Fed Eyes 75 • Double-Digit PPI • REIT Dividend Hike

- U.S. equity markets remained under pressure Tuesday while benchmark interest rates continued to plow higher ahead of the FOMC interest rate decision as investors brace for a 75 basis-point hike.

- Following its worst day since March 2020 and pushing the major benchmarks deeper into correction territory, the S&P 500 declined another 0.4% today, but the tech-heavy Nasdaq 100 gained 0.2%.

- The Equity REIT Index declined 0.8% today with 10-of-18 property sectors in negative-territory. After the close, Realty Income hiked its monthly dividend for the second-time this year.

- Benchmark interest rates continued their surge today as market-implied probabilities of a 75 basis point Fed rate hike - which was below 4% at this time last week - surged to above 95% today.

- Inflation Stays Red-Hot: The Bureau of Labor Statistics reported this morning that Producer Prices soared at an 10.8% annual rate in May - slightly cooler than consensus estimates - but still notching the third-highest annual inflation rate on record.

Income Builder Daily Recap

We recently launched Hoya Capital Income Builder - a premier income-focused investment research service through Seeking Alpha Marketplace - that will be the new exclusive home of all of Hoya Capital's investment research. Income Builder focuses on real income-producing asset classes that offer the opportunity for diversification, monthly income, capital appreciation, and inflation hedging. If you're not already on board, give us a try with a completely risk-free two-week trial and take a look around.

U.S. equity markets remained under pressure Tuesday while benchmark interest rates continued to plow higher ahead of the FOMC interest rate decision as investors brace for a 75 basis point rate hike. Following its worst day since March 2020 and pushing the major benchmarks deeper into correction territory, the S&P 500 declined another 0.4% today, but the tech-heavy Nasdaq 100 gained 0.2% following declines of nearly 5% on Monday. Real estate equities were mixed today as a rebound from industrial and storage REITs was offset by declines from cell tower REITs. The Equity REIT Index declined 0.8% today with 10-of-18 property sectors in negative territory while the Mortgage REIT Index declined by 2.4%.

Benchmark interest rates continued their surge today as market-implied probabilities of a 75 basis point Fed rate hike - which was below 4% at this time last week - surged to above 95% today. The 10-Year Treasury Yield advanced another 12 basis points to 3.48% - the highest level in more than a decade, which sent mortgage rates jumping to above 6% on the 30-year fixed - more than doubling since the start of the year. The cracks deepened in the highly-speculative crypto space today as the Bitcoin sell-off intensified amid ongoing liquidity concerns at crypto exchanges and service providers. Nine of the eleven GICS equity sectors were lower today with the Utilities (XLU) sector dragging on the downside.

Inflation Stays Red-Hot: The Bureau of Labor Statistics reported this morning that Producer Prices soared at an 10.8% annual rate in May - slightly cooler than consensus estimates - but still notching the third-highest annual inflation rate on record. Goods-prices drove nearly two-thirds of the increase and within the goods category, 70% of the increase can be attributed to an 8.4% month-over-month advance in the index for gasoline. On the services side, costs for truck transportation drove the cost increases. Among the relevant PPI metrics for the real estate industry, the PPI Self-Storage Index - which closely tracks rent growth in the storage REIT sector - posted another brisk month-over-month gain of 1.8%, pushing the year-over-year advance to 17.2% - just below the prior month's record-high rate of 17.9%.

Real Estate Daily Recap

Farmland: Gladstone Land (LAND) provided a business update in which it commented that it's close to finalizing an agreement to add up to 60 wind turbines, 1,600 acres of solar panels, and additional infrastructure as part of a renewable energy agreement on 16,500 areas of land. Elsewhere, Farmland Partners (FPI) announced that it purchased 280 acres of farmland in Illinois for $3.4 million, commenting that it remains in "growth mode." Publicly-traded landowners - specifically timber and farmland REITs - have been among the best-performing real estate sectors this year amid concerns over persistent inflation and soaring commodities prices.

