Fed Chatter • REIT Earnings • Stocks Slip

- U.S. equity markets retreated Wednesday while bond markets snapped a three-day skid as investors analyzed a busy slate of corporate earnings reports and hawkish chatter from Federal Reserve officials.

- Erasing much of yesterday's rebound, the S&P 500 slipped 1.1% today while the tech-heavy Nasdaq 100 declined 1.8%. The Dow slipped 208 points.

- Real estate equities were among the better-performers today following a generally solid slate of earnings reports. Equity REITs declined 0.5% while Mortgage REITs finished lower by 1.3%.

- West Coast-focused apartment REIT Essex Properties (ESS) rallied 2% after reporting decent fourth-quarter results. Despite a cooldown in rent growth and an uptick in unpaid rents, ESS expects FFO growth of 2% in 2023 following 16.2% growth in 2022.

- Site Centers (SITC) gained 0.5% after it reported decent results highlighted by a continued acceleration in rental rates with new lease cash spreads of 55.2% and renewal spreads of 7.6%. SITC reported interest in potentially vacated space from Party City and Bed Bath.

Income Builder Daily Recap

U.S. equity markets retreated Wednesday while bond markets snapped a three-day skid as investors analyzed a busy slate of corporate earnings reports and commentary from Federal Reserve officials. Erasing much of yesterday's rebound, the S&P 500 slipped 1.1% today while the tech-heavy Nasdaq 100 declined 1.8%. The Dow slipped 208 points. Bonds caught a bid with the 10-Year Treasury Yield retreating for the first time since Friday's jobs report, ending the session lower by 2 basis points to 3.65%. Real estate equities were among the better performers today following a generally solid slate of earnings reports. The Equity REIT Index declined 0.5% today with 3-of-18 property sectors in positive territory while the Mortgage REIT Index declined 1.3%.

Real Estate Daily Recap

Best & Worst Performance Today Across the REIT Sector

Strip Centers: The first strip center REIT to report fourth-quarter earnings, Site Centers (SITC) gained 0.5% after it reported decent results highlighted by a continued acceleration in rental rates with new lease cash spreads of 55.2% and renewal spreads of 7.6%. Comparable occupancy rates climbed to 95.4% - up 40 basis points from last quarter and 270 bps from last year. SITC recorded full-year FFO growth of 0.9% in 2022 - slightly above its prior guidance - but projects a 3.4% decline in full-year FFO in 2023 at the midpoint of its initial guidance range, which incorporates projections that several bankrupt or near-bankrupt retailers will vacate space this year. SITC noted that several tenants are eying potentially-vacated space from Party City and Bed Bath (BBBY) and that it expects to pursue an "aggressive recapture of space" given the backlog of demand rather than renegotiate leases. After the close today, we'll hear results from Federal Realty (FRT) after the close today and from Kimco (KIM) tomorrow morning.

Apartment: The relatively strong start for residential REIT earnings season continued as West Coast-focused Essex Properties (ESS) rallied 2% after reporting decent fourth-quarter results, noting that its FFO climbed 16.2% for full-year 2022 - slightly above the midpoint of its guidance - but provided a fairly soft initial outlook for 2023, calling for FFO growth of 1.7% and market rent growth of 2% for the year. As expected, rent growth cooled in Q4 with ESS reporting 7.6% renewal spreads and 0.8% spreads on new leases for a blended rent growth rate of 3.8% while blended rent growth cooled further to 2.2% in January. ESS highlighted an uptick in unpaid rents in Q4 which ESS attributes to the ongoing eviction moratorium in California - headwinds that it expects will result in a 70 basis point drag to same-store revenues in full-year 2023. We'll hear earnings results after the close today from AvalonBay (AVB).

