Stocks Slide • REIT Earnings • Housing Rebound

U.S. equity markets finished sharply lower Tuesday while benchmark interest rates retreated after First Republic Bank plunged following disappointing first quarter results, sparking renewed financial stability concerns.

Posting its worst one-day decline since mid-March, the S&P 500 slid 1.6% today, while Mid-Cap 400 declined 1.9% and the Small-Cap 600 dipped 2.6%. The Dow dipped 344 points.

Real estate equities were among the better-performers today, buoyed by a retreat in benchmark interest rates and a solid slate of earnings reports. The Equity REIT Index declined 1.0%.

New Home Sales rose to the highest level in a year in March. PulteGroup (PHM) - the fourth largest homebuilder in the nation - was among the top-performers today after its results easily topped consensus estimates.

Strip Center REIT Site Centers (SITC) was also among the best performers today after reporting strong first quarter results and raising its full-year guidance. Lab space owner Alexandria Real Estate (ARE) and apartment REIT NexPoint Residential (NXRT) slipped 3% after reporting mixed results.

Income Builder Daily Recap

U.S. equity markets finished sharply lower Tuesday while benchmark interest rates retreated after First Republic Bank plunged following disappointing first-quarter results, sparking renewed financial stability concerns. Posting its worst one-day decline since mid-March, the S&P 500 slid 1.6% today, while Mid-Cap 400 declined 1.9% and the Small-Cap 600 dipped 2.6%. Real estate equities were among the better-performers today, buoyed by a retreat in benchmark interest rates and a solid slate of earnings reports. The Equity REIT Index declined 1.0% today, with 16-of-18 property sectors in negative territory, while the Mortgage REIT Index declined 2.5%. Homebuilders were upside standouts following a strong report from PulteGroup and data showing that New Home Sales rose to the highest level in a year in March.

The CBOE Volatility Index (VIX) surged 15% today after easing to its lowest-lev els in seventeen months earlier this week. The renewed volatility was sparked by downbeat results from regional bank First Republic (FRC), which plunged nearly 50% today to record-lows after reporting higher-than-expected withdrawals in the first quarter. FRC had stabilized in recent weeks after turmoil in mid-March following the collapse of Silicon Valley Bank, Signature Bank, and Silvergate Capital. The 2-Year Treasury Yield dipped 15 basis points to 3.94% today, while the 10-Year Treasury Yield declined 10 basis points to 3.39%. All eleven GICS equity sectors finished lower on the session, with Materials (XLB) and Technology (XLK) stocks lagging on the downside.

Real Estate Daily Recap

Best & Worst Performance Today Across the REIT Sector

Homebuilders: The Commerce Department reported this morning that U.S. New Home Sales rose for a fourth-straight month to the highest level in a year in March, consistent with recent data showing that the previously-sluggish U.S. housing sector has again emerged as a bright spot, consistent with its countercyclical performance trends exhibited throughout the pandemic. PulteGroup (PHM) - the fourth largest homebuilder in the nation - was among the top-performers today after its results easily topped consensus estimates and boosted its share buyback program. Notably, PHM reported that its cancellation rate dropped to 13% in Q1, down from 24% in Q3 of last year. NVR (NVR) - the third-largest homebuilder - declined about 2% today after reporting results that were roughly in-line with estimates, noting that its new orders in Q1 were roughly flat year-over-year, a significant improvement from Q4 in which orders decreased by 27%. We'll hear results from Taylor Morrison (TMHC) and M/I Homes (MHO) tomorrow morning.

Strip Center: Site Centers (SITC) was among the best-performers today after reporting strong first quarter results and raising its full-year guidance. Continuing the trend of accelerating rental rate growth and rising occupancy rates, SITC reported that it achieved impressive cash leasing spreads of 20.3% on new leases and 8.7% on renewals while noting that its occupancy rate increased to 95.9% - up 50 basis points from last quarter and 270 bps from last year. Lifted by this strong leasing momentum, SITC raised its full-year NOI growth outlook by 50 basis points to 2.25% at the midpoint and its full-year FFO growth outlook by 90 basis points to 2.6%. SITC noted that Bed Bath & Beyond (BBBY) - which filed for Chapter 11 this week - comprises 1.8% of its base rent, but commented, "we feel extremely well prepared for a focused marketing cycle and are confident that there are single-user backfill options for 16 of those locations given the amount of inbound activity we’ve seen over the last several months... we would very much like to recapture space from weak tenants while demand for that space is strong." We'll hear results this afternoon from Retail Opportunity (ROIC).

