Cracks In Consumer • Global Inflation • REIT Dividend Hike

- U.S. equity markets plunged Wednesday amid mounting anxiety over looming stagflation following disappointing retail earnings results, mixed housing market data, and red-hot inflation data in the U.K. and Canada.

- Posting its worst day since June 2020 and pushing its drawdown to 18%, the S&P 500 slid 4.0% today while the tech-heavy Nasdaq 100 dipped 5.2% with its drawdown approaching 30%.

- Real estate equities were also broadly lower today as the Equity REIT Index declined 3.0% with all 19 property sectors in negative territory while Mortgage REITs declined 2.8%.

- Revealing potential "cracks in the consumer" economy, Target (TGT) plunged nearly 25% after reporting a "rapid slowdown" in key categories, which followed a similar dive from Walmart (WMT) on Tuesday.

- Mid America Apartments (MAA) was among the better-performers today after it became the 60th equity REIT to hike its dividend this year, announcing a 14.9% increase in its quarterly payout.

Income Builder Daily Recap

We recently launched Hoya Capital Income Builder - a premier income-focused investment research service through Seeking Alpha Marketplace - that will be the new exclusive home of all of Hoya Capital's investment research. Income Builder focuses on real income-producing asset classes that offer the opportunity for diversification, monthly income, capital appreciation, and inflation hedging. If you're not already on board, give us a try with a completely risk-free two-week trial and take a look around.

U.S. equity markets plunged Wednesday amid mounting anxiety over looming stagflation following disappointing retail earnings results, mixed housing market data, and red-hot inflation data in the U.K. and Canada. Posting its worst day since June 2020 and pushing its drawdown to 18%, the S&P 500 slid 4.0% today while the tech-heavy Nasdaq 100 dipped 5.2% as its drawdown now approaching 30%. Real estate equities were also broadly lower today as the Equity REIT Index declined 3.0% with all 19 property sectors in negative territory while Mortgage REITs declined 2.8%.

Stagflation concerns were amplified by a pair of hotter-than-expected inflation reports abroad as U.K. inflation jumped to a 40-year high of 9% while Canada inflation rose to a 30-year high at nearly 8%. Revealing potential "cracks in the consumer" economy, Target (TGT) plunged nearly 25% after reporting a "rapid slowdown" in key categories, which followed a similar dive from Walmart (WMT) on Tuesday. There was nowhere to hide from the selling pressure as all 11 GICS equity sectors were lower on the day with Consumer Staples (XLP) and Consumer Discretionary (XLY) each plunging more than 6%. Bonds caught a bid today amid an ongoing tug-of-war on rates between rising inflation and slowing growth. The 10-Year Treasury Yield pulled back 8 basis points to 2.89% - well below the 3.20% peak seen last Monday.

Real Estate Daily Recap

Apartment: Mid America Apartments (MAA) was among the better-performers today after it became the 60th equity REIT to hike its dividend this year, announcing a 14.9% increase in its quarterly payout. Today, we published our State of the REIT Nation which noted that amid the 'REIT Recovery,' FFO growth has significantly outpaced dividend growth, driving the dividend payout ratios to just 68.8% in Q1 - well below the 20-year average of 80%. With a historically low dividend payout ratio, we believe that REITs are well-equipped to deliver another year of robust dividend growth that may meet or exceed the record year in 2021 - despite the challenging macro environment. In the first quarter, REIT FFO was nearly 10% above its 4Q19 pre-pandemic level on an absolute basis, and 3% above pre-pandemic levels on a per-share basis while dividends per share remain 15% below 2019-levels.

Healthcare: Sabra Healthcare (SBRA) was also among the outperformers today after it finalized a previously-announced $236.5M acquisition of a 50% interest in Sienna Senior Living - a high-quality Canadian senior housing consisting of 11 senior housing communities in Ontario and Saskatchewan. In our REIT Earnings Recap published last week, we noted that Sabra and Omega Healthcare (OHI) have been upside standout over the past month after reporting resolutions in rent collection issues from several troubled SNF operators and an uptick in occupancy rates throughout the quarter. Senior housing REITs Ventas (VTR) and Welltower (WELL) have also been upside standouts after reporting an impressive rebound in their Senior Housing Operating ("SHOP") portfolios as COVID headwinds subside.

Mortgage REIT Daily Recap

Per the REIT Rankings Tracker available to Income Builder subscribers, mortgage REITs held-up rather well today with residential mREITs declining 1.9% while commercial mREITs declined 2.8%. Ares Commercial (ACRE) dipped more than 8% after launching a secondary common stock offering of 7M shares for expected gross proceeds of $105M. In our Earnings Recap published last week, we noted that mREITs have been an upside standout over the past several weeks after earnings season showed that Book Value declines were generally not as steep as analysts projected. Residential mREIT Book Value Per Share ("BVPS") metrics declined by 8.4%, on average while commercial mREIT reported an average BVPS increase of 0.1%.

