outlook, noting that its seen strong demand trends in early 2023 with January and February RevPAR ahead of 2019-levels by 3.9% and 5.5%, respectively.

Healthcare: Welltower (WELL) rallied more than 3% today after reporting better-than-expected results driven by a continued occupancy recovery and strong pricing trends in its senior housing portfolio. WELL noted that its FFO rose 17.1% in 2022 and projects growth of 2.7% in 2023 which would bring its FFO to within about 5% of pre-pandemic levels by the end of the year. Hospital owner Medical Properties Trust (MPW) declined about 2% today after it announced that Catholic Health Initiatives Colorado will lease its entire Utah hospital portfolio subsequent to CHIC’s acquisition of the business currently operated by Steward Health Care. Centura Health will manage the facilities and cash rental payments during the 15-year initial lease term are to begin at roughly 7.8% of MPT’s gross investment and increase by 3.0% annually.

Net Lease: A pair of net lease REITs traded higher today after reporting solid fourth-quarter results. Essentials Property (EPRT) rallied more than 2% after reporting full-year FFO growth of 14.2% for full-year 2022 - the highest in the net lease sector - and projecting FFO growth of 3.9% for 2023, also the highest among the REITs to report results thus far. Four Corners (FCPT) advanced about 1% after reporting in-line results with its full-year FFO rising 5.1% in 2022. We remain focused on cap rate commentary, which continues to show that net lease REITs are carrying on with "business as usual" despite the surge in benchmark interest rates over the last year. EPRT reported acquisition cap rates of 7.5% in Q4 - up 60 basis points from last year - while FCPT reported cap rates of 6.6% - up 40 basis points. During this period, the average 10-Year Treasury Yield climbed 230 basis points.

Data Center: Equinix (EQIX) - which we own in the REIT Dividend Growth Portfolio - traded flat despite reporting very strong results and announcing a 10% increase in its cash dividend to $3.41/share. EQIX recorded full-year FFO growth of 11% on a constant-currency basis and projects a growth of 9% in 2023. On a non-currency-adjusted basis, EQIX recorded growth of 9.0% in 2022 and projects growth of 5.6% in 2023. EQIX noted strength in its Americas region which "had another quarter of strong gross bookings, lower MRR churn and continued favorable pricing trends led by our New York, Toronto and Washington, D.C. metros." Pricing softened a bit in Q4 with EQIX recording same-store revenue total revenue growth of 5% - down from 7% last quarter. We'll hear results from Digital Realty (DLR) this afternoon.

Industrial: STAG Industrial (STAG) finished lower by 1.5% after reporting in-line results, noting that its FFO climbed 7.3% for full-year 2022 - 50 basis points above its prior guidance. STAG reported cash leasing spreads of 14.2% in Q4 and noted in its earnings call that its seen spreads accelerate to "25% to 30%" thus far in 2023. STAG's outlook for 2023 appears quite conservative given these strong pricing trends, calling for FFO growth of 1.4% for full-year 2023 as negative impacts from higher interest expense offset its expected same-store NOI growth of nearly 5%. LXP Industrial (LXP) finished lower after reporting mixed results, noting that its full-year 2022 FFO declined 14.1% - slightly better than its prior guidance - as it sold down its non-industrial assets throughout the year. LXP reported strong leasing spreads of 42.6% - an acceleration from the 40.7% growth reported last quarter. We'll hear results from Americold (COLD) this afternoon.

Single-Family Rental: Invitation Homes (INVH) traded lower by about 1% today after kicking off SFR REIT earnings season with a decent report, noting that its FFO rose 10.2% for full-year 2022 - 80 basis points above its prior outlook - and forecast FFO growth of 4.3% for full-year 2023. Rental rates remained quite firm in late 2022 despite the broader cooldown in national rent growth. INVH recorded blended rent growth of 9.1% in Q4 - comprised of renewal spreads of 9.9% and new lease spreads of 7.4%. INVH's revenue collection did see a modest decline in the back-half of 2022 - primarily related to the ongoing eviction moratorium in California - with rent collection declining to 97% in Q3 and Q4, down from its long-term average of 99%. Earlier this month, INVH hiked its dividend by 18% to $0.26/share.

