Rally Renewed • Storage Strength • Political Ad Spending

- U.S. equity markets rebounded Wednesday after oil prices slid to five-month-lows despite a disappointing OPEC production boost while investors expressed relief that U.S.-China tensions didn't further deteriorate following the Speaker's Taiwan visit.

- Following two days of declines, the S&P 500 rallied 1.6% today while the tech-heavy Nasdaq 100 advanced nearly 3% with China-exposed stocks leading the rebound.

- Real estate equities were mostly-higher today - led by self-storage and retail REITs - amid the busiest 24-hour stretch of earnings season. The Equity REIT Index advanced 0.3% today.

- ExtraSpace (EXR) was among the leaders today after kicking off storage REIT earnings season with a very strong report. EXR raised its full-year outlook for the third time this year and now sees FFO growth of 21.6% - up 330 basis points from its prior target.

- Billboard REIT Lamar (LAMR) was also an upside standout after reporting solid results and reaffirming its full-year outlook which calls for FFO growth of 10.4%. Political ad spending has been especially strong, rising 82% in '22 over 2020.

Real Estate Daily Recap

U.S. equity markets rebounded Wednesday after oil prices slid to five-month-lows despite a disappointing OPEC production boost while investors expressed relief that U.S.-China tensions didn't further deteriorate following the Speaker's Taiwan visit. Following two days of declines, the S&P 500 rallied 1.6% today while the tech-heavy Nasdaq 100 advanced by nearly 3% China-exposed stocks leading the rebound. Real estate equities were mostly-higher today - led by self-storage and retail REITs - amid the busiest 24-hour stretch of earnings season. The Equity REIT Index advanced 0.3% today with all 10-of-18 property sectors in positive territory while the Mortgage REIT Index rebounded 0.7%.

Real Estate Daily Recap

Best & Worst Performance Today Across the REIT Sector

Storage: ExtraSpace (EXR) was among the leaders today after kicking off storage REIT earnings season with a very strong report. EXR raised its full-year outlook for the third time this year and now sees FFO growth of 21.6% - up 330 basis points from its prior target - and NOI growth of 20.0% - up 350 basis points. As noted in our report last month, few REIT sectors have defied expectations as comprehensively as storage REITs since the start of the pandemic, and while several pandemic-fueled tailwinds are waning, the long-term outlook remains quite compelling. We'll hear results this afternoon from Life Storage (LSI) and National Storage (NSA) while CubeSmart (CUBE) and Public Storage (PSA) report results tomorrow after the close.

Billboard: Lamar Advertising (LAMR) - which we own in the REIT Dividend Growth Portfolio - was among the leaders today after reporting solid results and reaffirming its full-year outlook which calls for FFO growth of 10.4%. LAMR commented that it saw "strong growth across all business lines and geographies" with billboard revenue up more than 10% while its transit business has now recovered to pre-COVID levels following sharp revenue declines in 2020. Despite recession concerns, Lamar noted that was able to push pricing in Q2 with rates up "high single-digits" versus Q2 2021. Of note, LAMR reported that it's seeing particular strength in political advertising, which is up 82% in '22 over 2020 with about 50% of that spend on its digital platform, which Lamar is "aggressively" growing with 250-300 analog-to-digital conversions now expected this year. We'll hear results this afternoon from Outfront Media (OUT).

Net Lease: National Retail (NNN) was among the leaders today after raising its full-year FFO outlook for the third time this year, citing "continued operational momentum through the second quarter." NNN raised its FFO growth target to 8.2% - up 170 basis points from its prior outlook. - while also raising its acquisition target to $650M. Agree Realty (ADC) finished slightly lower after reporting in-line results with its Core FFO increasing 12.5% through the first half of 2022. While ADC does not provide FFO guidance, it did raise its full-year acquisition target to $1.6B from $1.5B. It'll be a busy afternoon for net lease REITs with reports from Realty Income (O), Store Capital (STOR), Spirit Realty (SRC), Broadstone (BNL), and Postal Realty (PSTL).

Shopping Center: Kite Realty (KRG) - which we own in the REIT Focused Income Portfolio - rallied nearly 3% after reporting another strong quarter and raising its full-year outlook. Driven by strong leasing activity with 13% blended cash spread, KRG now projects FFO growth of 22.0% this year - up 400 basis points from last quarter - and 10.2% above its pre-pandemic 2019 rate, the strongest in the shopping center REIT sector. Urban Edge (UE) gained after reporting its highest volume of lease activity over six years at spreads that rose 9.6% on a cash basis and 19.0% on a straight-line basis. Acadia Realty (AKR) finished lower after reporting better-than-expected core results, but revising its full-year outlook lower due to the negative mark-to-market declines in its investment in Albertsons. Whitestone (WSR) also slumped more than 4% after reporting in-line results and maintaining its full-year FFO and NOI outlook. We'll hear results this afternoon from RPT Realty (RPT) and Necessity Retail (RTL).