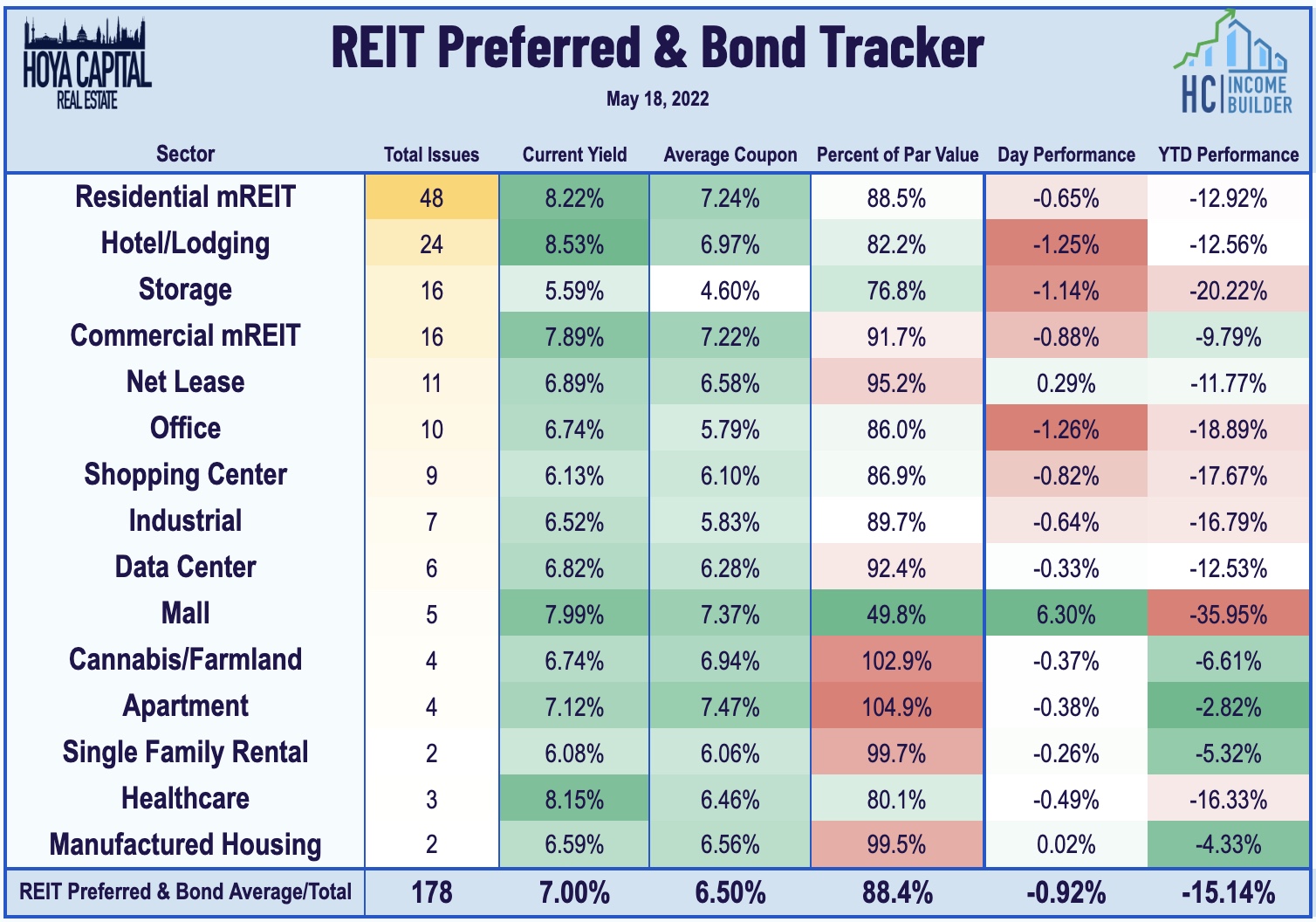

REIT Preferreds & Capital Raising

Per the Income Builder Preferred Tracker available to Income Builder subscribers, the Hoya Capital REIT Preferred Index finished lower by 0.92% today. REIT Preferreds ended 2021 with price returns of roughly 8.0% and total returns of roughly 14%. There are now roughly 180 REIT-issued exchange-listed preferred and debt securities with an average current yield of 6.96%. Over in the capital markets today, apartment REIT Equity Residential (EQR) announced a forward sale agreement with a group of banks to sell up to 13M shares of common stock. Elsewhere, healthcare REIT LTC Properties (LTC) entered into a note purchase agreement to issue $75M of 3.66% senior unsecured notes maturing on May 17, 2033.

Economic Data This Week

Housing data highlights the economic calendar in the week ahead which investors and the Fed will be watching carefully for indications of the impact of surging mortgage rates on housing demand. On Tuesday, we'll Homebuilder Sentiment which is expected to show a moderation to 75. On Wednesday, we'll see Housing Starts and Building Permits which are also expected to moderate from last month's stronger-than-expected levels. On, Thursday we'll see Existing Home Sales data which is expected to show a more pronounced pull-back to a 5.53M annualized rate, which would be the lowest since June 2020. We'll also see Retail Sales data on Tuesday and hear a half-dozen scheduled Federal Reserve member speeches or events including remarks from Chair Powell on Tuesday.

Access Our Complete Research Library

We recently launched Hoya Capital Income Builder - the new premier investment research service focused on real income-producing asset classes. Whether your focus is High Yield or Dividend Growth, we’ve got you covered with high-quality, actionable investment research and a comprehensive suite of tools and models to help build sustainable portfolio income targeting premium dividend yields of up to 10%. And of course, subscribers receive complete access to our investment research - including reports that are never published elsewhere - from Hoya Capital and our team of contributors.

Disclosure: Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index. Index definitions and a complete list of holdings are available on our website.

Additional Disclosure: It is not possible to invest directly in an index. Index performance cited in this commentary does not reflect the performance of any fund or other account managed or serviced by Hoya Capital Real Estate. Data quoted represents past performance, which is no guarantee of future results. Information presented is believed to be factual and up-to-date, but we do not guarantee its accuracy.