Volatility Eases • Movie Theater Deal? • NYC Office Lease

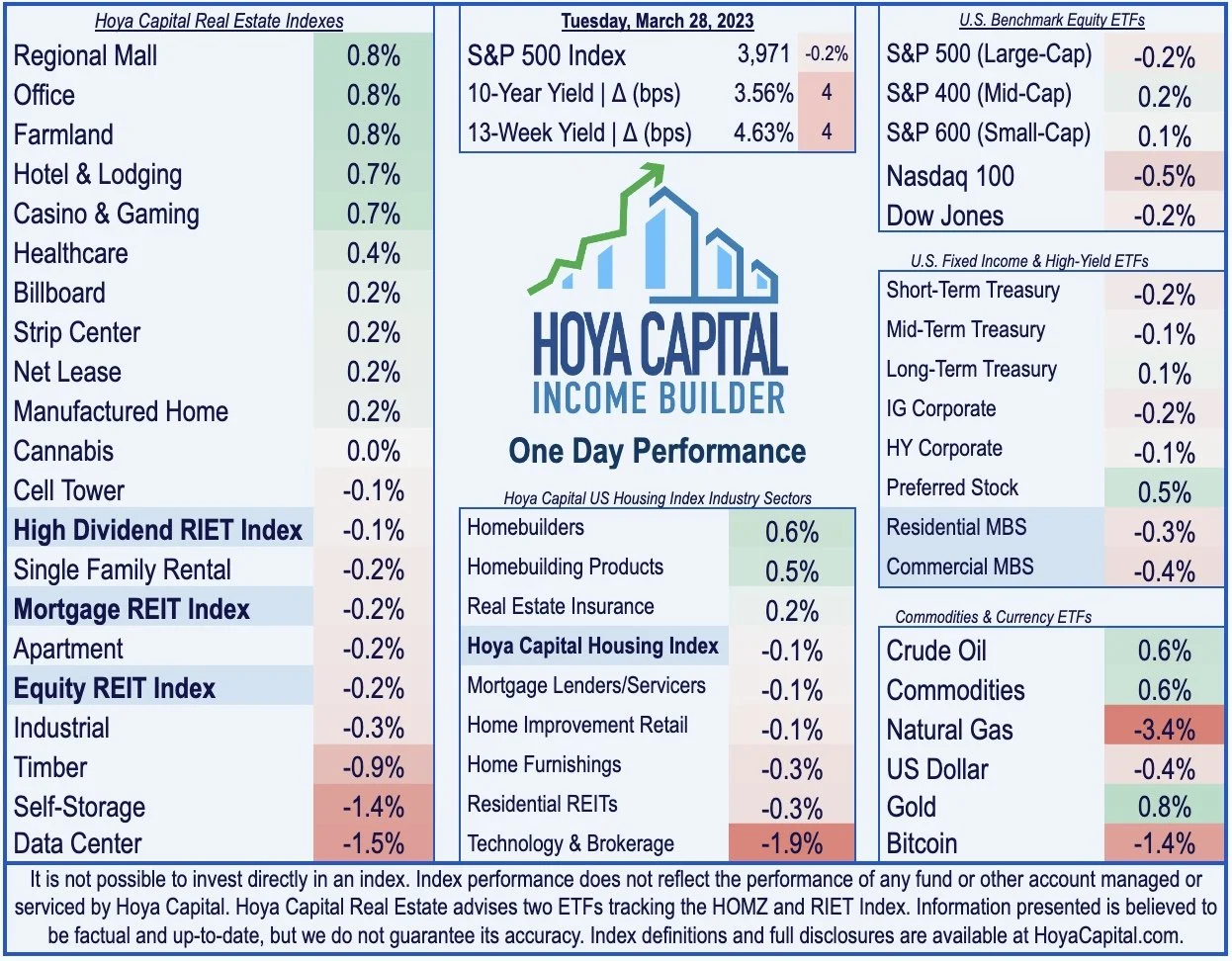

U.S. equity markets and bond markets finished little-changed Tuesday in a refreshingly calm trading session that saw the CBOE Volatility Index decline below 20 for the first time since the SVB collapse.

