Double-Digit PPI • Logistics Troubles • Cell Tower Deal

- U.S. equity markets declined for a fifth-straight session Thursday on data showing hotter-than-expected producer price inflation while earnings season began with a pair of downbeat reports from major banks.

- Now lower by nearly 3% on the week, the S&P 500 declined 0.3% today after a late-day rally that pared much of its intra-day declines which were as steep as 2%.

- Now lower by nearly 3% on the week, the S&P 500 declined 0.3% today despite a late-day rally that pared much of its intra-day declines which were as steep as 2%.

- Echoing the red-hot CPI report on Wednesday, PPI data this morning showed that wholesale prices rose 11.3% from a year ago in June - well above the 10.7% rate expected - and just below the record 11.6% posted in March.

- Industrial Logistics Properties (ILPT) dipped more than 20% today after slashing its dividend to $0.01, citing difficulties related to its recent acquisition of Monmouth. ILPT cited rising rates and difficult market conditions for delays to its post-acquisition financing plans.

Income Builder Daily Recap

U.S. equity markets declined for a fifth-straight session Thursday on data showing hotter-than-expected producer price inflation while earnings season began with a pair of downbeat reports from major banks. Now lower by nearly 3% on the week, the S&P 500 declined 0.3% today despite a late-day rally that pared much of its intra-day declines which were as steep as 2%. The tech-heavy Nasdaq 100 ended higher by 0.4% today. Real estate equities lagged today as long-term benchmark interest rates rebounded. The Equity REIT Index finished lower by 0.9% today with all 18 REIT sectors in negative territory while the Mortgage REIT Index dipped 2.0%.

Echoing the red-hot CPI report on Wednesday, PPI data this morning showed that wholesale prices rose 11.3% from a year ago in June - well above the 10.7% rate expected - and just below the record 11.6% posted in March. As with yesterday, bond markets were again relatively steady despite expectations of an even-more-aggressive path of Fed rate hikes as the 10-Year Treasury Yield rose modestly to 2.96% - still well below its recent high of 3.50% reached in early June. Nine of the eleven GICS equity sectors were lower today, dragged on the downside by Financials (XLF) stocks after JPMorgan (JPM) and Morgan Stanley (MS) each reported weaker-than-expected results while indicating a more downbeat economic outlook.

Real Estate Daily Recap

Best & Worst Performance Today Across the REIT Sector

Industrial: Industrial Logistics Properties (ILPT) dipped more than 20% today after slashing its dividend to $0.01, citing difficulties related to its recent acquisition of Monmouth. ILPT noted that its "taking longer than originally expected to complete ILPT’s long-term financing plan for the Monmouth acquisition, which includes the sale of additional equity interests in its consolidated joint venture, property sales and other refinancing activities" due to the "increases in interest rates and deterioration in real estate market conditions." Industrial REITs have been slammed this year in a sell-off sparked by Amazon's (AZMN) plans to scale back its logistics leasing activity. ILPT announced that it to "enhance its liquidity until it completes its long term financing plan for the Monmouth acquisition and/or its leverage profile otherwise improves." ILPT noted that it anticipates that its dividend will return to a rate at, or close to, its historical level sometime in 2023.

Cell Towers: Together with Brookfield Infrastructure (BIP), technology REIT DigitalBridge (DBRG) announced that funds affiliated with its investment management arm have reached an agreement to acquire a 51% ownership stake in Germany-based GD Towers. GD Towers - the mobile telecommunications tower business of Deutsche Telekom - is Germany’s largest tower company, owning and operating over 33,000 towers and communication sites in Germany and over 7,000 sites in Austria. The deal values GD Towers at $17.5B including the assumption of net debt and the deal is expected to close in late 2022. Deutsche Telekom plans to use the proceeds to lower debt levels and fund plans to gain majority control of T-Mobile US. Details of the ownership breakdown between Brookfield and Digital Bridge were not yet disclosed, and it's not yet clear whether any of the assets will be included in DBRG's Digital Operating business or if all will be retained under its Digital Investment Management business.