Healthcare: Lab space owner Alexandria Real Estate (ARE) slipped about 3% today despite reporting better-than-expected first-quarter results, noting that its same-store NOI rose 9% in Q1, and reiterated the midpoint of its full-year FFO outlook calling for FFO growth of 6.4%. ARE noted that it collected 99.9% of rents in Q1 and 99.7% thus far in April - pushing back on concerns over its tenants' exposure to Silicon Valley Bank - while achieving record-high rental rate increases of 48.3% GAAP/ 24.2% cash. ARE collected 99.9% of Q1 rents, but its leasing volume moderated to 1.2M SF, which was the lowest since early 2020. ARE also revised lower its full-year occupancy outlook from 95.3% to 95.1% and scaled back its targets for acquisition spending and construction spending from a combined 3.275B to $2.950B. ARE recognized a $139M impairment on an office campus that it acquired in January 2020 - its only traditional office assets in the Boston market, noting that the "demand for [traditional] office space has deteriorated considerably" since its purchase.

Apartment: NexPoint Residential (NXRT) slipped about 3% today after reporting mixed results. NXRT maintained its full-year NOI outlook at a sector-high of 11.0% but lowered its full-year FFO growth target by 130 bps to 2.2%, a revision driven by higher interest expense. NXRT reported blended rental rate increases of 3.8% - comprised of 2.8% growth on new leases and 4.8% on renewals - a modest cooldown from the 4.8% blended spread reported in the prior quarter. The regional spread was notable, however, with its South Florida and Atlanta markets posting new lease spreads of nearly 10% while Houston and Las Vegas posted negative spreads of -2.9% and 4.5%, respectively. NXRT also held its dividend steady at $0.42/share (3.8% dividend yield). We'll hear results this afternoon from Equity Residential (EQR).