Following gains of 0.2% on Monday, the S&P 500 finished lower by 0.2% today, while the tech-heavy Nasdaq 100 declined 0.5%. The Mid-Cap 400 and Small-Cap 600 both finished slightly higher.

Real estate equities were mixed with the Equity REIT Index finishing lower by 0.2% with 10-of-18 property sectors in positive territory, while the Mortgage REIT Index declined 0.2%.

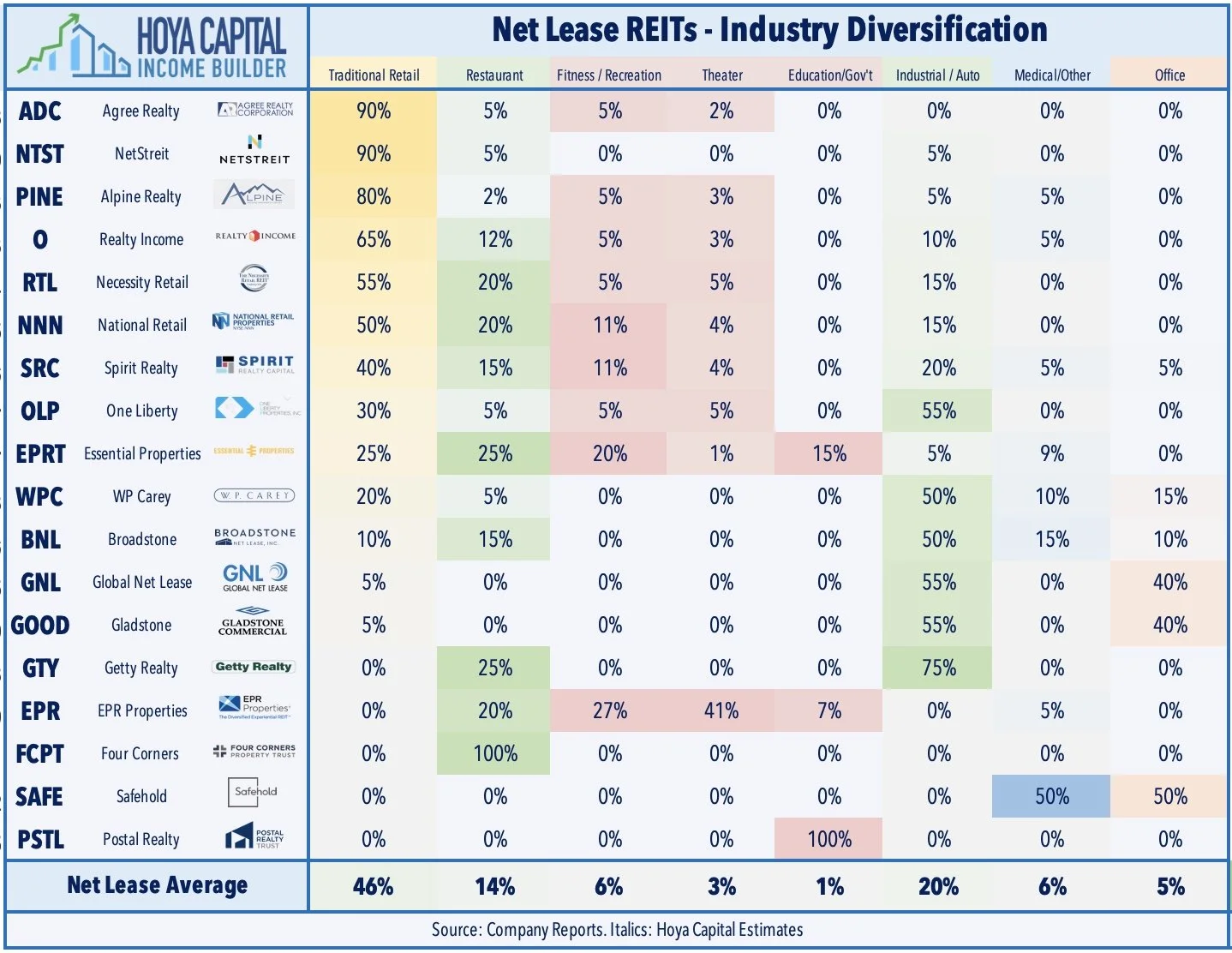

Movie theater chain AMC Entertainment - which is a tenant of several net lease REITs, including EPR Properties (EPR) - rallied more than 10% following a report from The Intersect that Amazon is exploring an acquisition of the company.