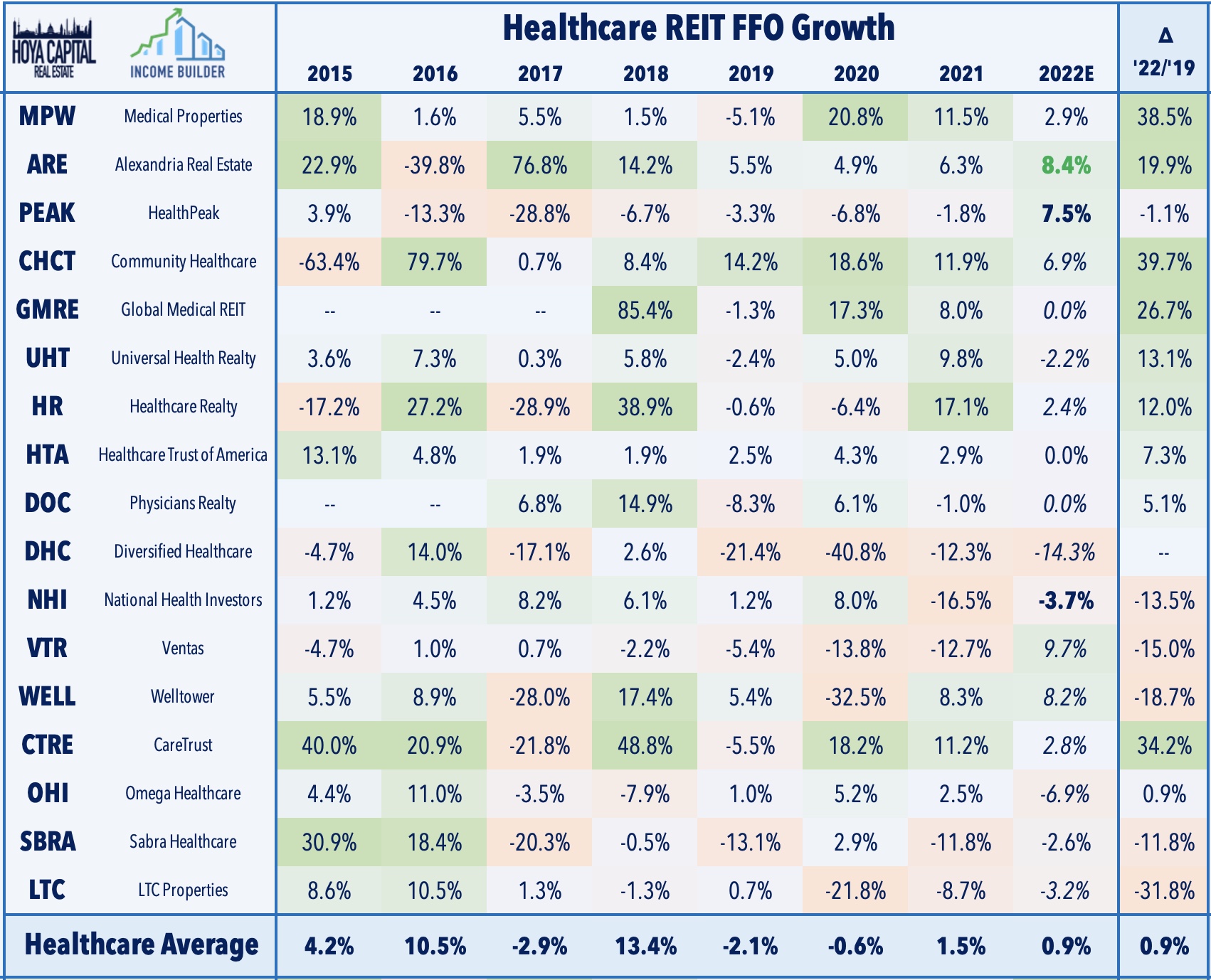

Healthcare: Healthpeak (PEAK) finished modestly lower after maintaining its full-year FFO growth outlook while boosting its full-year NOI growth outlook. PEAK reaffirmed its full-year FFO target which calls for growth of 7.5% and now sees NOI growth of 4.25% - up from 4.0% last quarter. For the quarter, PEAK's Life Sciences and MOB segments recorded NOI growth of 4.3% and 4.5%, respectively, while its CCRC segment remains a drag with a -2.1% decline. We'll hear results this afternoon from Global Medical REIT (GMRE) and Diversified Healthcare (DHC).