Storage: Yesterday, we published Storage REITs: Recession Resistant, But Not Acting Like It. Self-Storage REITs - usually known for their recession-resistant characteristics - have sold off in recent months despite a stellar slate of earnings results and upbeat interim updates. Storage REITs appear to be caught up in the bearish sentiment surrounding industrial REITs– a rather distant “cousin” to the storage sector– and the unusually-high recent correlations are fundamentally unwarranted. Few REIT sectors have defied expectations as comprehensively as storage REITs since the start of the pandemic, and while several pandemic-fueled tailwinds are waning, the long-term outlook remains quite compelling. We discussed our updated outlook and recent allocations in the report linked here.

Mortgage REIT Daily Recap

Per the REIT Rankings Tracker available to Income Builder subscribers, mortgage REITs slumped today with residential mREITs slipping 2.3% while commercial mREITs declined by 1.8%. Hannon Armstrong (HASI) continued to bounce back today following a nearly 20% dip on Tuesday following the publication of a short report from Muddy Waters. Ready Capital (RC) finished lower by 2.5% after announcing a new joint venture with Starz Real Estate, a European commercial real estate lending platform that plans to originate $300M of small-balance commercial real estate loans across several European markets over the next 2 years. Seven Hills Realty Trust (SEVN) held its quarterly dividend steady at $0.25/share, representing a forward yield of 9.2%. Orchid Island Capital (ORC) held its monthly dividend steady at $0.045/share, representing a forward yield of 18.5%.