Single-Family Rental: Today, we published Single-Family Rental REITs: Sturdy Shelter Amid Slowdown on the Income Builder marketplace which discussed recent developments and our updated outlook for the SFR sector. Amid mounting recession worries and a return of heart-stopping market volatility, residential REITs - particularly the traditionally countercyclical single-family rentals - should prove to be a source of relative shelter. Single-Family Rental REITs were born from the last economic crisis when a cascade of foreclosures enabled a new class of institutional rental operators to emerge by buying distressed properties en-masse. Similar distress in the U.S. housing market is highly unlikely given the underlying supply constraints resulting from a decade of underbuilding, and ironically, due to the presence of well-capitalized institutional investors. SFR REITs enter this uncertain period on solid footing, benefiting from historically favorable Buy vs. Rent economics.

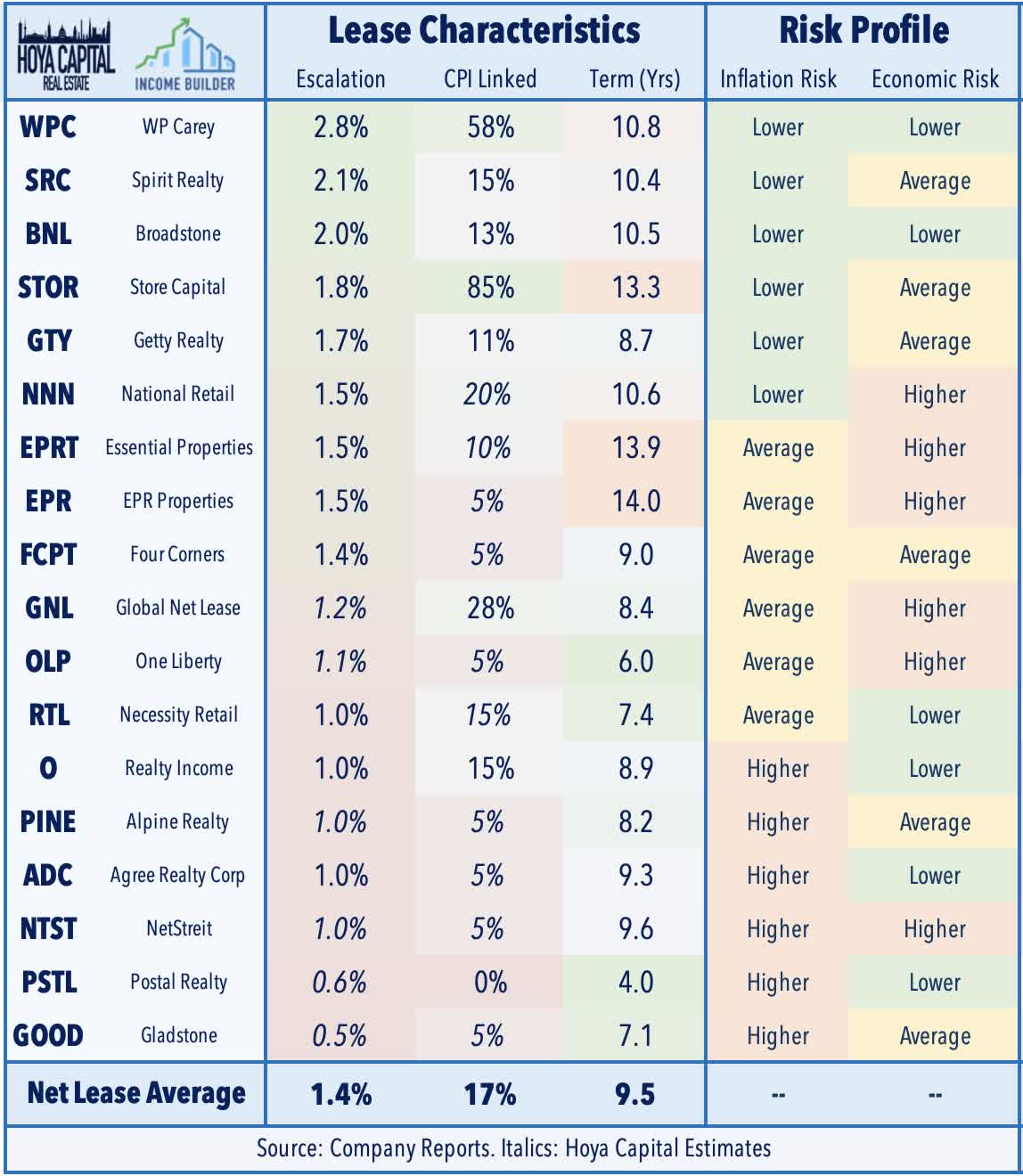

Net Lease: After the close today, Realty Income (O) hiked its monthly dividend by 0.2% to $0.2475/share. In Net Lease REITs: Surviving Inflation, For Now, we discussed why net lease REITs have surprisingly been among the best-performing property sectors this year despite the challenging macroeconomic environment. Even with rent growth significantly lagging inflation, net lease REITs are still on-pace for double-digit earnings growth as robust accretive external growth has more than offset the drag from muted property-level growth. Within the net lease sector, inflation risk isn't always efficiently-priced, however, and after taking a deep-dive into the inflation risk across the sector, we reiterate our positive outlook on a handful of REITs that can outperform in a variety of potential macroeconomic environments.

Mortgage REIT Daily Recap

Per the REIT Rankings Tracker available to Income Builder subscribers, mortgage REITs remained under pressure today with residential mREITs lower by 2.9% while commercial mREITs declined by 2.3%. Several of the more highly-levered mortgage REITs remained under pressure today including AG Mortgage (MITT) and Invesco Mortgage (IVR), which has dipped nearly 25% on the week. The especially sharp selling pressure in IVR may be amplified by confusion over its 1-10 reverse split last week, which prompted the Bloomberg automated news feed to publish a report projecting a 90% dividend cut, which was based on the pre-split dividend rate.