SL Green (SLG) was among the better performers today after it announced that Palo Alto Networks signed a long-term lease for a floor One Madison Avenue, bringing the company's 2023 signed office leasing volume to nearly 500K sq. feet, up from under 200k in Q4.

Income Builder Daily Recap

U.S. equity markets and bond markets finished little-changed Tuesday in a refreshingly calm trading session that saw the CBOE Volatility Index decline below 20 for the first time since the Silicon Valley Bank collapse. Giving back its gains of 0.2% on Monday, the S&P 500 finished lower by 0.2% today while the tech-heavy Nasdaq 100 declined 0.5%. The Mid-Cap 400 and Small-Cap 600 both finished slightly higher. Benchmark interest rates inched higher for a second session as concerns over further financial contagion have eased this week. The 2-Year Treasury Yield advanced 10 basis points to 4.08% today while the 10-Year Treasury Yield climbed 4 basis points to 3.56%. Real estate equities were mixed with the Equity REIT Index finishing lower by 0.2% with 10-of-18 property sectors in positive territory, while the Mortgage REIT Index declined 0.2%.

Real Estate Daily Recap

Best & Worst Performance Today Across the REIT Sector

Net Lease: Movie theater chain AMC Entertainment (AMC) - which is a tenant of several net lease REITs - rallied more than 10% following a report from The Intersect that Amazon (AMZN) is exploring an acquisition of the company, citing "Amazon insiders." Last week in Net Lease REITs: Avoiding The Winners Curse, we noted that movie theaters were one source of potential credit risk for the sector, which represents roughly 5% of overall net lease NOI, but nearly 50% of NOI for EPR Properties (EPR). Box Office Mojo data shows that box office revenue plunged 80% in 2020 and has remained about 25% below 2019 levels in early 2023. A handful of other net lease REITs have between 1.5-5% of their rents coming from movie theater tenants, but these REITs have not seen a material uptick in missed rents from these theater tenants despite the apparent distress.

Office: SL Green (SLG) was among the better performers today after it announced that Palo Alto Networks signed a long-term lease covering an entire tower floor at One Madison Avenue, bringing the company's 2023 signed office leasing volume to 492K sq. feet - up from under 200K in Q4 - while the company’s office leasing pipeline has increased to 1M sq. feet. The development at One Madison Avenue is scheduled for completion in October 2023 and is now 59% leased. Office REITs have been slammed over the past two months, with nearly a dozen REITs lower by more than 25% so far in 2023. Last week, Blackstone (BX) stopped making debt payments on its Hughes Center office campus in Las Vegas with public filing citing an inability to fund future monthly payments, which follows defaults over the past two months from Pimco, Brookfield, and RXR. Variable rate mortgage debt - and a lot of it - has been the common thread across these defaults. While the average office REIT uses just a fraction of the variable rate debt seen in these instances, there is concern that the gravity of private market distress will overwhelm any benefits of their comparative advantage.