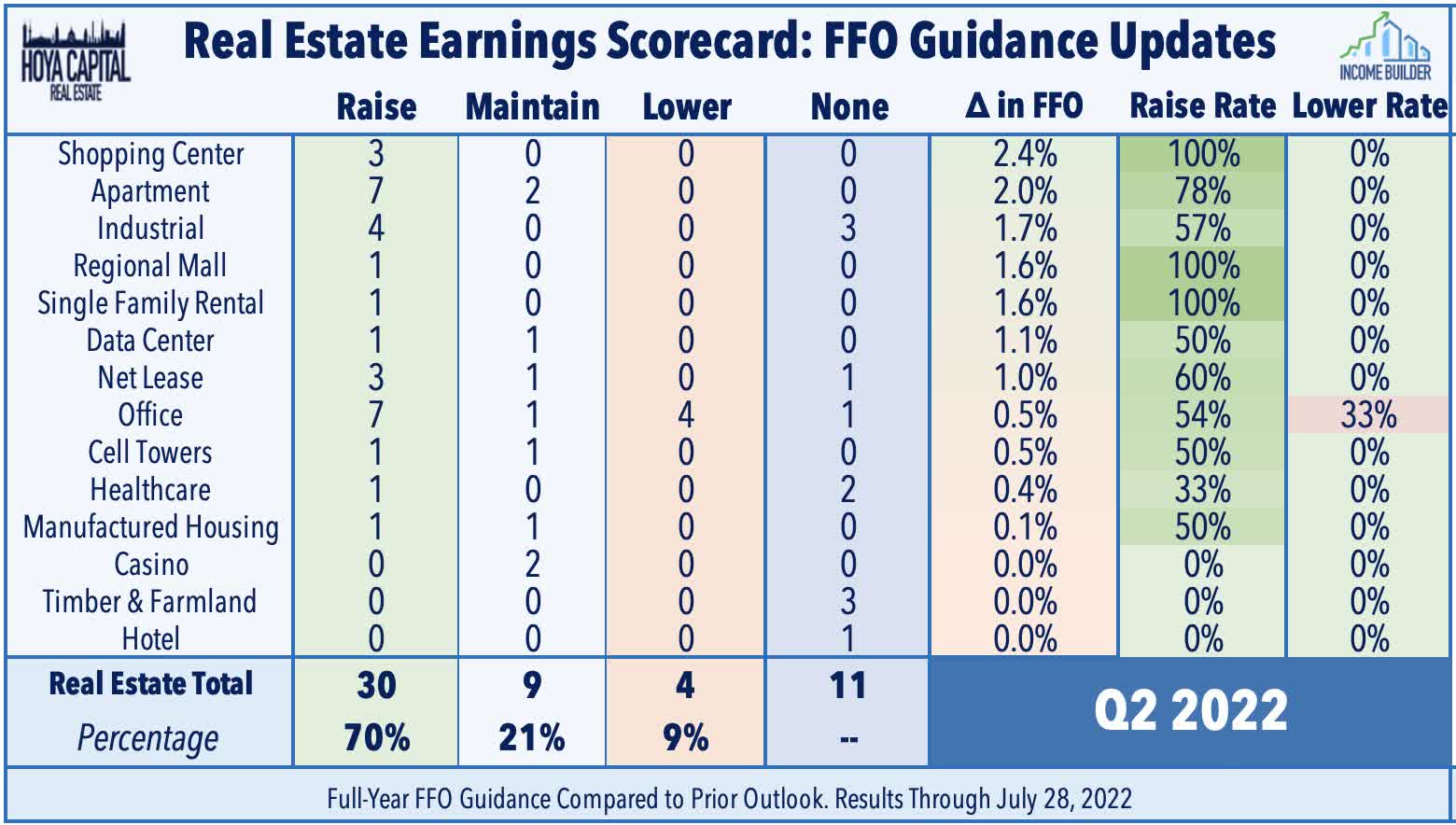

Earlier this week we published our Real Estate Earnings Halftime Report. REIT earnings have been quite impressive thus far with upside standouts being Apartment, Shopping Center, and Industrial REITs. In addition to the aforementioned REITs, we'll also hear earnings reports this afternoon from cannabis REIT Innovative Industrial (IIPR), manufactured housing REIT UMH Properties (UMH), industrial REIT Terreno (TRNO), along with a handful of hotel REITs: Host (HST), Hersha (HT), Braemar (BHR), and Diamondrock (DRH). We'll continue to provide real-time coverage for Hoya Capital Income Builder members and will publish follow-up articles summarizing our thoughts and analysis throughout earnings season.