REIT Preferreds & Capital Raising

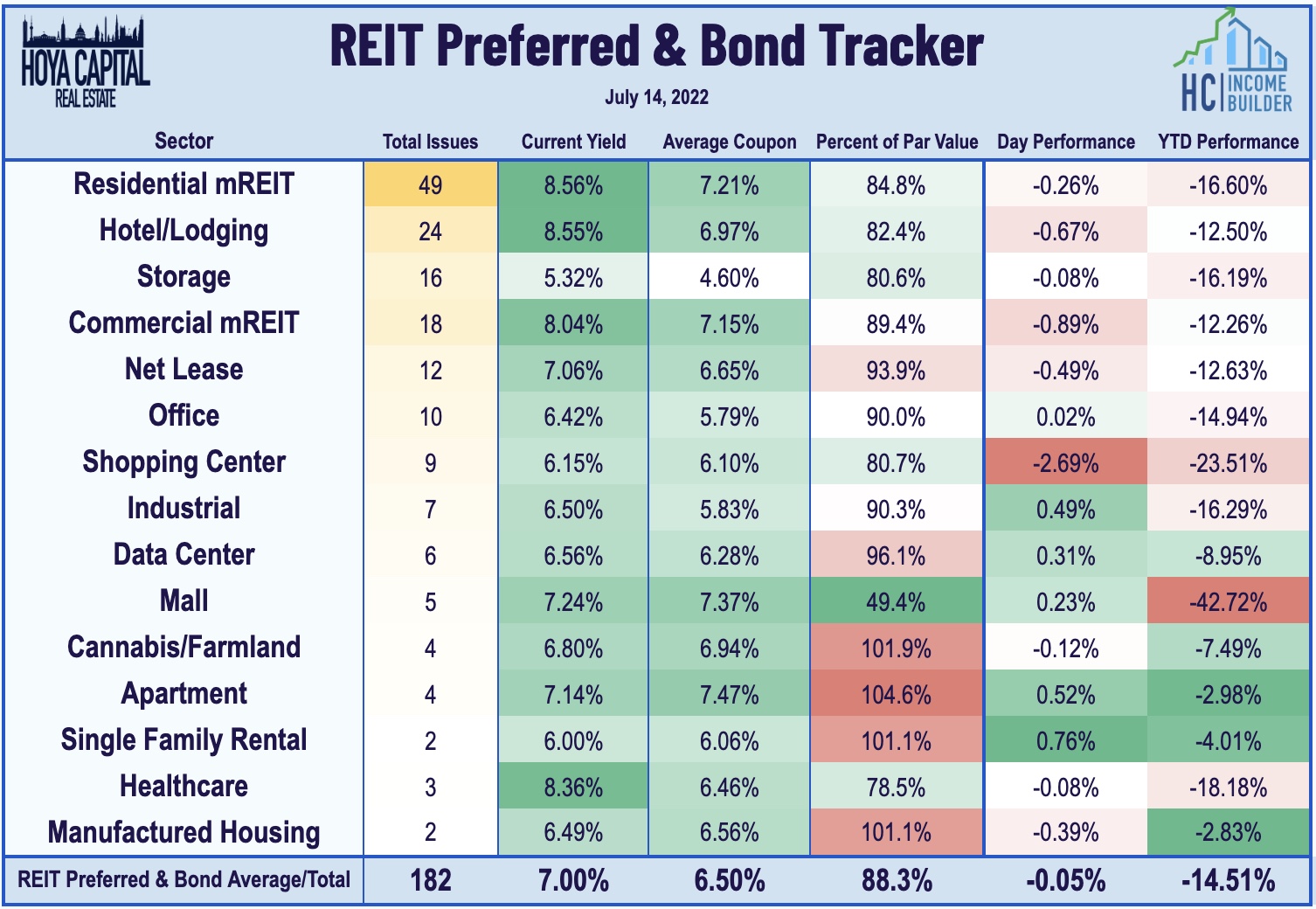

Per the Income Builder Preferred Tracker available to Income Builder subscribers, REIT Preferred stocks finished lower by 0.05% today, on average. REIT Preferreds are lower by roughly 10% on a total return basis this year after ending 2021 with price returns of roughly 8.0% and total returns of roughly 14%. There are now roughly 180 REIT-issued exchange-listed preferred and debt securities with an average current yield of 6.97%.

On Friday, we'll also see Retail Sales for June and get our first look at Michigan Consumer Sentiment for July. Last month, sentiment fell to the lowest level in more than 10 years as persistent inflation and worries over economic growth have weighed on confidence. We'll publish a full analysis and commentary of this week's developments in the real estate industry, as well as an analysis of the busy week of economic data in our Real Estate Weekly Outlook published this weekend.

Disclosure: Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index. Index definitions and a complete list of holdings are available on our website.

Hoya Capital Research & Index Innovations (“Hoya Capital”) is an affiliate of Hoya Capital Real Estate, a registered investment advisory firm based in Rowayton, Connecticut that provides investment advisory services to ETFs, individuals, and institutions. Hoya Capital Research & Index Innovations provides non-advisory services including market commentary, research, and index administration focused on publicly traded securities in the real estate industry.

This published commentary is for informational and educational purposes only. Nothing on this site nor any commentary published by Hoya Capital is intended to be investment, tax, or legal advice or an offer to buy or sell securities. This commentary is impersonal and should not be considered a recommendation that any particular security, portfolio of securities, or investment strategy is suitable for any specific individual, nor should it be viewed as a solicitation or offer for any advisory service offered by Hoya Capital Real Estate. Please consult with your investment, tax, or legal adviser regarding your individual circumstances before investing.

The views and opinions in all published commentary are as of the date of publication and are subject to change without notice. Information presented is believed to be factual and up-to-date, but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. Any market data quoted represents past performance, which is no guarantee of future results. There is no guarantee that any historical trend illustrated herein will be repeated in the future, and there is no way to predict precisely when such a trend will begin. There is no guarantee that any outlook made in this commentary will be realized.

Readers should understand that investing involves risk and loss of principal is possible. Investments in real estate companies and/or housing industry companies involve unique risks, as do investments in ETFs. The information presented does not reflect the performance of any fund or other account managed or serviced by Hoya Capital Real Estate. An investor cannot invest directly in an index and index performance does not reflect the deduction of any fees, expenses or taxes.

Hoya Capital Real Estate and Hoya Capital Research & Index Innovations have no business relationship with any company discussed or mentioned and never receives compensation from any company discussed or mentioned. Hoya Capital Real Estate, its affiliates, and/or its clients and/or its employees may hold positions in securities or funds discussed on this website and our published commentary. A complete list of holdings and additional important disclosures is available at www.HoyaCapital.com.