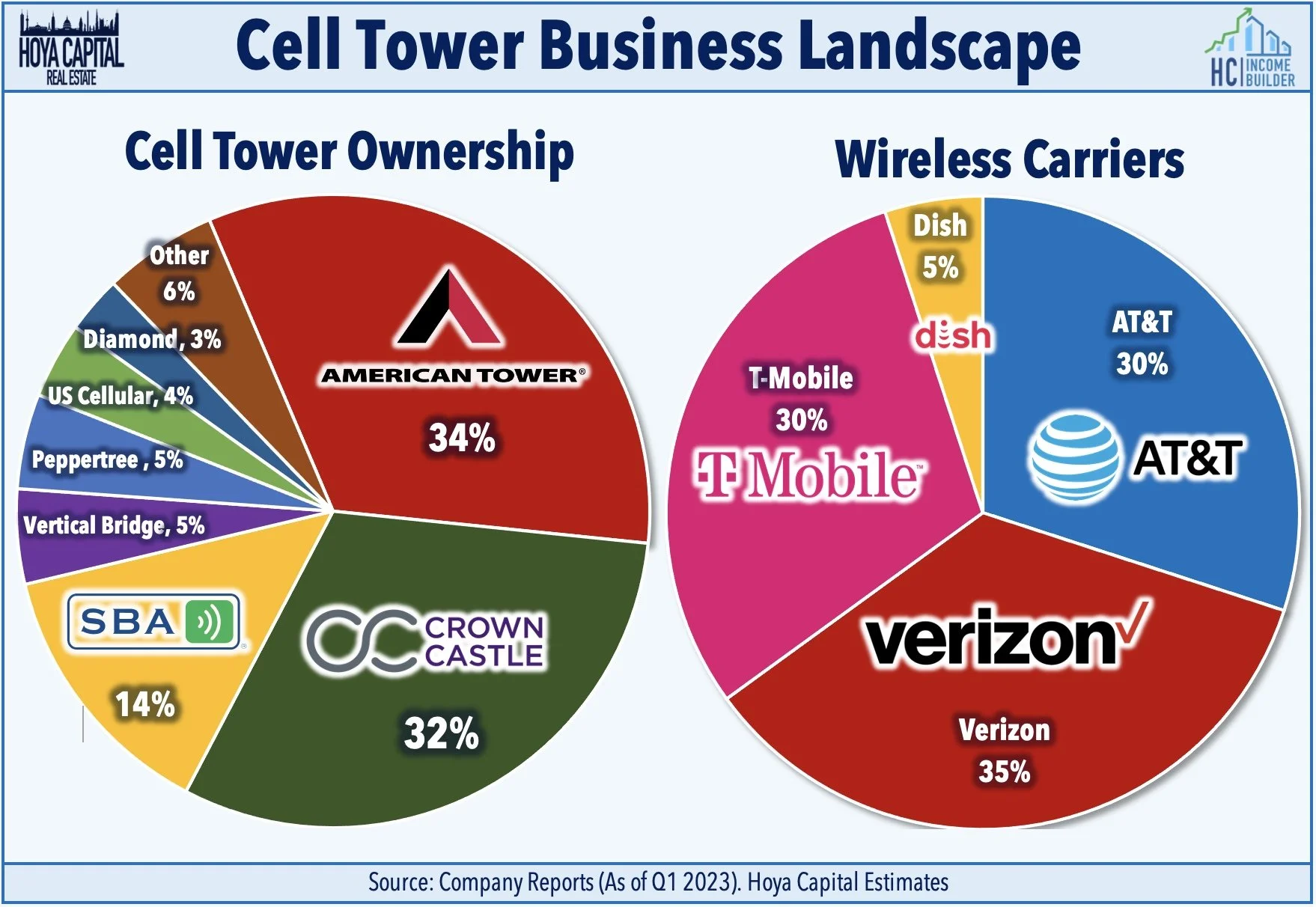

Cell Tower: Today, we published Cell Tower REITs: Tech Wreck Opportunity on the Income Builder marketplace, which discussed our updated sector outlook and recent allocations to our Dividend Growth portfolio. Cell Tower REITs have been one of the weakest-performing property sectors since early 2022, an uncharacteristic stretch of poor performance following a half-decade of industry-leading returns. Concern over the long-term competitive positioning of land-based cellular networks in the ever-evolving telecommunications industry has been amplified by the accelerated rollout of satellite-based networks offering some mobile connectivity - a concern that we believe is significantly "over-discounted" in current valuations. Awed by impressive rocket launches, the market has overlooked the more meaningful industry dynamic - the rapid growth of Fixed Wireless Access ("FWA") - which has further solidified the competitive positioning of land-based wireless networks - a market that is effectively "cornered" by the cell tower REITs.

