Powell Pop • Mall Earnings • REIT Dividend Hikes

- U.S. equity markets rebounded Tuesday after Fed Chair Powell maintained a decidedly less-hawkish tone in public remarks, easing concerns that blowout employment data would prompt a reversal.

- Snapping a two-day skid, the S&P 500 rebounded 1.3% today while the tech-heavy Nasdaq 100 rallied 0.8%. The Dow added 266 points.

- Real estate equities were mixed today as REIT earnings season kicked into gear. Equity REITs declined 0.3% but Mortgage REITs gained 1.2% and Homebuilders rallied 1.5%.

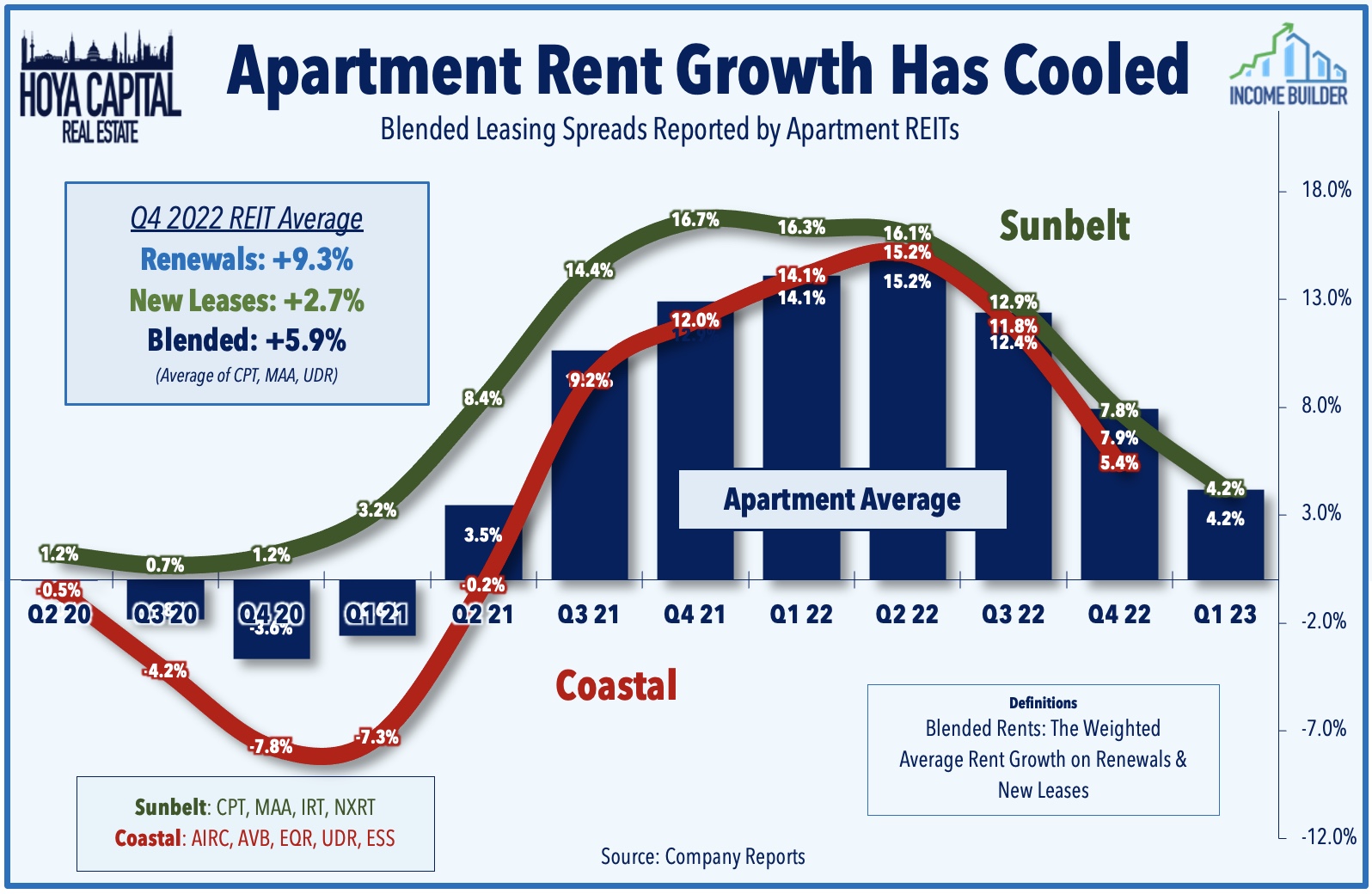

- Apartment REIT UDR (UDR) rallied more than 3% after reporting better-than-expected results and hiking its dividend, noting that its FFO climbed 15.9% for full-year 2022 and projected solid FFO growth of 7.1%.

