Fed Ahead • REIT Earnings • Spooky Economic Data

- U.S. equity markets slumped Monday- but held onto sizable monthly gains- as investors eyed a frenetic week of economic data, corporate earnings reports, and the Federal Reserve interest rate decision.

- Coming off its best two-week advance since November 2020, the S&P 500 declined 0.7% today while the tech-heavy Nasdaq 100 dipped 1.2%. The Mid-Cap 400 and Small-Cap 600 finished flat.

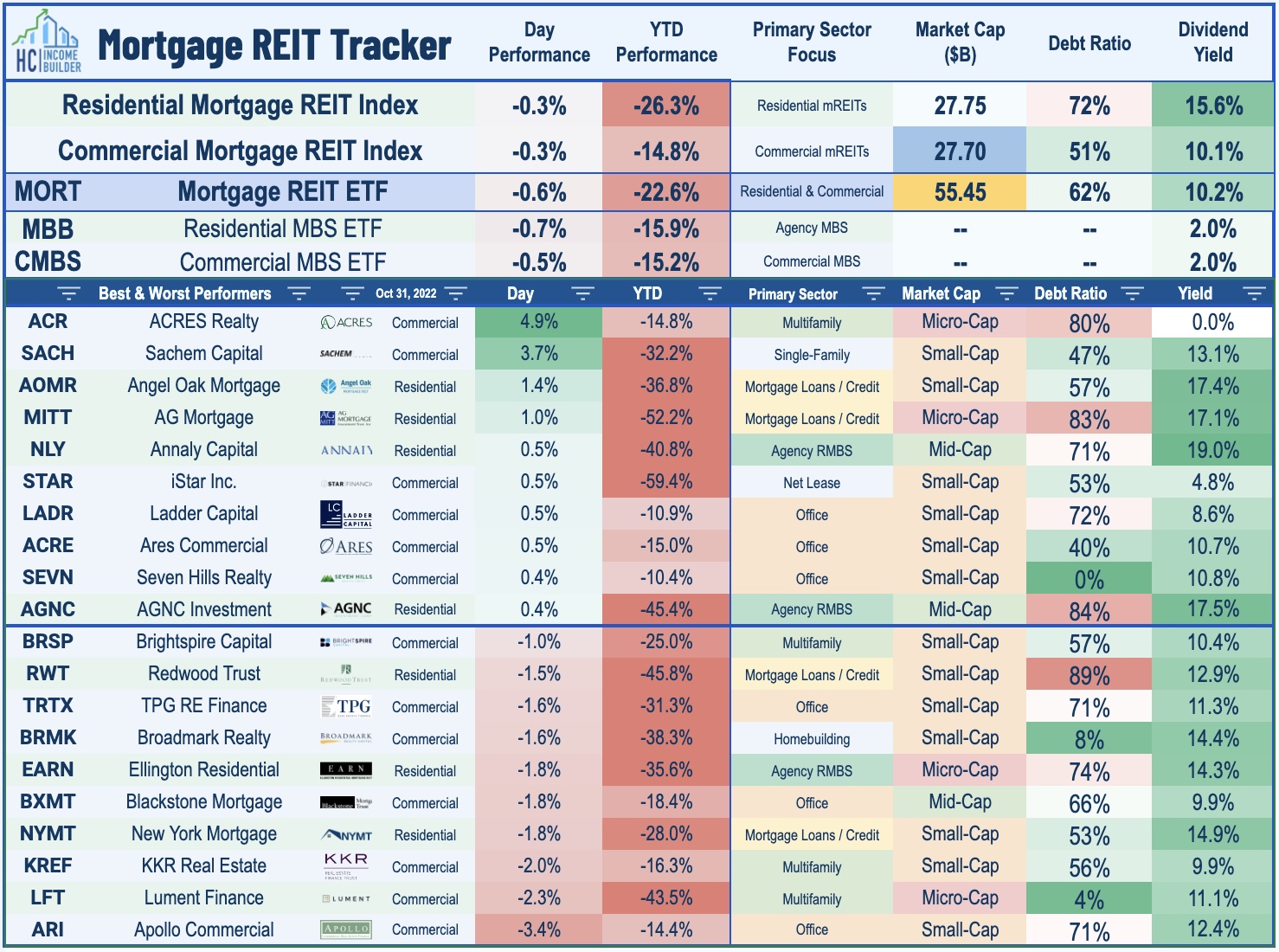

- Real estate equities were mixed today ahead of the busiest week of earnings season. Following its best week since November 2020, the Equity REIT Index declined 0.1% while Mortgage REITs declined 0.7%.