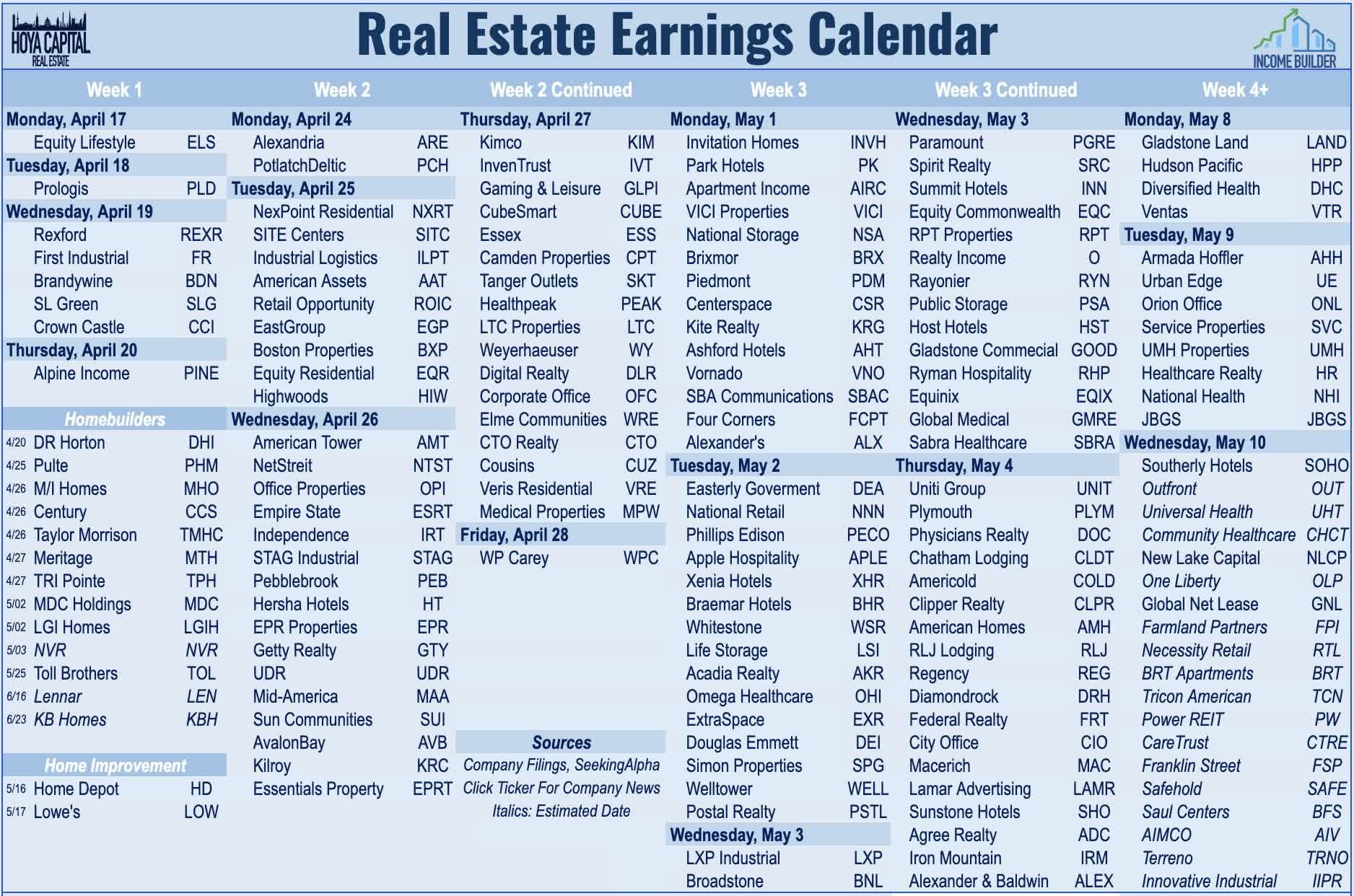

Today we published our REIT Earnings Preview. Real estate earnings season kicks into gear this week, and over the next month, we'll hear results from 175 equity REITs, 40 mortgage REITs, and dozens of housing industry companies. The flat performance on the REIT Index this year hides some notably sharp bifurcations within the sector, with residential and industrial sectors posting notable outperformance, offset by weakness in office. Many well-capitalized REITs are equipped to "play offense" and take advantage of acquisition opportunities from weaker private players - but whether or not these typically-defensive REITs are ready to take a more aggressive tact remains a key focus. Most equity REITs still have a healthy buffer to protect current payout levels if macroeconomic conditions take a turn for the worse, but we'll be closely-monitoring dividend commentary in the office, mortgage, and healthcare REIT sectors. In addition to the aforementioned reports, we'll hear results this afternoon from office REITs Boston Properties (BXP) and Highwoods (HIW) and industrial REITs EastGroup (EGP) and Industrial Logistics (ILPT).

Mortgage REIT Daily Recap

Mortgage REITs under pressure today with residential mREITs slipping 1.8% while commercial mREITs declined 2.8%. Seven Hills (SEVN) gained 1% after it reported adjusted EPS of $0.39/share - covering its $0.35 dividend - while noting that its BVPS declined 1.4% to $18.21. SEVN noted that all of its loans remain current. KKR Real Estate (KREF) dipped about 6% after reporting adjusted EPS of $0.48/share - easily covering its $0.43/share dividend - but noted that its BVPS declined 4.7% to $17.16, resulting from an $0.88/share increase in its Current Expected Credit Loss ("CECL") allowance due to additional reserves for two office loans. KREF noted that it collected 100% of interest payments. AGNC Investment (AGNC) declined 3% after it reported adjusted EPS of $0.70 - covering its $0.30/share dividend - but noted that its BVPS declined 4.4% to $9.41. AGNC commented that it expects Agency MBS spreads to "remain meaningfully wider than historical averages...as the Fed, and now banks, gradually reposition their balance sheets."

Economic Data This Week

The state of the U.S. housing market remains in focus early in the week across the busy slate of economic data. On Tuesday, we'll see home price data via the Case Shiller Home Price Index, which is expected to show an eighth consecutive month of declining home prices in February, with the 20-City composite expected to show that prices are now flat on a year-over-year basis and about 5% below recent peaks. We'll see some more-forward-looking data on Thursday with Pending Home Sales data, which is expected to show a third straight monthly increase in March following a stretch of thirteen straight monthly declines. The most important report of the week comes on Friday with the PCE Price Index - the Fed's preferred gauge of inflation - which is expected to show a continued moderation in price pressures. In the same report, we'll also be looking at Personal Income and Personal Spending data for March, a key read on the state of the U.S. consumer.