Additional Headlines from The Daily REITBeat on Income Builder

Four Corners (FCPT) announced the acquisition of a Methodist Le Bonheur Pediatric Clinic property in Tennessee for $3.3 million at a 6.9% cap rate

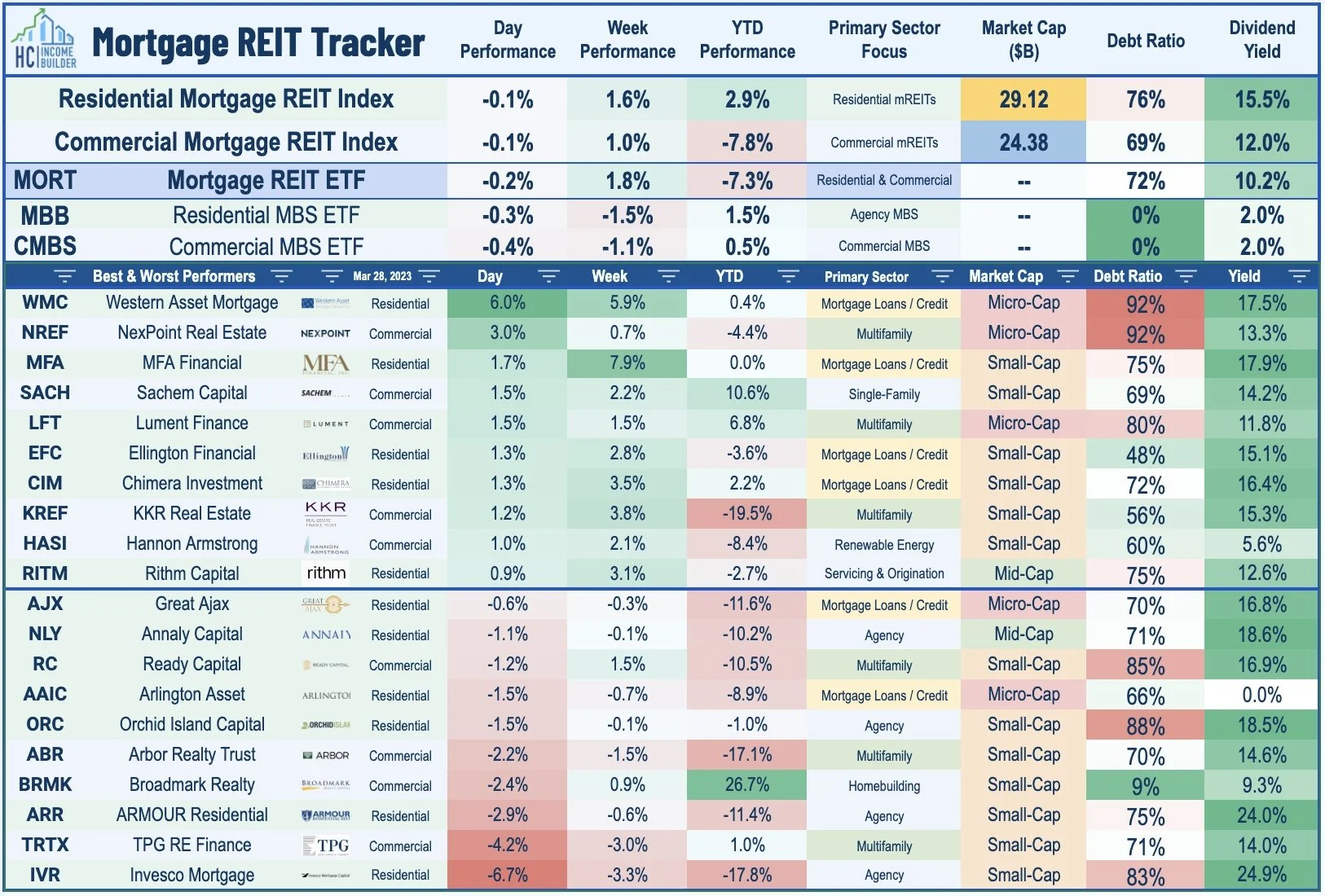

Mortgage REIT Daily Recap

Per the REIT Rankings Tracker available to Income Builder subscribers, mortgage REITs finished slightly lower today with residential and commercial mREITs both slipping 0.1%. Invesco Mortgage (IVR) dipped 6% today after announcing yesterday afternoon that it will reduce its dividend to $0.40/share - a 38.5% decrease from its prior dividend of $0.65 - representing a forward yield of 10.42%. IVR, which was previously the highest-yielding mREIT, was one of the REITs we flagged as at-risk for a dividend cut in our updated Mortgage REITs report published last week. IVR estimated that its Book Value Per Share ("BVPS") was $11.96-$12.44 as of March 17, a decline of roughly 5% since the end of Q4 at the midpoint of the range.