- Mall REIT Simon Property (SPG) declined 2% despite reporting decent results highlighted by a recovery in occupancy rates to levels that exceeded 2019-levels. Macerich (MAC) dipped 3% after reporting relatively weaker results with occupancy rates still 100 basis points below 2019-levels.

Income Builder Daily Recap

U.S. equity markets rebounded Tuesday after Fed Chair Powell maintained a decidedly less-hawkish tone in public remarks, easing concerns that blowout employment data would prompt a reversal. Snapping a two-day skid, the S&P 500 rebounded 1.3% today while the tech-heavy Nasdaq 100 rallied 0.8%. The Dow added 266 points. Real estate equities were mixed today as REIT earnings season kicked into gear. The Equity REIT Index declined 0.3% today with 6-of-18 property sectors in positive territory while the Mortgage REIT Index gained 1.2% and Homebuilders rallied 1.5%.

After two days of sharp selling pressure across fixed-income markets, the 10-Year Treasury Yield stabilized today after Federal Reserve Chair Powell passed on an opportunity to project a more hawkish tone in the wake of the robust BLS employment report last Friday and instead reiterated focused his commentary on data points pointing towards disinflation. Commodities prices rebounded today with Crude Oil rallying 3.5% while Natural Gas prices jumped more than 5% - continuing a two-day rally - as traders evaluated the supply impacts of a series of devastating earthquakes in Turkey and Syria which closed a key oil-export terminal. Eight of the eleven GICS equity sectors finished higher on the session with Energy (XLE) and Technology (XLK) stocks leading on the upside today while Consumer Staples (XLP) lagged.

Real Estate Daily Recap

Best & Worst Performance Today Across the REIT Sector

Mall: Simon Property (SPG) declined 2% despite reporting fairly upbeat results, noting that its FFO declined 0.6% in 2022 - slightly above the midpoint of its prior guidance - while projecting that its 2023 FFO will be roughly even with 2022. Comparable occupancy climbed to 94.9% in Q4 - up 150 basis points from last year and exceeding the average pre-pandemic occupancy rate of 94.8% in full-year 2019. Average base rents rose 2.3% in Q4, which was the highest since Q1 2020. Macerich (MAC) dipped 3% after reporting relatively weaker results, noting its FFO declined by 3.4% in 2022 - matching the midpoint of its prior guidance range - but projecting an 8.2% decline in FFO for full-year 2023. MAC's comparable occupancy rates rose to 92.7% - up 100 basis points from last year but still 100 basis points below its pre-pandemic level. Leasing spreads rose 0.3% on a trailing twelve-month basis, a deceleration from the 3.3% rate reported last quarter.

Apartment: Coastal-focused apartment REIT UDR (UDR) rallied more than 3% after reporting better-than-expected results, noting that its FFO climbed 15.9% for full-year 2022 - slightly shy of the midpoint of its guidance - but projected FFO growth of 7.1% at the midpoint of its 2023 range, well above consensus estimates. UDR achieved 9.3% rent growth on renewals and 2.0% on new leases for a blended rent growth rate of 5.4% in Q4 - roughly in-line with rent growth trends reported by Sunbelt-focused Mid-Amerca (MAA) and Camden (CPT) last week - as notable strength in its Southeast and Northeast markets offset weaker rent growth trends in the West. UDR also hiked its quarterly dividend by 10.5% to $0.42/share, the 8th REIT to hike its dividend this year. We'll hear earnings results after the close today from Essex (ESS).

Office: Today, we published Office REITs: Pain Is Priced In. Office REITs have been far-and-away the worst-performing property sector since the start of the pandemic as depressed utilization rates and recession concerns have curbed office space demand. Occupiers due for renewal have been somewhat-reluctant to cut office space with leasing volumes still at 75% of pre-pandemic levels, but fundamentals softened more definitively in late 2022. As employment markets normalize from historic tightness, we believe that utilization rates should recover to around 60% in urban metros and 80% in secondary markets – up about 20% from current levels - likely a more optimistic view than market consensus. With Office REITs trading at historically deep discounts to peers in public and private markets there appear to be some emerging pockets of value, particularly in Sunbelt and secondary markets. After the close today, we'll hear from Douglas Emmett (DEI), Highwoods (HIW), and American Assets (AAT).