- The busy week of economic data got off to a "spooky" start today with Chicago PMI falling to the lowest-level since June 2020 while the Dallas Fed Manufacturing Survey was similarly weaker-than-expected, falling for a sixth consecutive month.

- Apartment List released their National Rent Report this morning which showed a second-straight monthly decline in rents in October - marking a continued cooldown from the record-high pace of rent increases seen in early 2022.

Income Builder Daily Recap

U.S. equity markets slumped Monday - but held onto sizable monthly gains for October - as investors eyed a frenetic week of economic data, corporate earnings reports, and the Federal Reserve interest rate decision. Coming off its best two-week advance since November 2020, the S&P 500 declined 0.7% today while the tech-heavy Nasdaq 100 dipped 1.2%. The Mid-Cap 400 and Small-Cap 600 were each roughly flat. Real estate equities were mixed today ahead of the busiest week of earnings season with nearly 100 REITs reporting results. Following its best week since November 2020, the Equity REIT Index finished lower by 0.1% today while the Mortgage REIT Index declined 0.7%. Homebuilders declined nearly 2% following a strong rebound last week.

The busy week of economic data got off to a "spooky" start today with Chicago PMI falling to the lowest-level since June 2020 while the Dallas Fed Manufacturing Survey was similarly weaker-than-expected, falling for a sixth consecutive month. The U.S. Dollar rallied nearly 1% as investors digested close election results in Brazil which continued a recent leftward swing in Latin American politics. The 10-Year Treasury Yield climbed 7 basis points to close at 4.08% today with the Fed expected to raise the upper-bound of its policy rate by 75 basis points to 4.0% this week. With midterm elections in the U.S. now just one week away, Energy (XLE) stocks were the top-performing GICS sector today despite President Biden's plans to ask Congress to pursue "windfall" tax penalties for oil and gas companies.

It'll be another jam-packed week of economic data and corporate earnings results with the main event coming on Wednesday with the FOMC Interest Rate Decision on Wednesday, in which the Fed is widely expected to raise rates by 75 basis points to bring the Fed Funds rate to a 4.0% upper-bound. Jobs data highlights the busy economic data slate with JOLTS data on Tuesday, ADP Payrolls on Wednesday, Jobless Claims data on Thursday and the BLS Nonfarm Payrolls report on Friday. Economists are looking for job growth of roughly 200k in October - which would be the smallest gain since December 2020 - and for the unemployment rate to tick higher to 3.60%. 'Good news is bad news' will likely be the theme of these reports as investors and the Fed look for signs of the long-awaited cooldown in job growth which has yet to fully materialize. Purchasing Managers' Index ("PMI") data will continue to be a major market focus - particularly in Europe and Asia - as recent reports have dipped below the breakeven 50-level.

Real Estate Daily Recap

Best & Worst Performance Today Across the REIT Sector

Office: Small-cap Alexanders' (ALX) - which owns six Class A office assets in New York City with Bloomberg LP as its largest tenant - was among the leaders today after reporting in-line results. We've seen results from 12 of the 24 hotel REITs, of which six have raised their full-year FFO growth outlooks while five have maintained their outlook. Consistent with recent data from Kastle Systems, Sunbelt-focused office REITs have been the upside standout thus far, highlighted by a guidance raise from Highwoods (HIW) while Cousins (CUZ) and Brandywine (BDN) also reported notable strength in their Sunbelt markets. Results from coastal-focused REITs have been shakier - with the exception of the lab space segment which has seen continued robust leasing demand per reports from Kilroy (KRC) and Boston Properties (BXP). We'll hear results this afternoon from office REIT Vornado (VNO).