Office: A pair of office REITs were among the leaders after reporting decent fourth-quarter results. Empire State Realty (ESRT) rallied after reporting full-year FFO growth of 28.6% for full-year 2022 which marked a full-recovery to its pre-pandemic FFO level from full-year 2019. ESRT reported decent leasing metrics with a 100 basis point increase in comparable occupancy. Office Properties Income (OPI) rallied after reporting that its FFO was roughly flat in 2022 and progress with asset sales to pay down its debt, selling $210M of properties in 2022 and shrinking its variable rate percentage to less than 10% of its total debt. Paramount (PGRE) declined after reporting mixed results, noting that its FFO rose 6.5% for full-year 2022 - above its prior guidance - but recorded soft leasing activity in Q4 with a 10 basis point decline in occupancy rate and slightly negative cash re-leasing spread. Among the dozen office REITs that provided 2023 guidance, FFO is expected to decline by an average of 7.2% following gains of 4.3% this year that briefly brought the office REIT sector aggregate FFO above its pre-pandemic level.

Billboard: Today we published Billboard REITs: We're Paying Attention on the Income Builder marketplace which discussed our updated sector outlook and recent allocations. From the bright lights of Times Square to the iconic signage on LA's Sunset Strip, advertising billboards have been an inescapable fixture of the typical American commute for decades. Billboard REITs own a commanding share of the nation's 500,000 outdoor advertising displays - a surprisingly resilient business that has seen revenues and profitability fully recover to pre-pandemic levels. Unlike other increasingly-cluttered digital formats, there's "only one channel" on the highway and these Billboard REITs are well-positioned to capture the steadily growing share of marketing spending towards Out-of-Home ("OOH") advertising. We like the clear supply constraints and the importance of scale in the billboard business – granting these REITs a meaningful competitive advantage and legitimate economic moat.

Additional Headlines from The Daily REITBeat on Income Builder

- VICI Properties (VICI) announced a triple-net lease agreement with CNB with respect to the real property associated with Gold Strike where initial total annual rent under the lease is $40.0 million and the lease has an initial term of 25-years with three 10-year tenant renewal options.