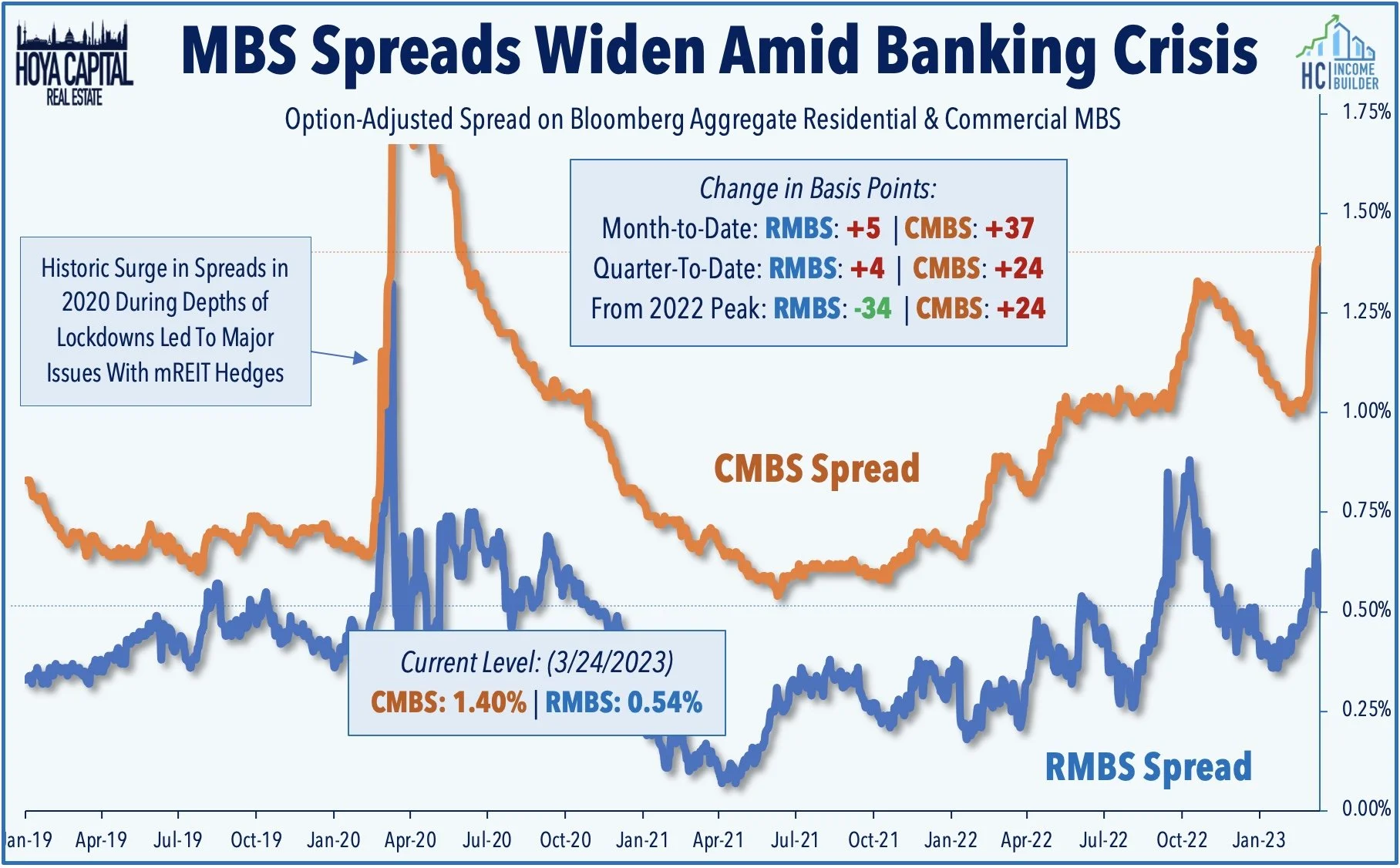

As discussed in Mortgage REITs: High-Yield Opportunities & Risk, mREITs have been under pressure in recent weeks by the fallout of the ongoing regional banking crisis amid a resurgence of interest rate volatility and credit concerns, erasing their once-robust gains for 2023. Commercial mREIT exposure to the troubled office sector has come into focus following a wave of mega-sized loan defaults from over-levered private owners. For Residential mREITs, Book Values remain in decent-shape as MBS spread-widening has been more-than-offset by a decline in benchmark rates, but sharp changes in rates heighten the hedge-related risk. Despite paying average dividend yields in the low-teens, the majority of mortgage REITs are still able to cover their dividends, but we identified several mREITs that are most at-risk of dividend reductions and broader risk factors.