REIT Preferreds & Capital Raising

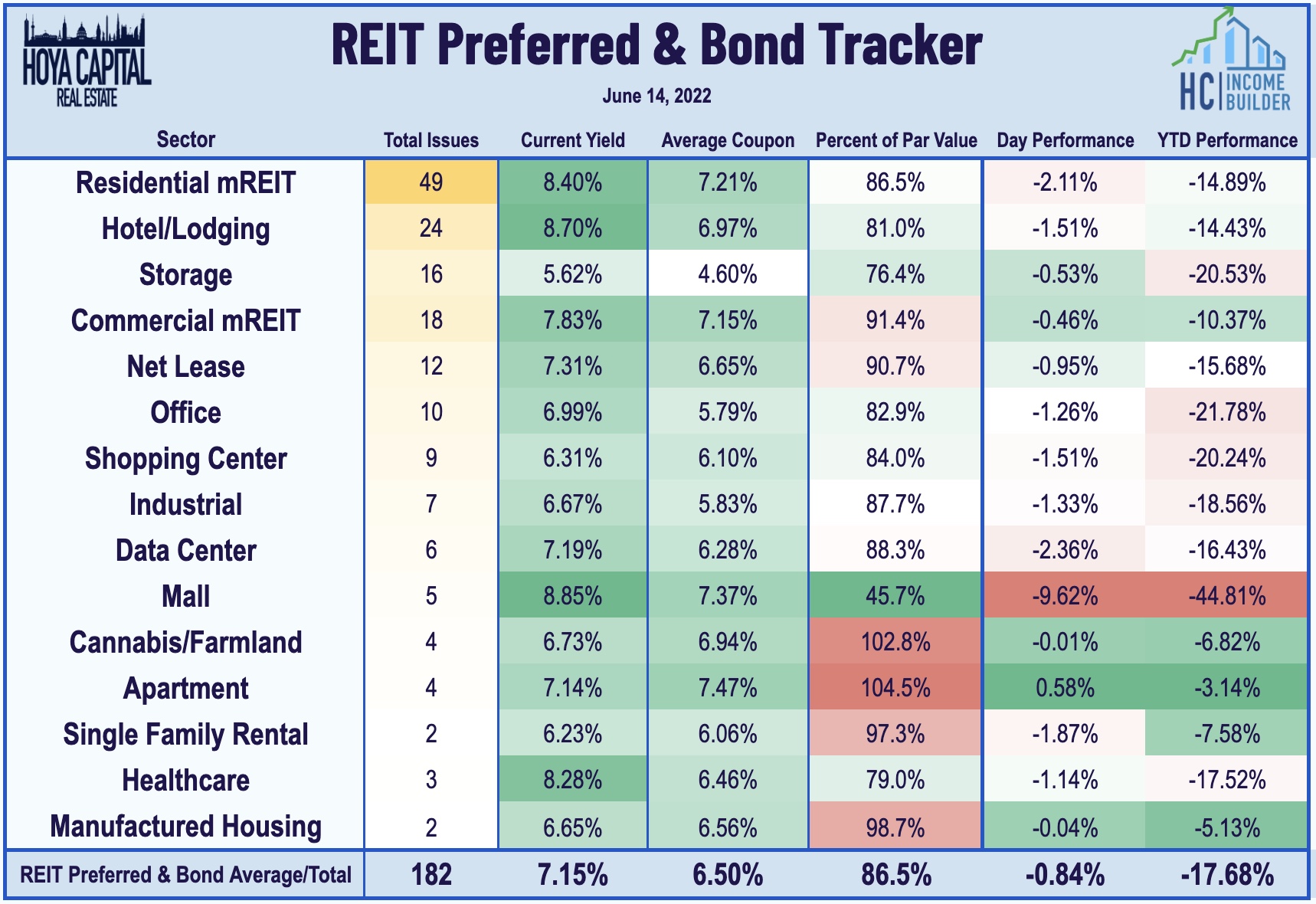

Per the Income Builder Preferred Tracker available to Income Builder subscribers, REIT Preferred stocks finished lower by 0.84% today, on average, following one of the sharpest one-day declines on record yesterday. REIT Preferreds are lower by roughly 13% on a total return basis this year after ending 2021 with price returns of roughly 8.0% and total returns of roughly 14%. There are now roughly 180 REIT-issued exchange-listed preferred and debt securities with an average current yield of 7.06%. Today, S&P Ratings raised American Homes' (AMH) credit rating to “BBB” from “BBB-“ with a stable outlook. Following its acquisition announcement by Prologis (PLD), S&P also placed Duke Realty's (DRE) credit ratings on CreditWatch with positive implications, reflecting its view that the transaction "will enhance Duke's credit profile given its acquisition by a higher-rated entity."

Economic Data This Week

The jam-packed week of economic data and monetary policy decisions kicked off today with the Producer Price Index for May. On Wednesday, we'll see Retail Sales data - which is expected to show the lowest month-over-month increase of 2022 - while Homebuilder Sentiment is expected to show a moderation to 68 which would be the lowest level since early in the pandemic. All eyes will be on the Federal Reserve on Wednesday afternoon for the FOMC Interest Rate Decision. Finally, on Thursday, we'll see Housing Starts and Building Permits which are expected to show a continued moderation in the pace of new home construction.

Access Our Complete Research Library

We recently launched Hoya Capital Income Builder - the new premier investment research service focused on real income-producing asset classes. Whether your focus is High Yield or Dividend Growth, we’ve got you covered with high-quality, actionable investment research and a comprehensive suite of tools and models to help build sustainable portfolio income targeting premium dividend yields of up to 10%. And of course, subscribers receive complete access to our investment research - including reports that are never published elsewhere - from Hoya Capital and our team of contributors.

Disclosure: Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index. Index definitions and a complete list of holdings are available on our website.

Additional Disclosure: It is not possible to invest directly in an index. Index performance cited in this commentary does not reflect the performance of any fund or other account managed or serviced by Hoya Capital Real Estate. Data quoted represents past performance, which is no guarantee of future results. Information presented is believed to be factual and up-to-date, but we do not guarantee its accuracy.