Mortgage REIT Daily Recap

Per the REIT Rankings Tracker available to Income Builder subscribers, mortgage REITs were mostly-higher today following a busy slate of earnings reports with residential mREITs advancing 0.2% while commercial mREITs gained 0.3%. PennyMac Mortgage (PMT) was among the leaders today after reporting better-than-expected results highlighted by a relatively modest 7.2% decline in its Book Value Per Share ("BVPS") during the quarter - below the average reported decline of about 9% thus far amid a historically brutal quarter for residential MBS valuations. New York Mortgage Trust (NYMT) also gained 0.3% after that its BVPS declined by 6.9%. The busy slate of earnings reports continues with results tomorrow from Starwood Capital (STWD), Two Harbors (TWO), and Chimera Investment (CIM).

REIT Preferreds & Capital Raising

Per the Income Builder Preferred Tracker available to Income Builder subscribers, REIT Preferred stocks finished higher by 0.48% today, on average. REIT Preferreds are lower by roughly 5% on a total return basis this year after ending 2021 with price returns of roughly 8.0% and total returns of roughly 14%. There are now roughly 180 REIT-issued exchange-listed preferred and debt securities with an average current yield of 6.89%.

Economic Data This Week

Employment data highlights another busy week of economic data and corporate earnings reports in the week ahead, headlined by JOLTS data on Tuesday, Jobless Claims on Thursday, and the BLS Nonfarm Payrolls report on Friday. Economists are looking for job growth of roughly 250k in July which would be the lowest month-over-month increase since the start of the pandemic as the U.S. has now recovered 95% of the 22 million jobs lost from the COVID-related economic shutdowns. The unemployment rate, meanwhile, is expected to stay steady at 3.6%. Purchasing Managers' Index ("PMI") data will continue to be a major market focus - particularly in Europe and Asia - as recent reports have barely managed to hold on to the breakeven 50-level.

Disclosure: Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index. Index definitions and a complete list of holdings are available on our website.

Hoya Capital Research & Index Innovations (“Hoya Capital”) is an affiliate of Hoya Capital Real Estate, a registered investment advisory firm based in Rowayton, Connecticut that provides investment advisory services to ETFs, individuals, and institutions. Hoya Capital Research & Index Innovations provides non-advisory services including market commentary, research, and index administration focused on publicly traded securities in the real estate industry.

This published commentary is for informational and educational purposes only. Nothing on this site nor any commentary published by Hoya Capital is intended to be investment, tax, or legal advice or an offer to buy or sell securities. This commentary is impersonal and should not be considered a recommendation that any particular security, portfolio of securities, or investment strategy is suitable for any specific individual, nor should it be viewed as a solicitation or offer for any advisory service offered by Hoya Capital Real Estate. Please consult with your investment, tax, or legal adviser regarding your individual circumstances before investing.

The views and opinions in all published commentary are as of the date of publication and are subject to change without notice. Information presented is believed to be factual and up-to-date, but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. Any market data quoted represents past performance, which is no guarantee of future results. There is no guarantee that any historical trend illustrated herein will be repeated in the future, and there is no way to predict precisely when such a trend will begin. There is no guarantee that any outlook made in this commentary will be realized.

Readers should understand that investing involves risk and loss of principal is possible. Investments in real estate companies and/or housing industry companies involve unique risks, as do investments in ETFs. The information presented does not reflect the performance of any fund or other account managed or serviced by Hoya Capital Real Estate. An investor cannot invest directly in an index and index performance does not reflect the deduction of any fees, expenses or taxes.

Hoya Capital Real Estate and Hoya Capital Research & Index Innovations have no business relationship with any company discussed or mentioned and never receives compensation from any company discussed or mentioned. Hoya Capital Real Estate, its affiliates, and/or its clients and/or its employees may hold positions in securities or funds discussed on this website and our published commentary. A complete list of holdings and additional important disclosures is available at www.HoyaCapital.com.