Apartment: Brokerage firm Apartment List released their National Rent Report this morning which showed a second-straight monthly decline in rents in October - marking a continued cooldown from the record-high pace of rent increases seen in early 2022. While a seasonal cooldown is typical after the peak summer rental season, its rent index noted a more significant decline than in past years, recording a 0.7% decline in October, which was the largest single-month dip since 2017. Despite the monthly decline, rent growth over the course of this year continues to outpace the pre-pandemic trend, even as it has slowed significantly from last year’s peaks with rents higher by 5.9% since the start of the year. The recent slowdown has been geographically widespread with rents declining in 89 of the nation’s 100 largest cities in October. We'll hear results this afternoon from apartment REIT Centerspace (CSR) and from AvalonBay on Thursday.

Last Friday we published REIT Earnings Halftime Report. At the halfway point of earnings season, of the 41 REITs that have provided full-year Funds From Operations ("FFO") guidance, 28 REITs (67%) raised their outlook while just 4 REITs (10%) have lowered their outlook. Solid results from REITs come amid an otherwise disappointing earnings season for the broader equity market as, per FactSet, just 48% of S&P 500 companies have boosted their outlook. In addition to the aforementioned reports, we'll hear results this afternoon from hotel REIT Ryman Hospitality (RPH) and cell tower REIT SBA Communications (SBAC). Tomorrow morning, we'll see results from Simon Property (SPG), Easterly Government (DEA), and Safehold (SAFE).

Mortgage REIT Daily Recap

Per the REIT Rankings Tracker available to Income Builder subscribers, mortgage REITs were roughly flat today ahead of a busy week of earnings reports following a double-digit rally last week. We'll hear results from 18 mortgage REITs this week including New York Mortgage Trust (NYMT) and Chimera (CIM) on Tuesday, Rithm Capital (RITM) and Ares Commercial (ACRE) on Wednesday, Hannon Armstrong (HASI) and Invesco Mortgage (IVR) on Thursday, and Arbor Realty (ABR) on Friday. Results thus far have been significantly better than expected - particularly for commercial mREITs and non-agency residential mREITs - despite the historically brutal quarter for lending markets with average BVPS declines of roughly 7.5% thus far.

Disclosure: Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index. Index definitions and a complete list of holdings are available on our website.

Hoya Capital Research & Index Innovations (“Hoya Capital”) is an affiliate of Hoya Capital Real Estate, a registered investment advisory firm based in Rowayton, Connecticut that provides investment advisory services to ETFs, individuals, and institutions. Hoya Capital Research & Index Innovations provides non-advisory services including market commentary, research, and index administration focused on publicly traded securities in the real estate industry.

This published commentary is for informational and educational purposes only. Nothing on this site nor any commentary published by Hoya Capital is intended to be investment, tax, or legal advice or an offer to buy or sell securities. This commentary is impersonal and should not be considered a recommendation that any particular security, portfolio of securities, or investment strategy is suitable for any specific individual, nor should it be viewed as a solicitation or offer for any advisory service offered by Hoya Capital Real Estate. Please consult with your investment, tax, or legal adviser regarding your individual circumstances before investing.

The views and opinions in all published commentary are as of the date of publication and are subject to change without notice. Information presented is believed to be factual and up-to-date, but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. Any market data quoted represents past performance, which is no guarantee of future results. There is no guarantee that any historical trend illustrated herein will be repeated in the future, and there is no way to predict precisely when such a trend will begin. There is no guarantee that any outlook made in this commentary will be realized.

Readers should understand that investing involves risk and loss of principal is possible. Investments in real estate companies and/or housing industry companies involve unique risks, as do investments in ETFs. The information presented does not reflect the performance of any fund or other account managed or serviced by Hoya Capital Real Estate. An investor cannot invest directly in an index and index performance does not reflect the deduction of any fees, expenses or taxes.

Hoya Capital Real Estate and Hoya Capital Research & Index Innovations have no business relationship with any company discussed or mentioned and never receives compensation from any company discussed or mentioned. Hoya Capital Real Estate, its affiliates, and/or its clients and/or its employees may hold positions in securities or funds discussed on this website and our published commentary. A complete list of holdings and additional important disclosures is available at www.HoyaCapital.com.