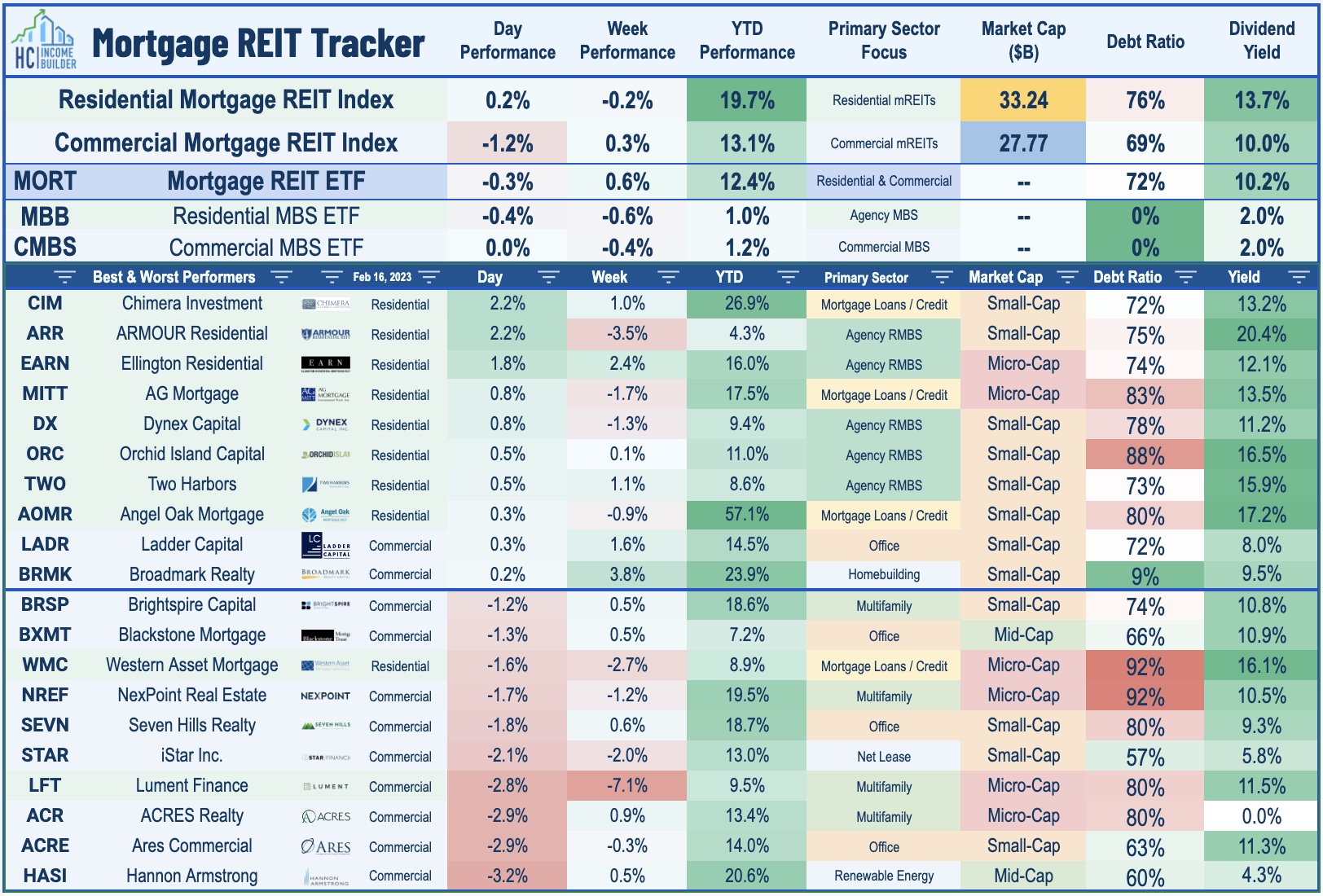

Mortgage REIT Daily Recap

Per the REIT Rankings Tracker available to Income Builder subscribers, mortgage REITs mixed today with residential mREITs gaining 0.2% while commercial mREITs slipped 1.2%. ARMOUR Residential (ARR) gained more than 2% today after reporting that its Book Value Per Share ("BVPS") was roughly flat in Q4 at $5.78/share while its Distributable Earnings per Share stood at $0.27 per common share, which matches its reduced dividend rate announced yesterday. Residential mREITs have reported an average 2% increase in BVPS in Q4 from the prior quarter - led by a rebound in agency-focused mREITs - while commercial mREITs have reported a 1% decline.

Economic Data This Week

We'll publish a full analysis and commentary of this week's developments in the real estate industry, as well as an analysis of the busy week of economic data in our Real Estate Weekly Outlook this weekend.

Disclosure: Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index. Index definitions and a complete list of holdings are available on our website.

Hoya Capital Research & Index Innovations (“Hoya Capital”) is an affiliate of Hoya Capital Real Estate, a registered investment advisory firm based in Rowayton, Connecticut that provides investment advisory services to ETFs, individuals, and institutions. Hoya Capital Research & Index Innovations provides non-advisory services including market commentary, research, and index administration focused on publicly traded securities in the real estate industry.

This published commentary is for informational and educational purposes only. Nothing on this site nor any commentary published by Hoya Capital is intended to be investment, tax, or legal advice or an offer to buy or sell securities. This commentary is impersonal and should not be considered a recommendation that any particular security, portfolio of securities, or investment strategy is suitable for any specific individual, nor should it be viewed as a solicitation or offer for any advisory service offered by Hoya Capital Real Estate. Please consult with your investment, tax, or legal adviser regarding your individual circumstances before investing.

The views and opinions in all published commentary are as of the date of publication and are subject to change without notice. Information presented is believed to be factual and up-to-date, but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. Any market data quoted represents past performance, which is no guarantee of future results. There is no guarantee that any historical trend illustrated herein will be repeated in the future, and there is no way to predict precisely when such a trend will begin. There is no guarantee that any outlook made in this commentary will be realized.

Readers should understand that investing involves risk and loss of principal is possible. Investments in real estate companies and/or housing industry companies involve unique risks, as do investments in ETFs. The information presented does not reflect the performance of any fund or other account managed or serviced by Hoya Capital Real Estate. An investor cannot invest directly in an index and index performance does not reflect the deduction of any fees, expenses or taxes.

Hoya Capital Real Estate and Hoya Capital Research & Index Innovations have no business relationship with any company discussed or mentioned and never receives compensation from any company discussed or mentioned. Hoya Capital Real Estate, its affiliates, and/or its clients and/or its employees may hold positions in securities or funds discussed on this website and our published commentary. A complete list of holdings and additional important disclosures is available at www.HoyaCapital.com.