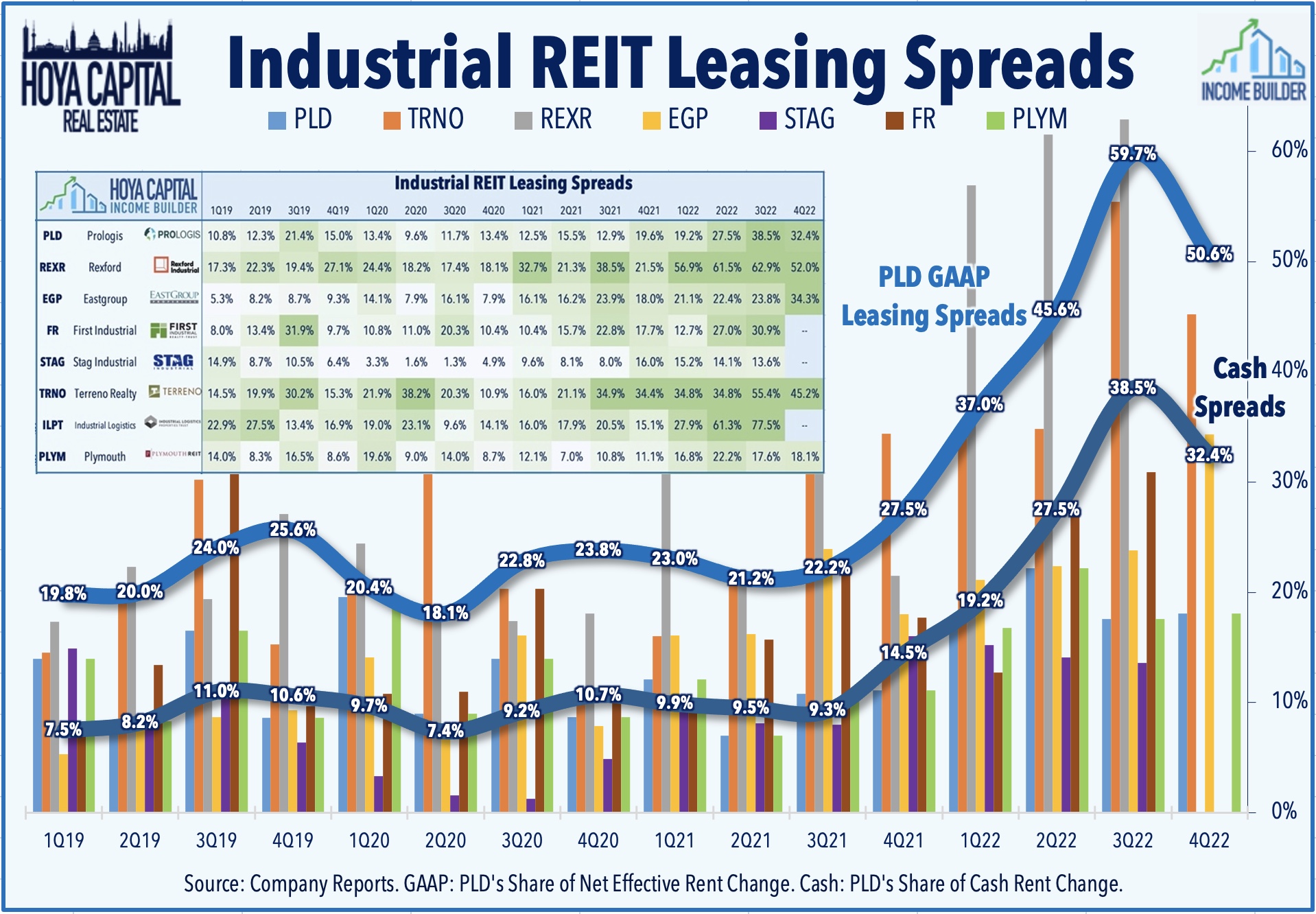

Industrial: Eastgroup (EGP) finished lower by about 1% today after reporting solid results, noting that it achieved FFO growth of 14.9% in 2022 - 110 basis points above its prior guidance - and provided initial 2023 guidance calling for FFO growth of 5.7%. Industrial property fundamentals in EGP's markets remain extremely strong, underscored by a sequential acceleration in rent spreads with rental rates on new and renewal leases increasing by 34.3% on a cash basis - its strongest quarter on record. EGP reported same-store NOI growth of 8.9% for full-year 2022 - also above its prior guidance - and its initial guidance for same-store NOI calls for growth of 6.0%. After the close today, we'll hear results from Rexford (REXR) and First Industrial (FR).

Office: Highwoods (HIW) was little-changed today after reporting in-line earnings results highlighted by FFO growth of 4.4% in full-year 2022 and a sequential increase in occupancy rates. HIW - which focuses on Sunbelt markets - recorded solid total leasing volume of 924k SF in Q4 which lifted its full-year total to 1.5 million - the highest in eight years. Douglas Emmett (DEI) - which focuses on urban Coastal markets - was also little-changed today after reporting mixed results with full-year 2022 FFO coming in shy of its prior guidance while its initial guidance for 2023 calls for a 6.4% decline in FFO. Leasing volume, occupancy, and rent spread metrics showed ongoing demand softness in its coastal markets with cash rents declining 9.9% from last year while occupancy rates declined another 20 basis points sequentially to 83.7%. After the close today, we'll hear from Hudson Pacific (HPP), Piedmont (PDM), and Equity Commonwealth (EQC).