Economic Data This Week

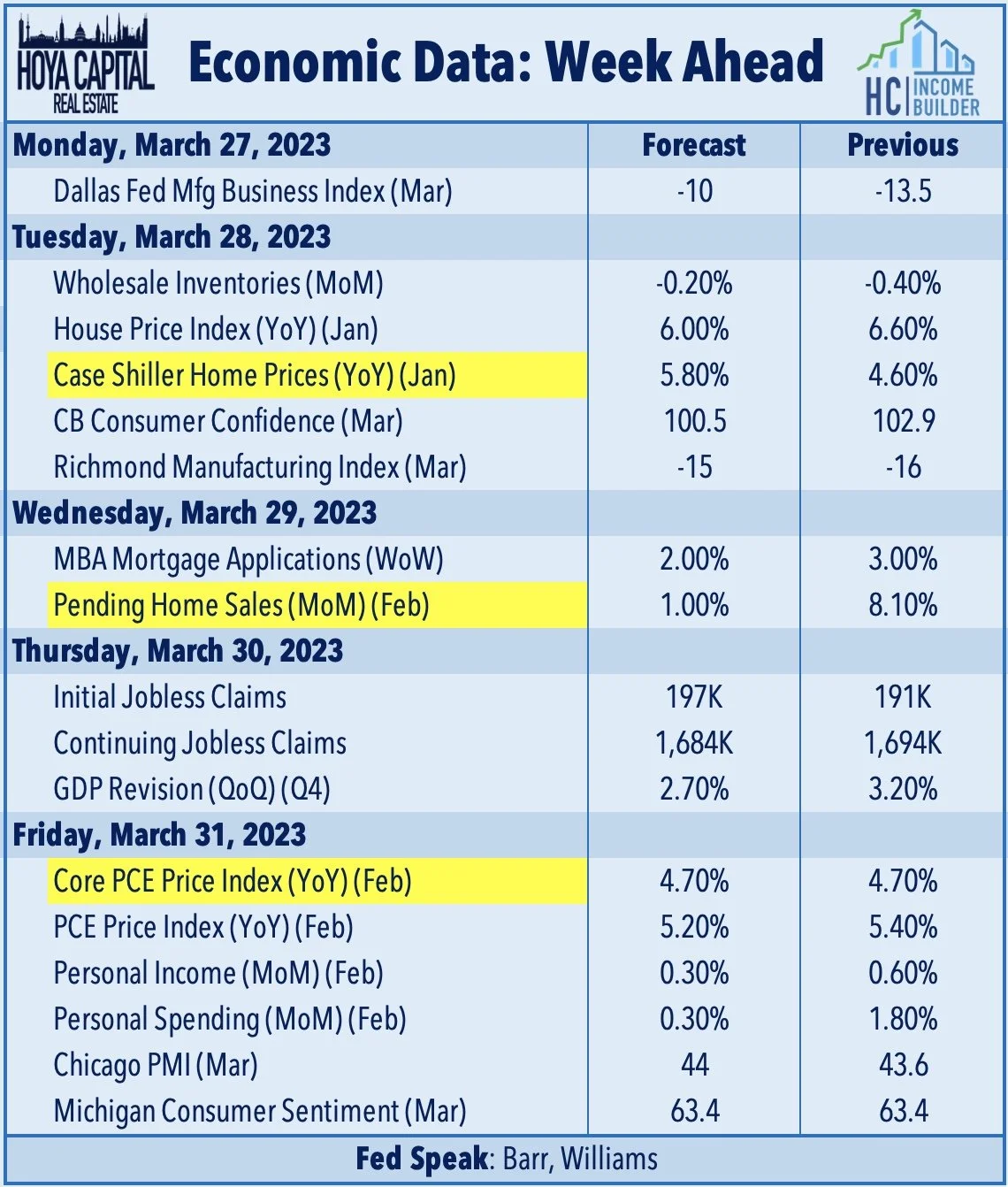

We'll see another fairly busy week of economic data in the week ahead. The state of the U.S. housing market will be a focus early in the week. On Tuesday, we saw home price data via the Case Shiller Home Price Index, which showed a seventh consecutive month of declining home prices in January with the 20-City composite now more than 5% below recent peaks. We'll see some more forward-looking data on Wednesday with Pending Home Sales data, which is expected to show a second straight monthly increase in February following a stretch of thirteen straight monthly declines. The most important report of the week comes on Friday with the PCE Price Index - the Fed's preferred gauge of inflation - which is expected to show a continued moderation in price pressures. In the same report, we'll also be looking at Personal Income and Personal Spending data for February, a key read on the state of the U.S. consumer.

Disclosure: Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index. Index definitions and a complete list of holdings are available on our website.

Hoya Capital Research & Index Innovations (“Hoya Capital”) is an affiliate of Hoya Capital Real Estate, a registered investment advisory firm based in Rowayton, Connecticut that provides investment advisory services to ETFs, individuals, and institutions. Hoya Capital Research & Index Innovations provides non-advisory services including market commentary, research, and index administration focused on publicly traded securities in the real estate industry.

This published commentary is for informational and educational purposes only. Nothing on this site nor any commentary published by Hoya Capital is intended to be investment, tax, or legal advice or an offer to buy or sell securities. This commentary is impersonal and should not be considered a recommendation that any