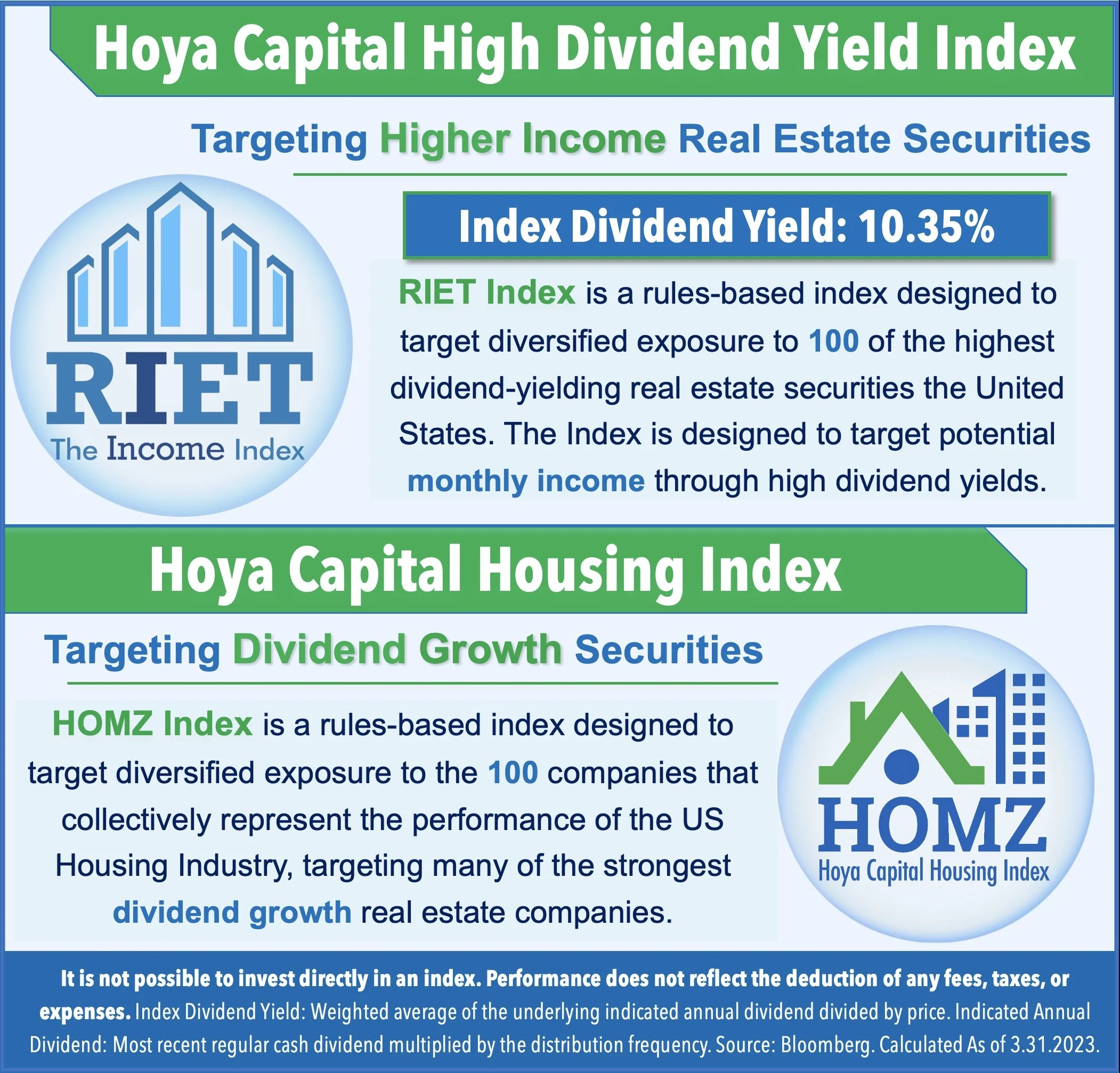

Disclosure: Hoya Capital Real Estate advises two Exchange-Traded Funds ("ETFs") listed on the NYSE. In addition to any long positions listed, Hoya Capital is long all components in the Hoya Capital Housing Index and in the Hoya Capital High Dividend Yield Index. Index definitions and a complete list of holdings are available on our website.

Hoya Capital Research & Index Innovations (“Hoya Capital”) is an affiliate of Hoya Capital Real Estate, a registered investment advisory firm based in Rowayton, Connecticut that provides investment advisory services to ETFs, individuals, and institutions. Hoya Capital Research & Index Innovations provides non-advisory services including market commentary, research, and index administration focused on publicly traded securities in the real estate industry.

This published commentary is for informational and educational purposes only. Nothing on this site nor any commentary published by Hoya Capital is intended to be investment, tax, or legal advice or an offer to buy or sell securities. This commentary is impersonal and should not be considered a recommendation that any particular security, portfolio of securities, or investment strategy is suitable for any specific individual, nor should it be viewed as a solicitation or offer for any advisory service offered by Hoya Capital Real Estate. Please consult with your investment, tax, or legal adviser regarding your individual circumstances before investing.

The views and opinions in all published commentary are as of the date of publication and are subject to change without notice. Information presented is believed to be factual and up-to-date, but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. Any market data quoted represents past performance, which is no guarantee of future results. There is no guarantee that any historical trend illustrated herein will be repeated in the future, and there is no way to predict precisely when such a trend will begin. There is no guarantee that any outlook made in this commentary will be realized.

Readers should understand that investing involves risk and loss of principal is possible. Investments in real estate companies and/or housing industry companies involve unique risks, as do investments in ETFs. The information presented does not reflect the performance of any fund or other account managed or serviced by Hoya Capital Real Estate. An investor cannot invest directly in an index and index performance does not reflect the deduction of any fees, expenses or taxes.

Hoya Capital Real Estate and Hoya Capital Research & Index Innovations have no business relationship with any company discussed or mentioned and never receives compensation from any company discussed or mentioned. Hoya Capital Real Estate, its affiliates, and/or its clients and/or its employees may hold positions in securities or funds discussed on this website and our published commentary. A complete list of holdings and additional important disclosures is available at www.HoyaCapital.com.