In addition to the aforementioned reports, we'll also hear results this afternoon from industrial REIT Eastgroup (EGP), and healthcare REIT HealthPeak (PEAK). Tomorrow morning, we'll hear results from strip center REIT Site Centers (SITC). As discussed in our Earnings Preview, REITs entered earnings season with some positive momentum amid the recent moderation in interest rates and hopes of a 'softish' economic landing following a punishing year of stock price performance. How REITs are responding to this higher rate environment – both on the acquisitions and the financing side - will be closely watched. REITs hunkered down in 2022, but opportunities are becoming more plentiful and we see the non-traded REIT segment as one area that may be "ripe for the picking" if investor redemptions continue. Full-year FFO guidance will be the most closely watched metric, especially in the residential, retail, and office sectors given the wide range of expectations.

Additional Headlines from The Daily REITBeat on Income Builder

- Fitch Ratings affirmed the Long-Term Issuer Default Ratings of Kite Realty (KRG) at “BBB” with a stable outlook

- Armada Hoffler (AHH) announced that it has achieved an investment grade credit rating from DBRS Morningstar at “BBB” with a stable trend

- Morningstar downgraded PSA to Hold from Buy

Mortgage REIT Daily Recap

Per the REIT Rankings Tracker available to Income Builder subscribers, mortgage REITs rebounded today after a sharp sell-off on Monday with residential mREITs advancing 0.8% today while commercial mREITs gained 0.8%. KKR Real Estate (KREF) reported results after the close today, noting that its Book Value Per Share ("BVPS") declined 1.5% in Q4. We'll hear results from Armour Residential (ARR), Ares Commercial (ACRE), and Chimera (CIM) on Wednesday, and from Hannon Armstrong (HASI) on Thursday.

Economic Data This Week

As discussed in our Weekly Outlook, while earnings season kicks into high gear this week, the economic calendar slows down following a busy two-week stretch. We'll hear from a number of Federal Reserve officials throughout the week including Fed Chair Powell, who spoke at the Economic Club of Washington on Tuesday. We'll be closely watching Jobless Claims data on Thursday as well for any signs of cracks in the seemingly unwavering labor market. On Friday, we'll get our first look at Michigan Consumer Sentiment data for February which includes a closely-watched consumer inflation expectations survey. Consumer Sentiment - which has tracked closely with consumer gasoline prices over the past two years - has rebounded in recent months since hitting its lowest-level on record in mid-2022.

Disclosure: Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index. Index definitions and a complete list of holdings are available on our website.

Hoya Capital Research & Index Innovations (“Hoya Capital”) is an affiliate of Hoya Capital Real Estate, a registered investment advisory firm based in Rowayton, Connecticut that provides investment advisory services to ETFs, individuals, and institutions. Hoya Capital Research & Index Innovations provides non-advisory services including market commentary, research, and index administration focused on publicly traded securities in the real estate industry.

This published commentary is for informational and educational purposes only. Nothing on this site nor any commentary published by Hoya Capital is intended to be investment, tax, or legal advice or an offer to buy or sell securities. This commentary is impersonal and should not be considered a recommendation that any particular security, portfolio of securities, or investment strategy is suitable for any specific individual, nor should it be viewed as a solicitation or offer for any advisory service offered by Hoya Capital Real Estate. Please consult with your investment, tax, or legal adviser regarding your individual circumstances before investing.

The views and opinions in all published commentary are as of the date of publication and are subject to change without notice. Information presented is believed to be factual and up-to-date, but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. Any market data quoted represents past performance, which is no guarantee of future results. There is no guarantee that any historical trend illustrated herein will be repeated in the future, and there is no way to predict precisely when such a trend will begin. There is no guarantee that any outlook made in this commentary will be realized.

Readers should understand that investing involves risk and loss of principal is possible. Investments in real estate companies and/or housing industry companies involve unique risks, as do investments in ETFs. The information presented does not reflect the performance of any fund or other account managed or serviced by Hoya Capital Real Estate. An investor cannot invest directly in an index and index performance does not reflect the deduction of any fees, expenses or taxes.

Hoya Capital Real Estate and Hoya Capital Research & Index Innovations have no business relationship with any company discussed or mentioned and never receives compensation from any company discussed or mentioned. Hoya Capital Real Estate, its affiliates, and/or its clients and/or its employees may hold positions in securities or funds discussed on this website and our published commentary. A complete list of holdings and additional important disclosures is available at www.HoyaCapital.com.