particular security, portfolio of securities, or investment strategy is suitable for any specific individual, nor should it be viewed as a solicitation or offer for any advisory service offered by Hoya Capital Real Estate. Please consult with your investment, tax, or legal adviser regarding your individual circumstances before investing.

The views and opinions in all published commentary are as of the date of publication and are subject to change without notice. Information presented is believed to be factual and up-to-date, but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. Any market data quoted represents past performance, which is no guarantee of future results. There is no guarantee that any historical trend illustrated herein will be repeated in the future, and there is no way to predict precisely when such a trend will begin. There is no guarantee that any outlook made in this commentary will be realized.

Readers should understand that investing involves risk and loss of principal is possible. Investments in real estate companies and/or housing industry companies involve unique risks, as do investments in ETFs. The information presented does not reflect the performance of any fund or other account managed or serviced by Hoya Capital Real Estate. An investor cannot invest directly in an index and index performance does not reflect the deduction of any fees, expenses or taxes.

Hoya Capital Real Estate and Hoya Capital Research & Index Innovations have no business relationship with any company discussed or mentioned and never receives compensation from any company discussed or mentioned. Hoya Capital Real Estate, its affiliates, and/or its clients and/or its employees may hold positions in securities or funds discussed on this website and our published commentary. A complete list of holdings and additional important disclosures is available at www.HoyaCapital.com.