Mortgage REIT Daily Recap

Per the REIT Rankings Tracker available to Income Builder subscribers, mortgage REITs were mixed today with residential mREITs slipping 0.4% today while commercial mREITs declined 2.5%. Rithm Capital (RITM) - which we own in the REIT Focused Income Portfolio - rallied more than 3% after reporting solid results with Q4 EPS of $0.33 - above expectations of $0.29 - while noting that its Book Value Per Share ("BVPS") was little-changed at $12.00. Blackstone Mortgage (BXMT) declined 4% after reporting mixed results with better-than-expected EPS of $0.87 offset by a -3.5% decline in its BVPS during Q4. KKR Real Estate (KREF) dipped more than 5% after missing EPS estimates and recording a -1.5% sequential decline in its BVPS. We'll hear results this afternoon from Annaly (NLY), Two Harbors (TWO), and Apollo Commerical (ARI).

Additional Headlines from The Daily REITBeat on Income Builder

- Chatham Lodging (CLDT) announced that it has repaid in full three mortgages with outstanding principal of $73.3 million and a weighted average interest rate of 8.0% with proceeds from its newly issued term loan which currently carries an interest rate of 6.1%.

- Medical Properties (MPW) announced that Lifepoint Health has completed its previously announced acquisition of Springstone Health. MPT sold for $205 million in cash its $190 million loan to Lifepoint while MPT will continue to own the 18 behavioral health hospitals it acquired.

Economic Data This Week

As discussed in our Weekly Outlook, while earnings season kicks into high gear this week, the economic calendar slows down following a busy two-week stretch. We'll hear from a number of Federal Reserve officials throughout the week including Fed Chair Powell, who spoke at the Economic Club of Washington on Tuesday. We'll be closely watching Jobless Claims data on Thursday as well for any signs of cracks in the seemingly unwavering labor market. On Friday, we'll get our first look at Michigan Consumer Sentiment data for February which includes a closely-watched consumer inflation expectations survey. Consumer Sentiment - which has tracked closely with consumer gasoline prices over the past two years - has rebounded in recent months since hitting its lowest-level on record in mid-2022.

Disclosure: Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index. Index definitions and a complete list of holdings are available on our website.

Hoya Capital Research & Index Innovations (“Hoya Capital”) is an affiliate of Hoya Capital Real Estate, a registered investment advisory firm based in Rowayton, Connecticut that provides investment advisory services to ETFs, individuals, and institutions. Hoya Capital Research & Index Innovations provides non-advisory services including market commentary, research, and index administration focused on publicly traded securities in the real estate industry.

This published commentary is for informational and educational purposes only. Nothing on this site nor any commentary published by Hoya Capital is intended to be investment, tax, or legal advice or an offer to buy or sell securities. This commentary is impersonal and should not be considered a recommendation that any particular security, portfolio of securities, or investment strategy is suitable for any specific individual, nor should it be viewed as a solicitation or offer for any advisory service offered by Hoya Capital Real Estate. Please consult with your investment, tax, or legal adviser regarding your individual circumstances before investing.

The views and opinions in all published commentary are as of the date of publication and are subject to change without notice. Information presented is believed to be factual and up-to-date, but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. Any market data quoted represents past performance, which is no guarantee of future results. There is no guarantee that any historical trend illustrated herein will be repeated in the future, and there is no way to predict precisely when such a trend will begin. There is no guarantee that any outlook made in this commentary will be realized.

Readers should understand that investing involves risk and loss of principal is possible. Investments in real estate companies and/or housing industry companies involve unique risks, as do investments in ETFs. The information presented does not reflect the performance of any fund or other account managed or serviced by Hoya Capital Real Estate. An investor cannot invest directly in an index and index performance does not reflect the deduction of any fees, expenses or taxes.

Hoya Capital Real Estate and Hoya Capital Research & Index Innovations have no business relationship with any company discussed or mentioned and never receives compensation from any company discussed or mentioned. Hoya Capital Real Estate, its affiliates, and/or its clients and/or its employees may hold positions in securities or funds discussed on this website and our published commentary. A complete list of holdings and additional important disclosures is available at www.HoyaCapital.com.